Financial Independence Using Real Estate Investing – A Case Study

Invest in real estate. Retire early. Do what matters.

That is the 3-sentence mantra here at coachcarson.com. Most of my writing focuses on the first part, as in the practical, detailed real estate techniques and strategies that you can use and apply right away. But today I’m going to begin from the end. I’m going to share an example of what early retirement (aka financial independence) is really like for someone who chooses real estate investing as their primary investment vehicle.

The people in this story are not real, but I’ve taken many of the details from real people who I know first hand. I hope this helps you to visualize the destination of financial independence at the end of your hard work. And I hope it shows that your current efforts are worth it!

Let’s jump in!

A Not-So-Ordinary Day

Marcus and Tiffany can’t help smiling today. In some ways, this day is like any other for the 45-year old couple from Raleigh, North Carolina. They wake up, exercise, eat breakfast, talk to their teenage children before school, and head to work.

But behind the ordinary routine, the couple knows they are on the cusp of a new era financially. It’s their real estate portfolio that has them smiling. Today they will reach a major milestone as they pay off one of the last debts on their 11 rental units and reach their free and clear real estate goal.

But Marcus and Tiffany don’t plan to immediately make any major life changes even though they’re now financially independent. They actually enjoy the current routine of watching their children’s activities, volunteering in the community, and working in their backyard garden.

On the surface, Marcus and Tiffany appear the same, but their journey over the last 15 years has built a secret confidence within them. A decade and a half ago they set a challenging goal to become financially independent by age 45. Now as they reach their milestone, they know that anything is possible.

They have money in the bank, equity in real estate, and most importantly – self-reliance in their souls! And financial independence will open up new doors never possible before.

Motivation For Financial Independence

When Marcus and Tiffany began their journey to reach financial independence, they were not unhappy with their careers. Marcus worked in sales, and Tiffany was a nurse. They enjoyed their jobs, and financially they were comfortable, together earning over $100,000 per year.

But they were skeptical that they’d feel the same way in a decade or two. The idea of a typical path of “making a dying” for 30-40 years scared them. They could not see themselves doing the same thing for the rest of their working lives.

This ambitious couple wanted security just like everyone else, but they also valued autonomy and flexibility. Marcus and Tiffany wanted control over the timing and the pattern of their lives. Using traditional investment vehicles like stocks to reach financial independence worked for some people, but for them, it did not take advantage of their personal entrepreneurial skills. And the timing depended on too many things outside of their control.

Instead, Marcus and Tiffany decided to use the vehicle of real estate investing. They planned to build wealth and to eventually live off of the rental income from their properties.

Your Residence CAN Be a Good Investment

The journey of a thousand miles begins with a single step.”

Lao Tzu, Tao de Ching

Because they lacked any savings other than an emergency fund, Marcus and Tiffany began modestly by simply thinking differently about their personal residence. They bought and moved into a series of three discount-priced, well-located foreclosure houses over a period of 6 years. In each case they waited two years, fixed up the property, sold it to realize their tax-free gain, and reinvested all of their cash into the next property. Using this live-in-flip method they ended up with their dream residence worth $350,000 and no mortgage debt.

Some people would have been satisfied with this accomplishment. But this couple had bigger aspirations.

So, they pulled out $280,000 using a 15-year, 3%, $1934 per month mortgage, and they used this capital to begin their accumulation of rental properties.

A Real Estate Mini-Empire

During their 6 years of fixing and flipping their residence, Marcus and Tiffany studied and learned a lot about other types of real estate investments in their market. They liked single family home rental properties, but about the time they refinanced their home, they stumbled upon a deal on a small mobile home park that they could not pass up.

For $100,000 they paid cash for a 2-acre parcel that was zoned to allow 6 mobile homes. The current landlord had neglected the property. Three of the six mobile homes were vacant and practically falling apart, and the remaining three newer mobile homes had tenants who did not pay on time or respect the property.

With some time, energy, and $50,000 of extra capital, Marcus and Tiffany turned the mobile home park around. They improved the curb appeal of the park as a whole, they bought 3 new mobile homes to replace the three old ones, and they found new tenants for all 6 homes.

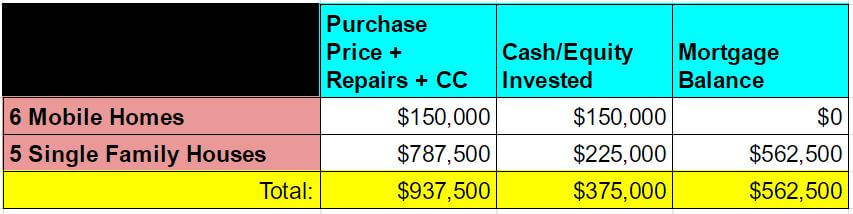

Their sweat equity and $150,000 total investment paid off. Once stabilized, their financials for the 6 mobile homes looked like this:

The land under the mobile home park also held potential someday because growth from town continued to move that direction. Eventually, the land might be repurposed as a commercial parcel and sold for a much higher price.

While they liked the mobile home park, Marcus and Tiffany saw more purchase opportunities locally with single family houses. So, they began the next phase of their growth looking for houses to purchase.

Moving on Up to Single Family Houses

Finding bargain house purchases wasn’t as easy as waiting for deals to fall in their laps. But Marcus and Tiffany’s experience had taught them that a whole lot of hustle combined with deliberately building competitive advantages inevitably led to consistently finding good deals.

Using the remaining cash from their home refinance, additional savings from their jobs, and reinvestment of the mobile home cash flow, the couple proceeded to purchase five single family houses in the next couple of years. The houses were in high-demand neighborhoods and rented easily for $1,500 per month.

The houses cost Marcus and Tiffany $150,000 each for a total price of $750,000. They made a 25% down payment on each property and spent an additional 5% for financing and other costs. So, at $45,000 per property (30% x $150,000) they had $225,000 cash invested in the houses. When added to the $150,000 mobile home park investment, their total investment of capital thus far was about $375,000.

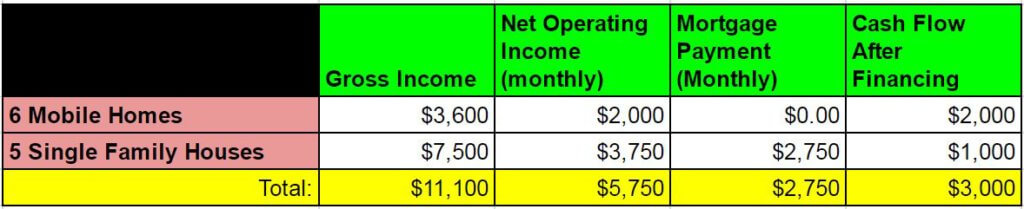

Their current financials from all of their properties looked like this:

With this simple portfolio – one small mobile home park and five single-family houses – they now proceeded to the final leg of their journey towards financial independence.

The Transition From Growth to Financial Independence

Taking the foot off the growth accelerator is a difficult transition for ambitious entrepreneurs to make. Once you realize there are always more good deals out there, it’s tough to stop accumulating more. And it’s difficult to convince yourself that enough is enough.

But Marcus and Tiffany remained focused and self-disciplined. They knew why they began this journey in the first place, and they were ready to transition to a new period of their lives with more free time and flexibility while their kids were still in the house.

Although their jobs produced $100,000 per year, Marcus and Tiffany’s family living expenses were much more modest. Not including their home mortgage, $5,000 per month from investments could easily give them a comfortable lifestyle for the rest of their lives.

So, instead of replacing their income at this stage, the couple made their goal to safely cover the $5,000 per month overhead using rental income.

Making Snowballs for Fun and Profit

As you saw in the spreadsheet in the previous section, their investments already made $3,000 per month positive cash flow (mobiles $2,000 per month, houses $1,000 per month). Instead of growing more to increase their cash flow by $2,000, Marcus and Tiffany decided to keep things simple and just pay down debt on their existing rentals.

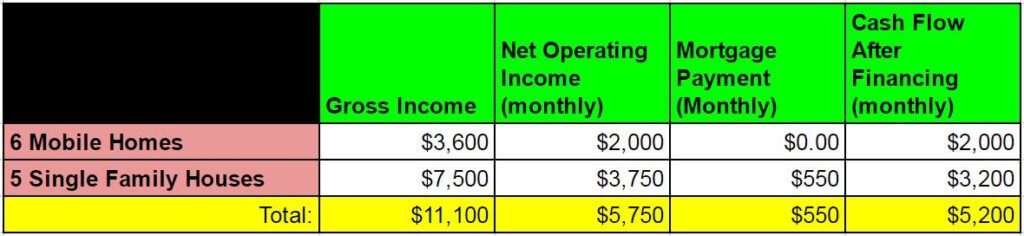

They used a snowball plan, which combined all of the cash flow from their mobile home park, rental properties, and extra job savings to attack one debt at a time. Within five years they had paid off the remaining debt on four of the five rental houses. They decided to leave in place the long-term, low-interest mortgage on the 5th house to let it continue to pay down and build equity.

The financials from their rental portfolio now looked like this:

As you can see, after approximately 15 years Marcus and Tiffany’s rental portfolio now meets their goal of $5,000 per month income. It’s also worth mentioning that the 15-year mortgage on their residence is set to full amortize to zero at about the same time and save them an additional $1,934 per month.

We’re now back at the point where this story began. Can you see why Marcus and Tiffany were smiling on that not-so-ordinary day?

Management Responsibilities & Passive Income

For those of you brand new to real estate investing, the prospect of owning 11 rental units may intimidate you. It’s true that management of real estate, even with a management company, is never a completely passive project. It does require some attention and time.

But Marcus and Tiffany learned that this real estate side business is MUCH easier than any other job they could imagine. And because they have help from a management company, they are even more free to be flexible with their time and location.

Each month their management company automatically deposits the net rent proceeds into Marcus and Tiffany’s bank account. The manager also sends them a report showing the rent collected and any expenses deducted. The couple spends about 2 hours per month reviewing the report and entering the data into their bookkeeping software.

The management company handles all tenant calls, overflowing toilets in the middle of the night, and leasing of vacant units. Marcus and Tiffany do observe the company’s work to ensure it is done correctly. The management company sends them pictures and a report twice per year from internal inspections of each of the properties. And Marcus or Tiffany personally ride by the units to make sure they are clean and in good shape.

But overall, the stabilized real estate business only requires 2-10 hours per month of their personal time. And should the couple want to travel for extended periods of time, they can work from anywhere they have a laptop and an internet connection.

The Emotions of Financial Independence

Is reaching financial independence like winning the lottery with celebrations, balloons, and a ticker tape parade? Not exactly.

The truth is a little more anticlimactic.

Humans are creatures of habit, and Marcus and Tiffany are no different. As disciplined goal-setters and planners, they have a hard time fully accepting their achievement. The possibility of immediately setting a new goal and continuing their march into the future tempts them.

Self-doubt and a hard-wired need for security creep into their thoughts. Voices in their head scream “Is this really going to be enough? Do you think you’re smart enough or good enough to just unplug from the system when so many other people can’t or don’t?”

They even experience a little-discussed phenomenon called the freedom void. Because their lives have been so full and focused for many years, they actually become a little disappointed or depressed by the reality of their new freedom. Will they become bored? What will they do with their time?

But all of these roller coaster emotions are normal. After all, financial independence isn’t just a formula on a spreadsheet. It’s a personal growth experience. And Marcus and Tiffany will rise to the occasion just like they have before.

Life After Freedom

I inhale great draughts of space,The east and the west are mine, and the north and the south are mine.I am larger, better than I thought,I did not know I held so much goodness.Walt Whitman, Song of the Open Road

Marcus and Tiffany realize that their version of financial independence does not have to look like a fairy tale. And no one except themselves can judge the right path to take from here.

So, they begin with a decision to take a sabbatical or mini-retirement with the entire family for a couple of months the next summer. They’ll rent an R.V, visit national parks and other interesting locations, and even pick up a few baseball games at stadiums their sons would love to see.

When they return, Marcus may consider quitting his job or going part-time. Because he’s learned to love fixing-and-flipping houses, he’s had the itch to do beautiful renovations on a house or two per year in the older neighborhoods in their town.

Tiffany still enjoys her current job as a nurse, but she may request a change of schedule or even work part time. She could use a slower pace for a while.

There are so many possibilities now. But there will be plenty of time to discuss their future plans on their R.V. road trip. For the first time in a long time, they don’t know exactly what their future will bring. And while scary, it’s also very exciting!

Conclusion

I have just outlined Marcus and Tiffany’s 15-year journey to financial independence using real estate. Your life and real estate journey are certain to be different than the details I’ve just shared, but I hope you’ll also find some similarities.

Just remember that your goals and your plans don’t have to be perfect. Formulas are made for spreadsheets. Your life is organic and can’t be reduced to math. You will certainly change your approach to match reality many times along the way. And that’s ok.

But the forward motion spurred on by actually having a goal and a plan ARE completely necessary. I hope you’ll accept the challenge to create or update your own financial independence goals and plans starting today.

I also appreciate you allowing me to be your real estate investing guide and coach. I look forward to helping you retire early and do what matters in your life.