What’s Your Financial Independence Number? Here’s Mine.

Listen to or Download the Audio/Podcast Version of This Article

A financial independence number tells you when you’re free from the need to work. It’s basically a math equation, as you’ll see later in this article. But discovering your personal financial independence number is about much more than money or math. It’s about your life and what matters to you. And it’s about whether money supports your ideal life or simply suppresses your potential.

While I don’t believe money is the most important thing in life, I do agree with Zig Ziglar that money is reasonably close to oxygen on the “gotta have it” scale in today’s economic-centered world. A financial independence number is useful because it tells you exactly how much money you really need.

In the rest of this article, I’ll show you how to calculate your financial independence number. Plus, I’ll also even share my own number.

Money and the Ideal Life

You certainly need money to survive. But you also need money for opportunities to live a life that is more fulfilling, flexible, and fun. Money buys you food to nourish your body, but it can also buy you the time and flexibility to nourish your sould. It can give you freedom to become your best, to share your gifts with the world, and to do what matters.

Ahhh. Becoming your best self. Sharing your gifts. Doing what matters.

Those are the lofty ideals that I aspire to. Perhaps you have your own lofty ideals.

Whatever your personal ideals are, I bet they’re bigger than money. But as I realized soon after I graduated from college, simply trading my time for dollars wouldn’t lead to my ideals.

It’s not that working a job or running a business were bad things. Serving others with your time, energy, and skills can be incredibly fulfilling. But even a great job can become a drag when you know you must do it to earn money.

Instead of happiness and growth, a less than ideal job situation traps you like a rat running on a wheel. While most people call it making a living, you’re really on a long path called “making a dying.”

Luckily, there is a different financial path you can take. Instead of trapping you, this path creates more freedom and independence. Which brings us back to the financial independence number.

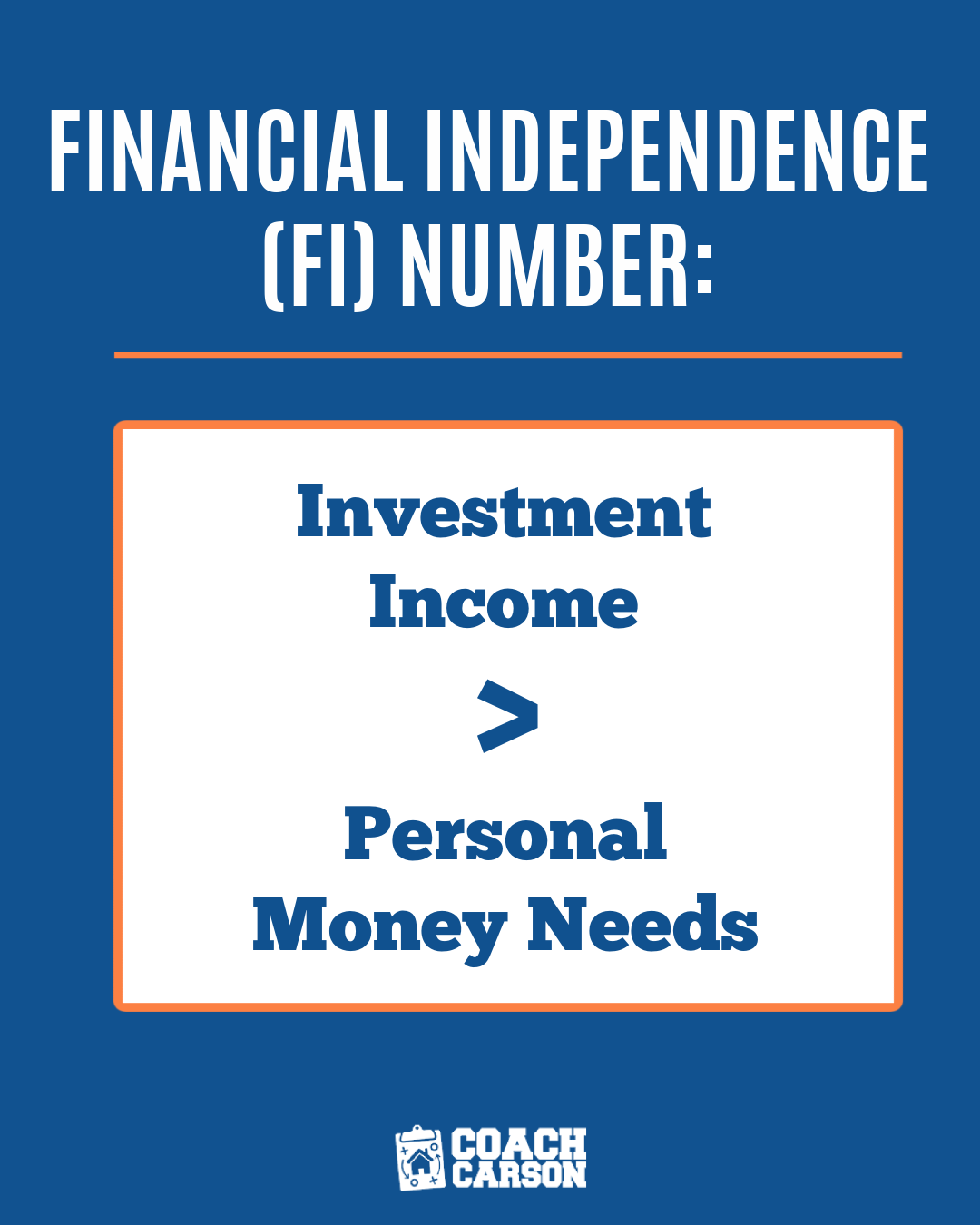

The Financial Independence Number Defined

Written as a formula, your financial independence number looks like this:

Investment income is the money you receive from investment assets like real estate, stocks, and bonds. When your investment income exceeds your personal money needs, you no longer need to trade hours for dollars in order to survive financially.

When you reach your financial independence number, you break the cycle of working for money. You draw a line in the sand beyond which you will no longer financially need a job.

Joe Dominguez and Vicki Robin in Your Money or Your Life call this line in the sand the crossover point. Robert Kiyosaki in Rich Dad, Poor Dad calls this leaving the rat race.

In the language of real life, this financial independence number means you could survive at a certain level only using the production of your investments. For example, your net income from rental properties would cover your personal overhead. Or with more traditional investments like stocks and bonds, the 4% rule for safe withdrawal may allow you to live off of 4% of your total holdings each year for a long period of time.

But before you begin hustling to accumulate wealth and income, let’s look at how to actually calculate your own financial independence number.

How Much Does the Ideal Life Cost?

The formula for financial independence may be simple. But actually squeezing all of your financial hopes, dreams, and insecurities into a math formula is challenging. If you’re like me, it’s a process you’ll continually tweak and update throughout your life.

But the financial independence number does not have to be perfect to be useful. Like any other goal, you can benefit from moving towards a goal even if the goal is just a reasonable guess.

So, how do make an educated guess for your financial independence number? How do you figure out the cost of your ideal life?

I like to begin with the present by calculating your current expenses. You can do this a couple of different ways:

- Estimate your expenses using something like these personal financial spreadsheets.

- Use software apps to automatically track your expenses. You simply enter your credit card and bank account info, and the software automatically tracks and categorizes your spending. Some of the most popular apps for this are mint.com (free) or YouNeedaBudget.com (paid).

Once you have an estimate of what you currently spend over a 1 year period, you can make a guess for the future.

Many people find that their personal expenses will actually go down after retirement. If you pay off your home mortgage before retirement, that obviously reduces one major expense. And you may be surprised how much you can save in taxes when you live off of investment income. My blogging colleague Jeremy at gocurrycracker.com has legally not paid income taxes for over 4 years after retiring early.

For more information to help you estimate your future expenses after retirement, I like the article How Much Will It Cost You to Live in Retirement by Darrow Kirkpatrick of caniretireyet.com. Darrow retired early himself, and he writes about the nitty-gritty financial details of retirement.

My own number may or may not be relevant to you, but I’ll share it just to give you another perspective. I have a basic number of $36,000 per year, which is what I know our family could live off of to cover the essentials. And I also have a comfortable number of $60,000 per year which would give us plenty of cushion.

But the most important number is yours. And that’s something you can now figure out for yourself.

Life After Financial Independence

Reaching your financial independence number does not mean that you can’t still work and make more money. It does not mean you will stop growing financially for the rest of your life. It does not mean you are perfectly safe and secure forever.

Achieving the goal simply means that the pressure is off. Your assets could support you instead of your job.

This is an incredible place to be. An entire universe of life possibilities opens up.

The same job that you once hated could be transformed when you know that you’re there by choice.

Creativity and energy that had been dormant for years will suddenly reemerge.

New opportunities, new businesses, new questions, and new exciting paths will open themselves to you.

And even more amazing, these benefits don’t just emerge once you’ve crossed the finish line. Whether you’re at the peak or just a plateau along the way, the freedom of financial independence can still be experienced.

So, whatever an ideal life means for you, I highly recommend you figure out your own financial independence number. It will provide a clear, focused goal that will help you win with money.

What about you? Do you know your financial independence number? How did you arrive at that figure? How do you plan to get there? I’d love to read your comments below.