How to Calculate Rental Property Cash Flow – A Comprehensive Guide

Investors don’t decide to buy properties; they decide to buy the income streams of the properties.” – Frank Gallinelli

Some rental buildings are beautiful. I particularly admire well-constructed, brick structures with hardwood floors and large, dry crawl spaces. But the building only matters indirectly for rental property investors.

The beauty of the building is relevant if it attracts good tenants who pay you rent consistently. Then that rental income stream can be used to cover your expenses, produce cash flow, and increase your bank account balance.

Cash in the bank. Ahhh. Isn’t that also beautiful?

It’s like a pristine mountain stream that continually provides nourishment to your business and to your life. It pays your bills. It helps you pay off your mortgages. And it gives you a resource to reinvest and grow your pool of investments to a point of financial independence.

But this beauty of cash flow from real estate is elusive. Not all properties produce it equally. And too many investors ignore the steps required to calculate cash flow up front.

When this happens, you invest with your eyes only half-open. And negative or sub-par cash flow tends to follow you for years.

I know this from first-hand experience!

I hope to remedy that situation in this article. I’m going to show you the most common ways to calculate real estate cash flow so that you can recognize it and seek it out from your investments.

The Financial Waterfall

You can think of the flow of cash real estate sort of like a waterfall. The investor (you) is at the bottom. Here’s what that waterfall looks like:

- Collect rent

- Operating expense payments (taxes, insurance, maintenance, etc)

- Capital expense payments (replace roof, heat-air system, etc)

- Mortgage payments

- Income tax payments

- Pay owner/equity partner

That’s a long waterfall, isn’t it? There are a lot of opportunities for that precious cash flow to be diverted away from you.

Since the goal of real estate investing is to pool as much cash as possible at the bottom of the waterfall, it’s critical to understand and correctly calculate all of the prior steps. This will help you negotiate the right price and financing terms that ensure a steady stream of cash flow to you for years.

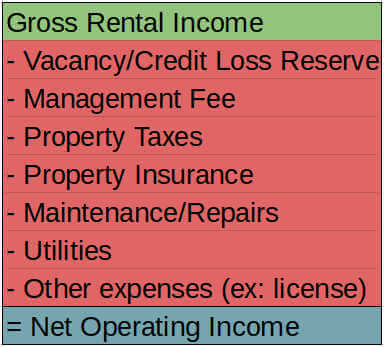

The first cash flow calculation is Net Operating Income.

Net Operating Income

Net Operating Income (aka NOI) is the foundational formula used to calculate rental property cash flow. I have an 11-minute YouTube Video that explains this concept in detail, but I’ll also briefly share it with you here.

NOI tells us the income left over after paying all of our every-day rental expenses (not including financing). These are called operating expenses, and they include things like vacancy reserves, management fees, property taxes, insurance, and maintenance.

The formula for NOI looks like this:

These operating expenses are items you will likely write checks for some time during the year. Without paying these expenses, you would not be able to operate and rent the property.

But notice the expenses this formula does not include, like mortgage costs and capital expenses. Mortgage expenses vary for each investor depending upon the financing amount and terms. Capital expenses are something I’ll discuss more later in the article.

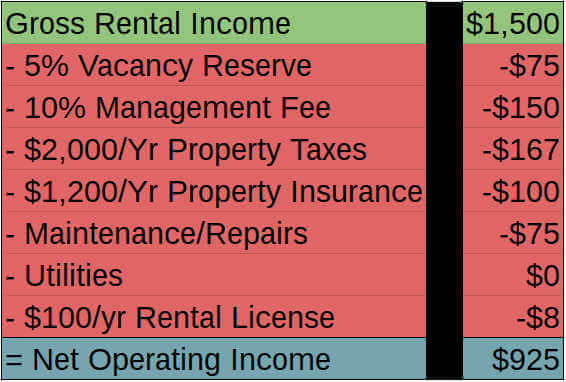

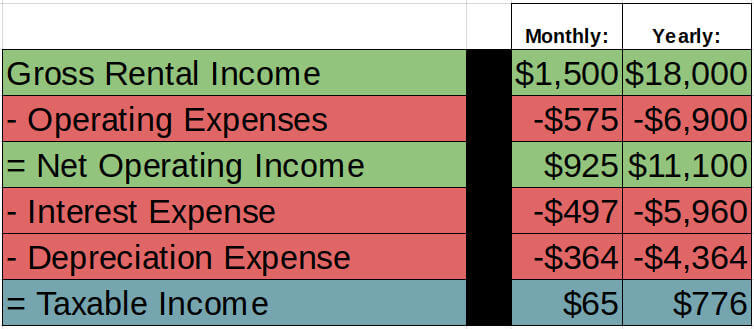

An example with real-life numbers might be a house that rents for $1,500 per month. Here is a possible monthly net operating income calculation for that property:

NOI is helpful because it begins to tell us how much cash flow we have available to pay lenders and equity partners. But as you’ll see in the next section, the normal calculation for NOI is missing one critical ingredient.

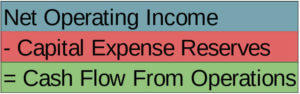

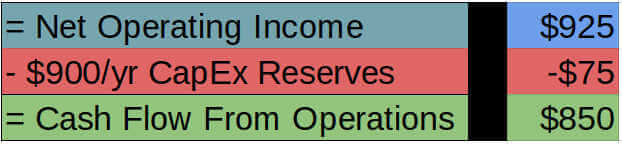

Cash Flow From Operations

While net operating income is important, its close cousin cash flow from operations (CFO) more accurately tells you what you need to know as an investor.

Here is the formula for cash flow from operations:

For commercial investors, this definition would also include deductions like leasing commissions and tenant improvements. But for those of us in the small residential investing world, the important thing to include are capital expense reserves.

What are capital expenses (aka CapEx)? They are THE real-life expenditure I see ignored by real estate investors more than any other at the time of purchase. CapEx includes the large expenses like roofs, heat-and-air systems, driveways, and other structural items.

These items wear out over time and must be replaced. And when this happens, it’s not a small check you must write! It’s the kind of event that can empty your bank account if you have multiple properties needing the same repairs.

So, in order to avoid cash flow catastrophes, use this formula below to budget for future capital expenditures. And then set up a reserve savings account where you deduct the CapEx reserve just like you would any other monthly expense.

Trust me – you will be VERY happy that you did this!

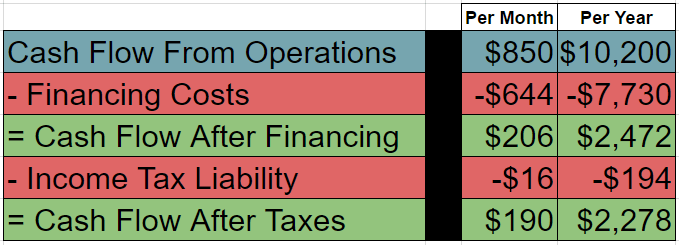

Here is an example of the monthly cash flow from operations using the same single family house. I’ve included a $900 per year or $75/month capital expense reserve. This may or may not be enough. If you want to dig in further to CapEx budgeting, read this article by my friend Brandon Turner at BiggerPockets.com.

With cash flow from operations calculated, you can now proceed to figure out how much you can afford to borrow against the property and how much cash flow you’ll actually put into your bank account.

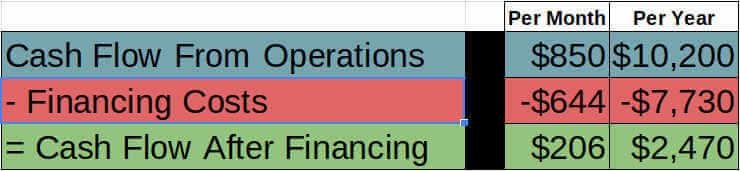

Cash Flow After Financing

Although free and clear real estate can be a wonderful thing, most investors start off using borrowed money to purchase real estate. So, the cash flow our property produces will be used to make regular payments to our lender.

In order to ensure you have enough cash flow both to pay your lender AND to pay yourself, you need to figure out cash flow after financing. Here is the formula:

This is a simple formula. The only real effort is calculating your financing cost, and there are a couple of different ways to do that.

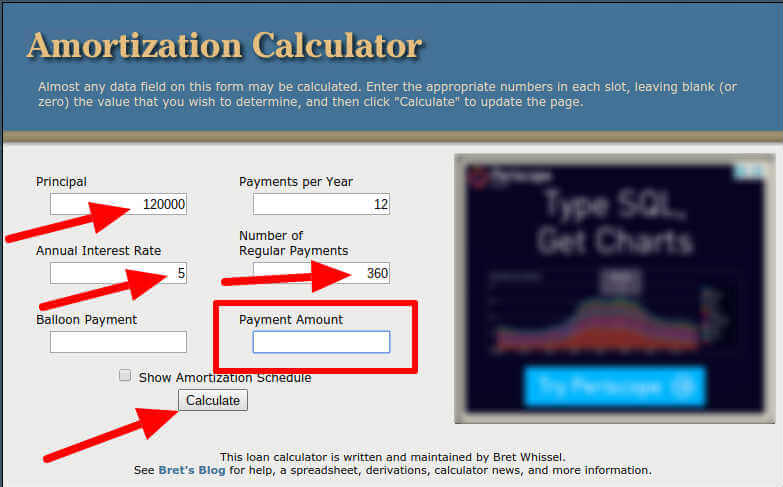

If you have an amortizing loan where it automatically pays down over a period of time like 30 years, then you can use a loan calculator. Here are a few resources that may help:

- http://bretwhissel.net/amortization/amortize.html – simple and helpful – my go-to loan calculator for years

- http://www.fncalculator.com/ – the app I use for my android phone (also available for iPhones)

- http://www.calculator.net/loan-calculator.html – another helpful online calculator

Here’s an example to show how you might use this while analyzing a prospective rental purchase.

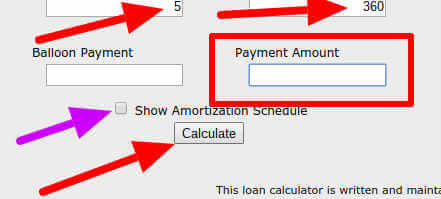

Let’s say the asking price of a property is $150,000. Your lender requires 20% down on a loan at 5% interest for 30 years. This means at most you can borrow $120,000 (80% of $150,000).

You would then enter $120,000 and the other loan information into your loan calculator in order to get the monthly payment. The steps are illustrated below:

The result given by the calculator will be your monthly payment on the loan. This will be both principal and interest.

In this example, the payment amount is $644.19 Now you can calculate the cash flow after financing.

This means you will put $206 per month or $2,470 per year into your bank account. Does that mean you’re all finished? Can you swim in your pool of cash yet?

Actually, there is one more buddy who gets angry if he’s forgotten. That’s big ‘ol Uncle Sam the tax man:).

Cash Flow After Tax

So far you’ve paid all of your operating expenses, your capital expenses, and your lender, but you’ve still got to pay income taxes before you can figure out what YOU get to keep.

The final calculation, then, is cash flow after tax. It will take a couple of steps.

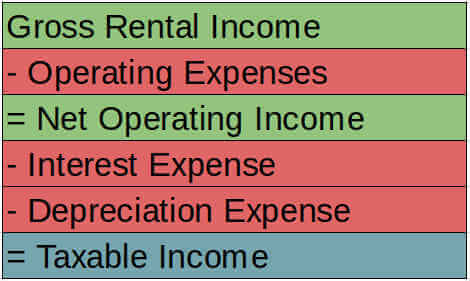

First, you need to figure out how much of your rental income is taxable. Here is the basic formula.

Taxable income is different than our prior calculations, cash flow from operations or cash flow after financing. It’s different because not everything you spend cash on is a taxable expense. For example, capital expense reserves and mortgage principal both cost you cash but are not deductible on your taxes.

Taxable income is also different than cash flow because you can deduct some expenses, like depreciation, which don’t actually come out of your cash flow. Instead, depreciation is a “paper loss” which means it could make your taxable income less than the actual cash flow you receive. This is a good thing!

To calculate depreciation, you must know your cost basis for the physical building you own. According to the IRS, land does not depreciate in value, so we must separate the land and building costs before calculating depreciation.

In the single family house example, let’s say $120,000 of the $150,000 house purchase was building and $30,000 was land. This is residential property, so as of this writing the IRS requires you to depreciate $120,000 over 27.5 years.

To calculate depreciation, we take $120,000 / 27.5 = $4,364 in depreciation expense per full year.

Hold that number in mind while we calculate the second expense of this formula, interest.

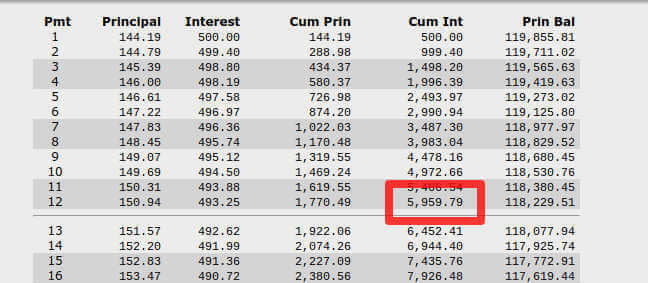

Interest expense is just the portion of your mortgage payment that goes towards interest. In our example of a loan for $120,000 at 5% interest for 30 years, the first year of interest will be about $5,960.

You can use the same amortization calculator I recommended earlier to calculate this. Just click the checkbox for “Show Amortization Schedule,” which I’ve pointed out with a purple arrow below:

Once you press the Calculate button, a schedule will show you the interest paid in the first year.

Now that you have the depreciation and interest expenses, it’s possible to calculate taxable income. Here is the full calculation for the example:

Interestingly enough, your taxable income is only $776 per year even though the cash flow in your bank account (cash flow after financing) is $2,470 per year! This shows the effect of the depreciation expense to shelter your rental cash flow from taxes.

Now for the final step, you need to finally calculate what’s left over after paying your income tax bill.

Just assume the tax bracket for the income in this example is 25%. That means the taxes owed will be 25% of the taxable income.

So, 25% x 776 = $194. That number is your income tax owed.

Now you’re ready to make the FINAL cash flow calculation. Using the numbers from the example here is the final cash flow after tax:

The Power of Real Estate Cash Flow

The point of the step by step calculations in this article was to help you understand the details of cash flow produced from your rental properties. I hope you’ll use the formulas shared here as tools to pick apart and analyze any investment you may own or are looking to purchase.

But more than everyday tools, these cash flow concepts also start revealing the bigger picture strategies of wealth building in real estate.

For example, did it strike you that the effect of income taxes on your rental income was relatively minor in the illustration above? Assuming you are an employee taxed at 32.65% (25% income tax and 7.65% for social security and medicare tax), you would have to earn MUCH more than the $2,470 cash flow after financing in order to end up with the same cash. This is true because you only keep 67.35% (100% – 32.65%) of each dollar earned on the job.

On the other hand, you kept 92% of your cash flow after financing ($2,276/$2,470) from the rental property. To put the same amount of cash in the bank from your job, you’d need to earn $3,379 ($2,276 ÷ 67.35%). For a family that makes $7,000 per month, this is the equivalent of working half a month.

So, if you own 12 rental properties like this example, you could put $27,312 in the bank (12 properties x $2,276 cash flow after tax). That is the same cash flow after tax as working half a year at a full-time job. Rental properties certainly require some effort, but I can tell you from first-hand experience that you can self-manage 12 rental properties very easily compared to a full-time job.

If rental properties interest you, the payoff will be worth the effort of getting started. The financial advantages I’ve shared here and the many other advantages of investing in real estate make it an ideal choice for wealth building and long-term cash flow generation.

Did you find these cash flow formulas helpful? Do you use any of these cash flow calculations in your own rental property investing? Are there other formulas that you also use?

I’d love to hear from you in the comments section below.

Photo Credit: Waterfall Picture – By the original uploader Weihao.chiu at Chinese Wikipedia – Transferred from zh.wikipedia to Commons., CC BY-SA 3.0, https://commons.wikimedia.org/w/index.php?curid=1392471