The Trade-Up Plan – How to Retire in 8 Years Using Tax-Free Exchanges

This article is about the Trade-Up Plan, which shows you how to quickly build a portfolio of rental properties with strong cash flow using 1031 exchanges. In the sections that follow, I’ll first share the basics steps of the Trade-Up Plan. Then I’ll give you a detailed example that begins with $34,000 in savings and within 8 years produces a portfolio of rentals with income of over $40,000 per year and equity of $372,500. I’ll also show how to use this portfolio to retire early and achieve financial independence.

If you’ve just found me at coachcarson.com, this article is part of a series of Real Estate Retirement Plans. The goal of this series is to give you specific, practical real estate plans that help you build wealth and reach the destination called financial independence as quickly as possible. After that, you can begin doing what matters in your life without the pesky reality of lack of money.

There is not one right plan for everyone. I provide multiple plans so that you can choose which applies best to your life. Some of the other plans include:

A key part of the Trade-Up Plan that I’ll cover in this article is a technique called a tax-free exchange. This technique is also known in the U.S. as a 1031-exchange, which stands for a section of the US tax code. This section allows investors to postpone the payment of federal taxes when a property sold if it’s replaced by a like-kind property. Read more details and the rules that must be followed on this IRS web page.

Most importantly, this technique helps you start small and maximize your growth by reducing the negative impact of federal taxes each time you sell a property.

Now let’s get started with the details of the Trade-Up Plan.

What is the Trade-Up Plan?

The Trade-Up Plan basically works like this:

- Save up cash for a down payment, closing costs, and cash reserves

- Buy a simple rental property (like a duplex) at a slight discount (10-15%)

- Rent the property, build equity, and save cash for a period of time (like 2 years)

- Sell the property

- Use a 1031 tax-free exchange to purchase a larger property, also at a slight discount

- Repeat and continue growing until you meet your financial goals

This plan works well because it combines three powerful investing tools:

- Discount purchases – buy solid rental properties at a slight discount

- Debt leverage – control a larger property with only 20-25% of the purchase price

- Tax-free exchange – harvest equity through a sale, pay no tax, buy another property

The equity and cash flow grow and compound fast because of the repeated purchases, rental holding periods, and strategic resales.

Now let me demonstrate the concept through an example. Please keep in mind that this example is provided for educational purposes. The details of applying any real estate strategy require on-the-ground, local knowledge. And the specific application depends upon your unique circumstances. You should seek the help of local, qualified professionals to help you apply these principles.

Example of the Trade-Up Plan

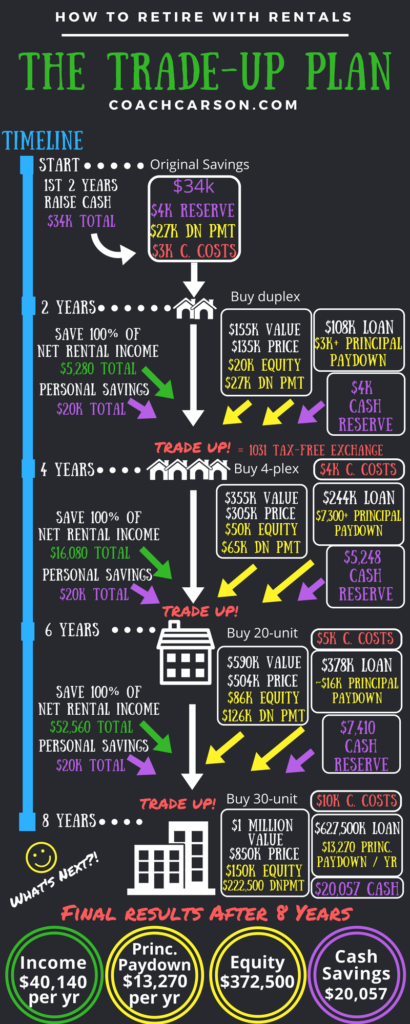

This infographic gives you an overview of how the Trade-Up Plan works.

While the infographic gives you the big picture and final results, there are more details to consider. The rest of this article will explain each step in greater depth.

Self-Imposed Rules to Maximize Your Results

Let’s start with some self-imposed investing rules to guide your acquisitions and borrowing during the Trade-Up Plan. These rules will help ensure your financial success and reduce risk:

- Each unit must produce at least $100/month in net rental income (before tax). See How to Calculate Rental Property Cash Flow. My definition of net rental income is the same as cash flow after financing in the article.

- The purchase price must be at least 10% below full current value (or the value can be quickly increased with minimal cost by increasing rent, decreasing expenses, or both).

- No major remodels

- Class B or C property types desired (using this A – D scale). No old, cheap, war-zone properties.

- All loans must be 25-30 year amortizations.

- No loan balloon payments shorter than 10 years

These rules are important disciplines for a few reasons. The rental units must have some equity that can be harvested when resold, and they must produce cash flow to help you pile up savings for the next purchase. The units must also be quality enough to attract buyers who will want to purchase the properties from you. And the loans must have attractive enough terms to produce your needed cash flow while not putting your entire investment at risk.

With those guidelines in mind, let’s now explore each step of the Trade-Up Plan in more detail.

Years 1 & 2 – Prepare For Your First Purchase

“If I had only five minutes to chop down a tree, I’d spend the first two and a half minutes sharpening my axe.” – anonymous woodsman

Worthwhile results don’t happen by accident. They take careful preparation. So, in this Trade-Up Plan, you have two years to prepare before your first purchase. The preparation tasks include:

- Save cash

- Study your target market

- Prepare purchase financing

- Hunt for deals

I’ll briefly explain each task below.

Save Cash

This plan makes use of debt leverage, which means you don’t have to save up 100% of the costs of purchasing the real estate. But you still need some cash to get started.

The up-front cash needed in this example will be $34,000. It will be split like this:

- $27,000 for a down payment

- $3,000 for closing costs

- $4,000 for a minimal reserve (which will increase each month as you collect rental income)

You have two years to raise the upfront cash. I assume this is enough time for you to come up with the cash.

But it’s possible you already have the money, which means you can start faster. And if you begin with a larger amount of cash than $34,000, you could also buy more rental properties in the beginning. If done well, this could lead to an even faster path to your desired financial results.

But I’m assuming you don’t have the upfront cash. So, where could you get it? Here are some ideas:

- Cut personal expenses to increase your savings rate

- Work overtime and earn bonuses at your day job

- Sell personal items (i.e. yard sales, eBay, etc)

- Sell assets (cars, other investments, other properties)

- Flip a house

- Sell your principal residence to capture equity. Then downsize and/or rent.

- Borrow money on a HELOC (home equity line of credit) – I’d use this as a last resort. If anything goes wrong you are also risking your personal residence. Plus, you have to make monthly payments on the borrowed cash.

- Bring in a partner – Partnerships add complexity and risk from potential break-ups. Enter them carefully (like a marriage). Partnerships also reduce your share of the profit on the back-end. But if you don’t have the cash and/or credit, part of something is better than all of nothing.

I’m sure there are other options. The main point is that if your financial independence is important, you’ll find a way to raise the cash. And even if it takes longer than two years, the principle is the same. Just stick with it.

Study Your Target Market

In the example, you immediately begin studying your target market. If you hadn’t chosen a target market, you use my Comprehensive Guide to Pick the Ideal Location For Investment Properties to learn and get focused.

In order to make educated purchases, you know you need to understand the rental market very well. So, you specifically focus your market education on:

- what tenants like

- what tenants don’t like

- the supply of rental units

- rental rates

- how the rental market is changing (up, down, flat)

You also study the overall resale market for investment properties. You learn about sold properties as well as properties actively for sale on the market. Then, you confirm if your plans are possible in this location. If they’re not, you adjust the plan or you move it to a different location. You also learn the best (and worst) neighborhoods and streets to invest in within your market.

Prepare Purchase Financing

Financing terms and qualification criteria change like the wind. And they’re sometimes difficult to understand. So, you begin work on financing immediately.

You look for mortgage lenders for two different types of loans:

- conventional 30-year financing on 1-4 unit properties

- commercial financing on 5 units or more

These are two different lending worlds. So, you end up getting two different lenders. You find your lenders by asking for referrals locally and through online forums at BiggerPockets.com. You insist that your lender representative is someone who you get along with, who is responsive, and who will be honest. Mortgage brokers are notoriously over-optimistic. So, you want someone who will tell you the cold, hard truth throughout the process so that you can build your plan around those lending criteria.

You also work on non-traditional financing options like loans from private lenders or selling financing. My comprehensive BiggerPockets.com article about my five favorite creative financing techniques gives you a head start.

You finally get preapproval letters and firm commitments from your lenders so that you can begin to confidently make offers on properties.

Start Hunting For Deals

You start hunting for deals early because good acquisitions funnels take time to gain momentum.

An important part of this acquisition funnel is your relationships with local real estate brokers, wholesalers, and other referral sources. You also build a spreadsheet with the addresses and owner information for all of the investment grade properties (smaller and larger multiunits) in your target location. This list allows you to send letters and reach out to owners directly about buying their properties.

You get started with deal finding ideas by listening to my Bigger Pockets podcast interview 7 Ways to Find Incredible Real Estate Deals.

End of Year 2 – Purchase Duplex

You finish your preparations and hustle for two years. This hard work pays off because at the end of year #2 you purchase your first duplex!

Hooray! Happy dances and celebrations ARE allowed!!

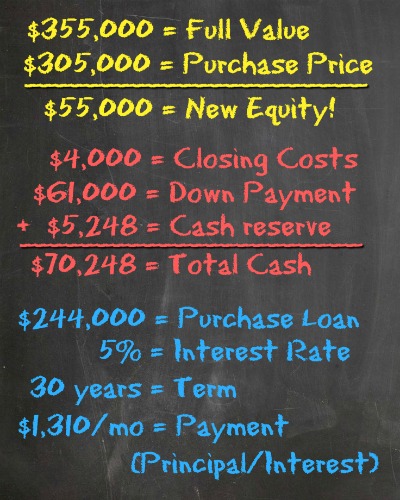

The purchase and financing numbers for your duplex purchase look like this:

Years 3 & 4 – Collect Rent & Sell Duplex

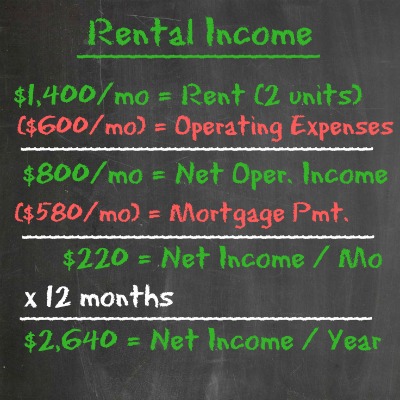

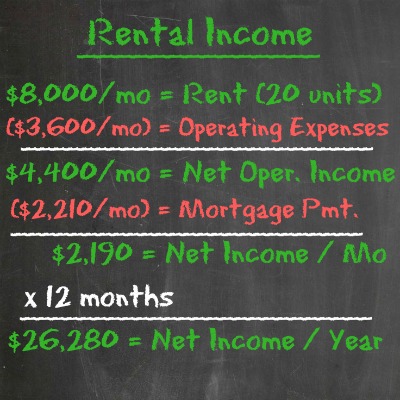

The duplex was already rented, but you raise the rent some to improve its overall performance as a rental. The rental operating numbers of your duplex look this:

Because the rental income is sheltered by depreciation, you pay no taxes on this rental income. So, for two years you collect rent and save 100% of the rental income. This equates to $5,280 savings over two years.

You also save $10,000 per year or $20,000 over two years by working your day job and reducing your personal expenses.

These cash savings are important because you’ll need the extra cash for the next purchase.

During this holding period, you also look for the next purchase. One of your letters to a rental property owner pays off. You find a 4-plex owner willing to sell at an attractive price, and she’ll give you an option to purchase for 6 months (you pay a $10,000 non-refundable option deposit in exchange). The option period gives you time to put your duplex on the market and sell it, and the $10,000 option fee is credited towards your purchase price at closing.

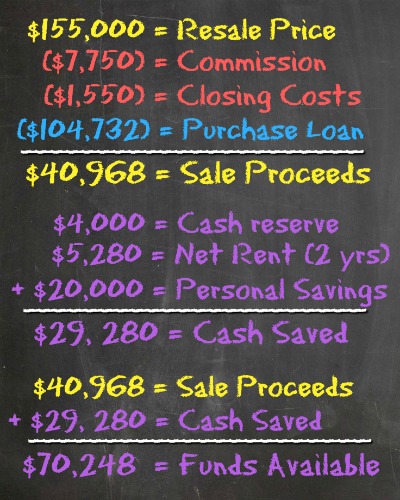

You put the duplex on the market with a real estate agent. You agree to pay a 5% commission at the time of sale, and you also budget 1% for seller closing costs. When the property sells, you hire a 1031 exchange intermediary to handle the details of the tax-free exchange.

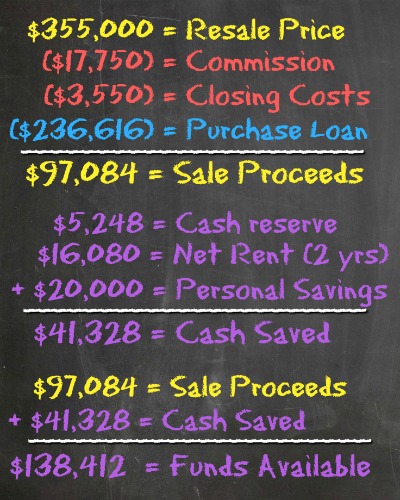

Your duplex sells relatively easily. At the time of the sale, your funds available for the next purchase look like this:

End of Year 4 – Purchase 4-Plex

You execute the sale of the duplex and the purchase of the 4-plex right after one another. Using the proceeds from the duplex sale, your 4-plex purchase numbers look like this:

Years 5 & 6 – Collect Rent & Sell 4-Plex

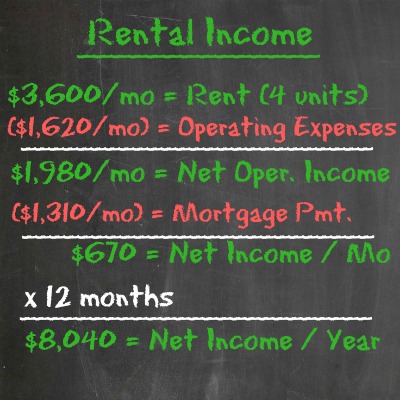

Like the duplex, your 4-plex was already rented. But you again raise the rent to improve its overall performance as a rental. The rental operating numbers of your duplex now look this:

You again pay no taxes on this rental income because of depreciation shelter. So, for two years you collect rent and save 100% of the rental income. This equates to $16,080 in savings over two years.

You also continue your trend of saving an extra $10,000 per year or $20,000 over two years.

As you collect rent and save cash, you once again work hard to find a new property to purchase. This time you find a 20-unit building listed with an agent. It’s a big jump from a 4-plex, but it meets your criteria perfectly.

In the meantime, you also follow up with your commercial lender who has preapproved you for a larger, commercial loan.

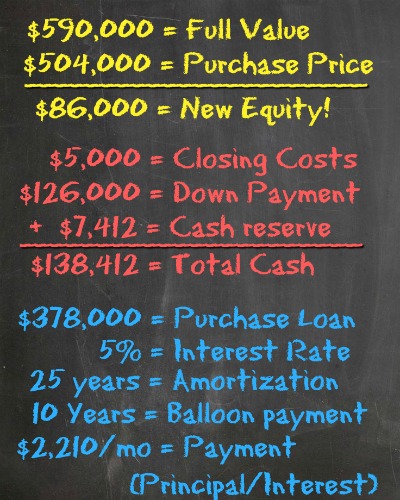

The negotiation for the 20-unit is tough, but the seller finally agrees to a deal. You give the seller an option fee of $15,000, and he gives you the right to purchase the building for a price of $504,000 for a period of 6 months.

Now you put your 4-plex on the market to sell. Your same agent charges you 5% and you budget 1% for seller closing costs. And your same 1031 exchange intermediary agrees to handle the details of the exchange.

Your 4-plex quickly sells to an eager new investor who wants to do a house hack after reading my House Hacking Guide. Your sale proceeds look like this:

End of Year 6 – Purchase 20-Unit

You execute the sale of the 4-plex and the purchase of the 20-unit right after one another. Using the proceeds from the 4-plex sale, your 20-unit purchase numbers look like this:

Years 7 & 8 – Part 1 – Collect Rent & Save More Cash

Your rental experience with the duplex and the 4-plex payoff. You’re able to raise rents on the 20-unit. You also find expense savings by negotiating down the tax value to reduce your tax bill. These all contribute to an increased overall value of the 20-unit complex.

The rental operating numbers of the 20-unit look like this:

The net rental income on the 20-unit is $26,280 per year, which is much greater than the duplex or 4-plex. While this is a nice problem, it also exceeds the depreciation tax shelter provided by a typical, straight line depreciation schedule.

So, you decide to perform a simple cost segregation study. To do this, you identify personal property and other short-lived parts of the property that can be depreciated faster (thus providing more current tax shelter). For example, all of the appliances, HVAC units, hot water heaters, carpets/flooring, etc have shorter expected life spans than the typical 27.5 years for residential real estate. With the help of your real estate CPA, you use this extra depreciation to shelter 100% of your rental income from tax. This allows you to save 100% of your net rental income.

You also of course personally save your $20,000 during the two-year holding period.

Years 7 & 8 – Part 2 – Control the Next Deal & Sell 20-Unit

This time around you already had your eyes on your next purchase just a couple of months after purchasing the 20-unit. The new property is a 30-unit complex in the same neighborhood as your 20-unit. You meet the owner, an older gentleman, one day while you were out walking around your property.

After getting to know one another, you negotiate a master lease option with the 30-unit owner. This means he rents the entire 30-units to you, and you sublease each unit separately to individual tenants. You also get an option to purchase the property for $850,000. Your master lease effectively removes the owner from having to manage the property day-to-day.

The owner does this master lease because he is motivated to get rid of headaches associated with the property. He has begun to neglect it over the last few years. The owner also trusts you, and trust is the ultimate bank account.

Your master lease is not a huge money-maker. In fact, it just breaks even during the holding period of 1.5 years. But it accomplishes your goal. It ties up the property until you can sell the 20-unit. And it allows you to begin improving the property, the tenants, and the rents in preparation for your ultimate purchase.

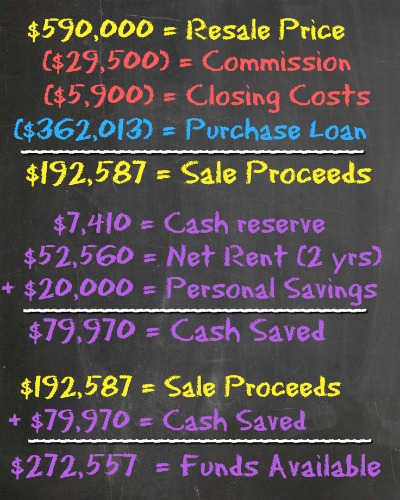

Once you tie up the 30-unit, you put the 20-unit building on the market. Unlike the duplex and 4-plex, the 20-unit takes longer to sell. But after 9 months of marketing, you find a buyer. Your same agent charges you 5% and you again budget 1% for seller closing costs. And your same 1031 exchange intermediary agrees to handle the details of the exchange.

Your sales proceeds from the 20-unit look like this:

End of Year 8 – Purchase 30-Unit

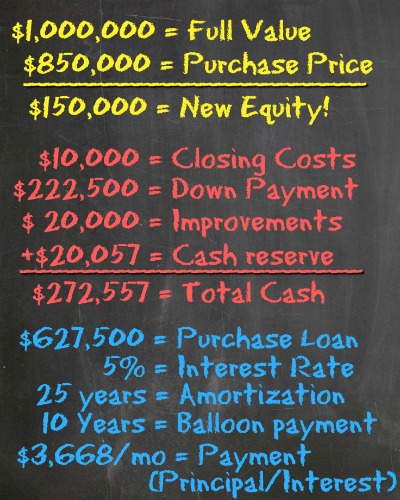

You’ve sold your 20-unit! And just like before, you use the proceeds from the sale plus your cash savings to purchase the 30-unit property with the help of your 1031 exchange intermediary.

Soon after the purchase, you spend $20,000 on some minor exterior upgrades (new roofs, landscaping). These and the other efforts you made during the master lease period improve the profitability and the value of the property.

Here are the numbers from the purchase of the 30-unit building:

Final Results of Trade-Up Plan Example

The last eight years required a lot of focus, planning, and determination. But the results have been worth it.

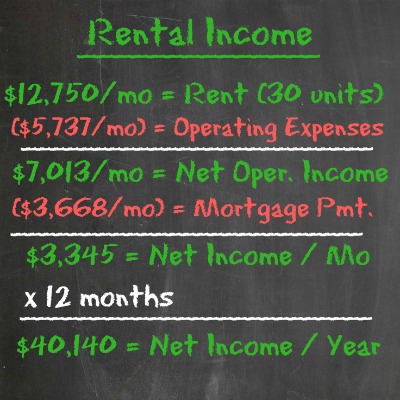

You began with very little savings, and you now own a 30-unit, 1 million-dollar rental property that produces over $40,000 per year in net rental income with $372,500 in equity!

Here is the calculation for the rental income for the 30-unit property:

You could now take a rest and just enjoy the fruits of your labor. I’d personally suggest my favorite between-goal break – a mini-retirement. But if your financial independence number is $40,000 or less, maybe it’s time to make a major, permanent shift in your life. After all, that’s what your financial results are for!

But it will also be time to think about the big picture. What do you really want? What are the next steps? And are the current financial results enough?

Is This Good Enough?

I wrote an article on Bigger Pockets that basically said a massive real estate empire won’t give you the life you imagined. The point was that bigger isn’t always better. You need to identify “enough” for yourself and stop there. A relatively small portfolio can give you everything you want financially (enough) with the lease hassle and risk.

But I deliberately made a key definition fuzzy. What’s “bigger” or “massive” mean? Ten units? Fifty units? One thousand units?

The answer depends on you, your definition of financial independence, your business skills, and the other motivations that drive you.

So, the key questions of this entire example go back to you. Is this investment good enough for you? And what makes an investment good enough?

I personally like to look at both the investment’s ability to make money and its inherent risk. You can use these two criteria with the 30-unit property.

Money

The 30-unit property produces over $40,000 per year. For me and many others, this would actually be plenty to pay for a minimum required lifestyle. And with the principal pay down and potential rent appreciation, it will likely get better over time.

But if you wanted more, you’d need to take some additional steps. I’ll share a couple of ideas to accomplish this below.

Risk

What can possibly go wrong to spoil this investment? That’s a risk question.

And in this case, the biggest risk that stands out to me is the debt. The $627,500 loan has a balloon note after ten years. What if you can’t refinance at that point? You’d risk losing everything. I actually saw this happen during the 2008-2009 economic crisis.

And even if you were able to refinance, what if during the next ten to twenty years the economy experiences a major deflationary cycle like the Great Depression of the 1930s? You’d again risk losing everything if rents could not cover your expenses.

On the flip side, during a major inflationary cycle, your 30-unit with a long-term debt would actually be in great shape. Your rent would likely continue to increase while your payment would remain fixed. And you’d pay back the principal with much cheaper dollars.

So, if you are satisfied with the 30-unit in terms of money and risk, you’re free to move on with your life. If I was able to refinance with a fixed-rate, non-recourse mortgage for 20-25 years, I would probably be ok with the other risks given the overall benefits.

But if the money or the risk are not good enough in your case, you may need to do a little bit more. Here are a couple of ideas for what you could do next.

Possible Next Steps After the Trade-Up Plan

To make more money and build more wealth, you could consider continuing to trade-up. After all, at this pace, you could own the Empire State Building and make $1 million per month with just a few more trades!

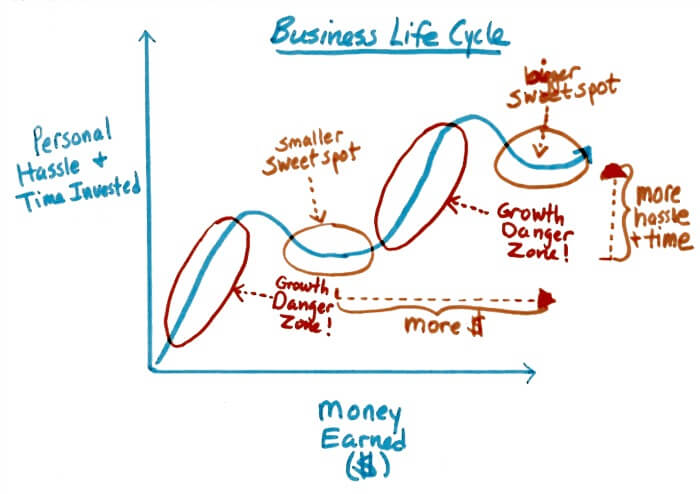

But managing continual growth is like being the captain of a ship that keeps getting bigger and bigger. You have to become much more diligent as the captain to continually check for financial leaks and other problems. Your ship’s bigger size makes this inherently challenging (although not impossible).

This diagram I made shows this reality of business growth as I see it:

Each step of the Trade-Up Plan brings greater rewards but also great risks and hassle. So, as an entrepreneurial investor, you have to decide when the risk outweighs the reward.

If you decide to trade-up another time or two, that’s certainly your prerogative. If you can manage the challenges, you’ll likely experience much greater cash flow and equity rewards.

But if you decide not to trade up anymore, you also have another solid alternative. You could transition to debt acceleration and payoff, much like I wrote about in the Debt Snowball Plan. You could use the extra rental income and job savings to make enormous mortgage payments and cut the total loan term down significantly.

In 7-10 years it’s possible you could own the property free and clear of debt. Many commercial mortgages have prepayment penalties, so you’ll have to negotiate or find a lender without the penalty up front.

But in the end, your free-and-clear property would produce over $84,000 per year in rental income (assuming no rent appreciation)! And you’d have lower risk and more flexibility with no debt on the property.

I’m sure there are other variations or alternatives you could pursue. But I hope this detailed example has given you some ideas to think about.

Closing Thoughts

You’ve made it to the end of the Trade-Up Plan. I showed you how the basic plan works, and I gave you an example of the plan applied to a real-life situation.

As you can see, the Trade-Up Plan has real potential to accelerate your financial goals. But it also has real challenges. I see it as a plan for the more entrepreneurial real estate investors who can juggle the demands of deal finding, financing, and transaction details in order to reach the attractive end result.

Please remember that my detailed example was not provided as a recipe for exactly how the plan will work in your life. The example is meant to make the concept come alive. But the specifics will never be exactly the same as your situation. It’s the principles and the core benefits that matter.

My primary goal is to get you thinking. I want you to expand your possibilities and your toolbox of options. And I want you to have hope that a plan to achieve your financial independence exists. I then trust that you’ll use your own intelligence and creativity to learn more and to turn these ideas into reality for yourself.

I wish you all the best with your real estate investing!