How to Use Seller Financing (aka Owner Financing) to Buy Real Estate

Seller financing (aka owner financing) is a way to buy real estate without having to go to the bank. As a real estate investor, it has been an incredible tool for me to acquire rental and flip properties. I've often received better interest rates, lower down payments, less risky terms, and most importantly - a long-term, win-win relationship with a real person (instead of a big corporate bank).

But many people don't know what seller financing really is or how it works. Other investors wonder "is owner financing a good idea?" And still others think owner financing is a good tool that rarely works in the real world.

That's why I created this comprehensive guide. My goal is that after it reading you understand seller financing and how it can benefit you as a buyer of real estate. Based on my 15-years of experience with seller financing as a buyer and seller, I'll show you what it is, how it works, the pros and cons of using it, and how to find, negotiate, and execute it.

How to Use This Guide (& Table of Contents)

This guide is almost 7,500 words long! To give you all the details you need to know, I had to cover a lot of ground. But don't feel like you need to read everything all at once.

Start with the parts that interest you the most, and then dig into the examples and details until they make more sense. And be sure to bookmark this as a resource to come back to over and over again.

The table of contents below will help you jump to the topic you want to read.

I’ll start by explaining how seller financing fits in with your overall toolbox of real estate financing strategies.

The Toolbox of Real Estate Financing

When a master carpenter builds a house, he uses different tools for different situations. To drive a nail, he uses a hammer. For cutting wood, he uses a saw. To turn a screw, he uses a screw driver.

And so it is with real estate financing. The different types of real estate financing are just tools in a toolbox. And the more tools you have and know how to use, the better real estate investor you will be.

Seller financing is one of the better tools available to you. But the other tools in your real estate financing toolbox include:

- Conventional financing – typically 15 or 30-year loans, often conforming to Fannie Mae/Freddie Mac standards

- FHA/VA/USDA loan programs – only for owner-occupied financing, like with a house hack

- Commercial financing – business loans usually from a local bank or other commercial lender

- Private financing – from an individual or an individuals’ self-directed IRA

- Hard money financing – also private financing but usually from a group or business that loans the money of others

- Lease options – has similarities to seller financing but the seller retains the property title (see my YouTube lease option video)

It would be ridiculous for a carpenter to try to use a hammer to cut a board or turn a screw. Yet, real estate investors try to use only 1 or 2 of the financing types above (usually conventional financing). This is basically like hitting every object (i.e. real estate transaction) with a hammer!

Only using “hammer” investing might allow you to drive a few nails and even force in a few screws. But you may miss out on many opportunities that could have been unlocked with more financing knowledge and skills. And eventually you may hit a wall of frustration and perhaps a bruised ego as your growth slows.

So, in the rest of the article I’ll help you expand your toolbox with one particularly powerful tool – seller financing. Let’s start with the basics of what seller financing is.

What is Seller Financing?

The definition of seller financing is a transaction where the seller extends credit to the buyer. You can think of it as a loan, although no money actually changes hand between the buyer and seller. Instead, the buyer usually makes a down payment and then the seller receives the rest of the purchase price in installments over time (aka an installment sale).

So at its most basic, seller financing just means the seller of real estate waits to get all of his or her sales price. Instead of getting the entire price in cash at closing, the seller carries back part or all of the price using some sort of contract (more on that in the section on Owner Financing Contracts).

There are actually different variations on the idea of seller financing. But for the purposes of everything I’ll explain in this article, here’s what I mean:

- A seller has equity in the property (i.e. no debt or a relatively small debt that can be paid off at closing)

- The seller deeds the property to the buyer

- The buyer gives the seller a promissory note (i.e. a debt or contract that outlines all the seller financing terms)

- The buyer also gives the seller a mortgage (or trust deed in some states) to secure the promissory note against the property.

While that’s what I mean, there are also various terms you might hear others use for something similar.

Other Related Terms For Seller Financing

The overall topic of seller financing can be confusing because there are numerous techniques and related terms that often get lumped together. They include:

- Owner financing

- Seller carry-back financing

- Installment sale

- Bond-for-title

- Contract-for-deed

- Wrap-around-mortgages

- All-inclusive-trust-deeds

- Lease options

- Rent-to-own

- Subject-to the mortgage

Owner financing, seller carry-back financing, and installment sale are different names for the same thing as the seller financing I’ll explain here.

But other names, like bond-for-title, contract-for-deed, lease options, subject-to, and wrap-around mortgages are similar but different techniques. I won’t be covering these in this article. It’s long enough as it is! But you can see links to a couple of videos I made in the section on seller financing with an existing mortgage.

In case all of that is confusing, let me explain exactly how this seller financing process works using some diagrams.

How Does Seller Financing Work?

A picture is worth 1,000 words, right? So, to explain how seller financing works I’ll give you my best artistic efforts.

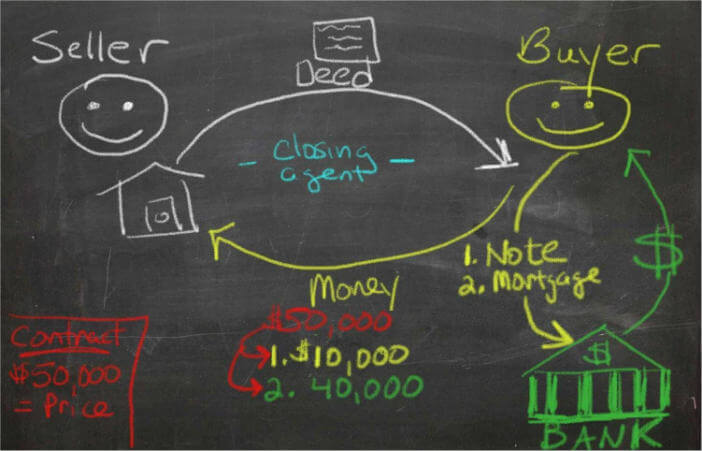

But I want to start by explaining a normal real estate transaction. Here is a diagram of how a closing would would typically work if you got bank financing.

(The only difference is that I’m not sure there would normally be so many smiling faces. It’s hard to smile when you actually read the 500+ page loan documents that basically pledge everything to the lender but your oldest child!)

A Picture of a Normal Real Estate Transaction

It’s important to know what’s exchanged in a closing. You just follow the money and the property. In this case:

- The bank brings the money

- The seller brings a property (in the form of a deed)

- The buyer brings a down payment AND a promise to pay back the money to the bank)

- The closing agent brings a promise that the property has good title (and a title insurance company backs up that promise)

So, these three parties plus the closing agent (an attorney or title company) are involved in the closing.

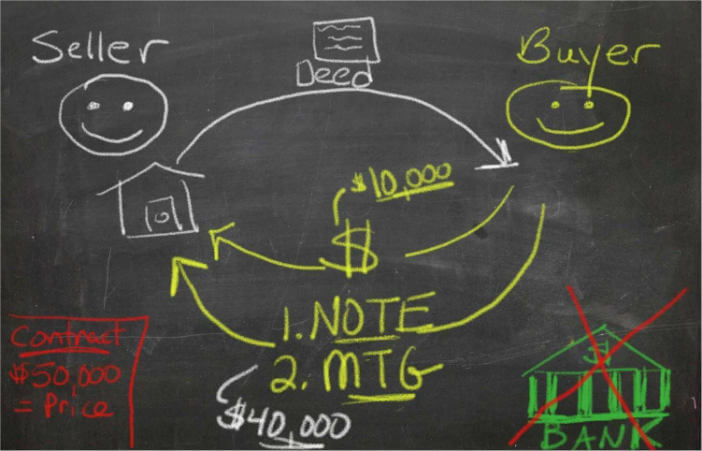

A seller financing transaction is similar, but there is a key difference: no bank or 3rd party lender.

A Picture of a Seller Financing Real Estate Transaction

Again following the money and the property, here is what’s exchanged:

- The seller brings a property (in the form of a deed)

- The buyer brings a down payment AND a promise (to pay the SELLER the entire purchase price)

- The closing agent brings a promise that the property has good title (and a title insurance company backs up that promise)

This time there are only two parties plus the closing agent. No “loan” is actually made because the seller doesn’t physically give the buyer money like the bank did.

Instead, the seller lets the buyer pay on credit over time. That’s what seller financing really is. And we’ll talk about the different seller financing terms that can be negotiated later in the article, like interest rate, payment amount, collateral, and more.

Now that you have an idea what seller or owner financing is, let’s look at the pros and cons of doing that type of transaction.

The Pros and Cons of Seller Financing

We’re all grown-ups here. You know that there are always pros and cons to every strategy. Seller financing is no different.

So, below I’ll explain the pros and cons of seller financing from two perspectives – the buyer and the seller.

Pros From a Buyer Perspective

Pros of seller financing from the point of view of the buyer:

- Easier qualifying – The seller still has to trust you, but typically less paperwork and hassles than a bank loan

- Everything is negotiable – Unlike with a bank or conventional lender who says take it or leave it

- Lower interest rate (potentially) – Especially compared with commercial or private financing

- Lower down payment (potentially) – I have negotiated between 0% to 10% down

- No personal guarantee (potentially) – With most loans, you pledge ALL of your personal assets in case the lender loses money. This can often be removed from seller financing contracts so that only the property is security for the debt.

- Faster, simpler closing – You avoid layers of bureaucracy, delays, repetitive processes, inspections, and appraisals

- Potential discount on the loan balance – Sometimes the seller or the heirs need cash. As a result, they may be willing to let you pay off all or part of the loan at a discount in exchange for a lump sum of cash. I have had this happen a few times.

- Valuable relationship for more business – A former coaching client of mine bought one property with seller financing. The seller later sold dozens of other properties to my client because they demonstrated their competence and trustworthiness. Similarly, you may also be able to get future private loans from the seller.

Cons From a Buyer Perspective

Here are the cons of seller financing from the point of view of the buyer:

- Everything is negotiable (!) – Although this is a pro, it’s also a con because you need to learn what terms to negotiate. There is a learning curve. I’ll give you some ideas later in the article, but I also recommend using a competent local attorney to help.

- Harder to negotiate – Seller financing requires patience and some skill to negotiate. I can teach you (see later in article), but you’ll have to throw out most traditional investor tactics and haggling that pit you against the seller.

- Issues with heirs – If the original seller dies, you will be involved with the estate and the heirs. You have a secured contract, so this doesn’t have to be a bad thing. But it may involve more hassle and communication than with a bank loan (although there are opportunities – like the potential discount I mentioned above!)

Now let’s take a look at the pros and cons of seller financing from the seller’s perspective.

Pros From a Seller Perspective

Pros of seller financing from the point of view of the seller:

- Familiar investment – The seller often owned this property for a long time. So, owning a mortgage secured by the same property is very familiar and can be more comforting than exotic or unfamiliar investments elsewhere.

- Continued income – If the property was a rental, the seller probably liked regular income. Seller financing continues that income stream just without the hassles of ownership and management.

- More Passive – Transitioning from landlord to lender is a natural progression. It’s less hassle and day-to-day worry, while still maintaining many benefits (like security of the real property and an income stream)

- Tax planning – The IRS recognizes an installment sale as a way to defer a capital gain on a property sale. This can save on taxes by avoiding a bump up into a higher tax bracket if the seller had a huge gain.

- Higher interest & return on investment – Compared with alternatives, like bank accounts, annuities, bonds, and stock dividends, interest on a seller financing note can often be much better. Plus, the seller earns interest on principal that would’ve been taxed if he or she had sold for cash.

- Higher Price – By offering terms, seller often get a higher sales price (with less holding costs) than if they sold for cash.

- Estate Planning – What would most heirs of an estate do with a lump sum of cash? Spend it! So, it can be smart to dole out inheritance in monthly installments so that the heir spends it more wisely – like on groceries!

Cons From a Seller Perspective

Cons of seller financing from the point of view of the seller:

- Everything is negotiable (!) – Like the buyer, this is a pro and con. Few sellers are familiar with seller financing or its terms, so the transaction requires careful thought and likely advice from family and advisers.

- Trust in the buyer – Banks qualify borrowers for a reason – it’s smart! So, a seller has to find a way to trust the competence and character of the buyer so that payments get made and the property doesn’t deteriorate.

- Inflation – Any fixed payment investment, including seller financing notes, become less valuable as inflation occurs. But at an older age or with sufficient other assets, this may not be an issue.

- Tax planning – The long-term landlord seller will likely have tax on depreciation recapture at the time of sale. So, a tax professional will likely need to help calculate the tax liability and sufficient funds must be available to pay the tax (typically from the seller’s down payment).

Now let me demonstrate these pros and cons by sharing the example of my first seller financing purchase.

Case Study: From Seller Financing to Life-Long Friends

In 2005 I bought a 3 bedroom single family house using seller financing. The sellers, named Ed and Eileen, were retired Methodist ministers and a wonderful couple.

I was 25 years old, and I was only a couple of years out of college. This was my first seller financing purchase, and it was one of my first rental property purchases period (I had previously only flipped and wholesaled properties).

Looking back now, I might have done a few things differently. But in the end I made money, the sellers were happy, and I became such good friends with Ed and Eileen that my wife and I asked them to be the ministers at our wedding (no kidding)!

Here’s how it all worked.

The Details of My First Owner Financing Purchase

All was was well with Ed and Eileen’s rental for a time, but then they ran into awful tenants. These final tenants tore up the house, left owing money, and spoiled Ed and Eileen on the idea of being a landlord. So, they were ready to sell.

They happened to receive a personal letter from me expressing my interest in buying their rental house. At that time I often sent letters to long-time property owners in locations I liked. They also talked to several real estate agents, one of whom said “you NEVER want to work with an investor like THAT.”

But Eileen looked me up on Google and didn’t seem to think I was THAT bad. And she later told me she had a good feeling about me after we met. I had shown up with a stack of reference letters, and I was not pushy or trying to talk her into something she didn’t want to do.

We actually met 2 or 3 times to get to know each other before I finally presented offers to purchase their property. I basically made two offers:

- $115,000 with $3,000 down and $112,000 in seller financing

- $100,000 with all cash at closing

Both prices were below the full $125,000 to 130,000 value of the house. But the seller financing price was about what they hoped to net after paying real estate agent fees. So, they accepted my offer.

The Final Results of My First Owner Financing Purchase

For my part, the seller financing offer worked because it allowed me to hold a solid property longer-term as a rental. I had a 10% discount, and the cash flow worked (barely!) after paying all costs and their principal and interest payments. With my cash offer I knew I’d have to borrow money from a private or commercial lender at a higher interest rates. So, I needed an even lower price in order to make the property cash flow.

So, we began renting the property. After the first tenant moved out, we found another who expressed interest in purchasing the house. So, about 4 years after we bought it, we decided to sell the property to our tenants for $130,000. It happened to be 2009 in the depths of the Great Recession. So we decided we needed the cash more than a long-term rental!

We had built some equity by paying the loan down, so we received a nice net gain of approximately $18,000 for our efforts. And Ed and Eileen got paid their own chunk of cash at closing. They used the money to pay off the remaining debt on their retirement residence.

Lessons Learned From My First Owner Financing Purchase

I went on to buy other properties with seller financing over the years. But they all shared a few key negotiating principles that I learned on this first deal:

- Approach the negotiation slowly, with the primary goal of helping the seller

- Focus on building trust FIRST before bringing up unfamiliar terms like “seller financing” (i.e. don’t ask a stranger over the phone if they will seller financing a property to you)

- Once the sellers are receptive, explain the pros and cons of seller financing using an offer

- Make multiple offers, at least one of which is seller financing. You never know which offer they will want.

- Use seller financing as a tool to buy a property that fits into your overall investing strategy and that makes sense when you run the numbers. Some people get caught up with the tool and forget the overall real estate fundamentals (I speak from experience!)

With those lessons in mind, let’s go into more detail on how to find properties and sellers who may be willing to owner financing to you.

The Type of Owners Who Will Finance Their Properties

The universe of people who may sell you a property is enormous. But the type of seller willing to carry back the financing is much smaller. So, you have to first understand who those people are before you start looking for owner financing properties.

One time I reviewed all of my purchases where the sellers financed their property to me. The results confirmed what I already suspected — well over 50% of sellers were what I called “burned-out landlords.” You may also run into other types of sellers willing to owner finance. But if you want to give yourself the best chance of buying properties with owner financing, I recommend that you focus on burned-out landlords first.

A burned-out landlord is basically a rental property owner who has become fed up with tenants and all the other details of rental ownership. And if you don’t study rental best practices or treat it like a business, it’s EASY to become burned out. You’ll quickly hate the business if you fail to learn how to screen tenants, allow tenants to break rules (or don’t have rules!), don’t maintain the property, and do too much work yourself.

Real-Life Situations That Lead to Burned-Out Landlords

The sellers who financed to me included situations like:

- Savvy investor who lived too far away to self-manage like he did his other properties

- Real estate agent whose brother rented the building but was not a good tenant (sometimes it’s easier to sell than kick out family!)

- Sister and brother who inherited their childhood home, tried renting, but got fed up with bad tenants

- Man who inherited a house from his mother, tried renting, but got emotionally upset seeing tenants in his house

- Investor who couldn’t handle the intensive management of a house in a low-rent neighborhood

- Investor ready to retire and travel but wanted continued passive income

The common theme was that all of these burned-out landlords were motivated. This doesn’t mean they were desperate or unaware of what was going on. In most cases they had more business and investing experience than me! But they had enough motivation so that I could negotiate terms they may not have initially thought they wanted.

And remember the pros and cons I explained earlier? Because these sellers were motivated, they were more receptive to listening to the benefits of seller financing (especially after they got to know, trust, and like me). And many of those benefits fit the situations of long-time landlords in particular.

So if burned out landlords are your #1 type of owner who may finance a purchase, how do you find them? Here are a few ideas.

How to Find Burned-Out Landlords

There are many ways to find investment properties to purchase. But here are some ideas how to specifically find burned-out landlords who may be more likely to owner finance a property to you:

- Absentee landlords – Absentee owners are property owners who don’t live in the property. By sending letters to absentee owner, some of them may fit the burned-out landlord profile. You can buy a list from online sources like realquest.com, CRSdata.com, or listsource.com, or you can sometimes get lists from your MLS or local county tax assessor.

- Eviction landlords – Eviction court cases are public records in most locations. You can contact owners by mail or phone and ask if they’d like to sell. This is often the peak time of motivation after being frustrated with tenants!

- Vacant houses – When you drive or walk around your target neighborhoods (aka Driving For Dollars!), you’ll see vacant houses. Track down the owner and ask them if they want to sell. Some owners will be landlords, and a vacant house costs them money and creates stress. So, you will be offering a solution to their problem.

- Networking – Participate at local real estate meetups, Real Estate Investor Associations, and online forums. You will sometimes meet rental investors who are motivated to sell a particular property. Also tell everyone you know that you buy properties from people tired of owning a rental property.

- For Rent – Find For Rent signs and ads (like on Craigslist) and contact the phone number. After gathering initial information, ask if they’d be interested in selling. They just might be a burned-out landlord.

Once you find a willing property owner and begin negotiating, you’ll need to discuss the terms of owner financing and put them into a contract. So, I’ll explain the important terms in the next section.

Typical Owner Financing Terms

Contracts are central to successful real estate investing. That is why you should always have a competent real estate attorney on your local investing team. This specialist can help you apply the general concepts and turn them into contracts that work within your local laws.

But as a negotiator of owner financing, you also need to understand the typical owner financing terms. It also helps to be able to write them down yourself when you’re sitting in front of a seller willing to accept your offer.

So, in the list below I’ll give you some of the most important terms you’ll want to discuss during a negotiation. Most of these would be put in an addendum to a standard real estate purchase contract, which I’ll discuss more in the section on owner financing contracts.

Price

This seems like an obvious one, but just know that there is always a relationship between price and terms. I don’t advocate paying more than a property is worth. But there is no doubt you can sometimes pay a premium price depending on the other terms, like a low payment that allows you to cash flow an otherwise great property.

Your plans for the property can also determine how high or low of a price you can pay. It all starts with creating your own real estate deal analysis goals. But for example, buying an in-demand, long-term hold property in a quality location can make sense to pay a retail price. This is especially true if the seller financing terms allow you to have good rental cash flow.

But if you’re buying a house in a depressed location or planning to resell the property sooner, you should push for a price as low as possible – even with good terms.

Down Payment

Most sellers will want some sort of down payment so that you have “skin in the game.” But a seller may be happy with a much smaller down payment than a traditional lender would. So, don’t be afraid to ask for 3%, 5%, or 10% of the purchase price as a down payment.

You can also think creatively about what you give as a down payment. Let’s say you’re buying an expensive 30-unit apartment building. What if you own a piece of land, a truck, or a promissory note paying monthly interest? Each of those assets has a value. And the seller might perceive their value higher than you do.

For example, I once traded a Harley-Davidson motor cycle that I owned as a down payment. The seller had buddies who all rode motorcycles together, and his motivation completely changed after I brought up the idea! He ended up seller financing the balance of the purchase price to me.

Also, if the property needs a lot of repair work, don’t be afraid to negotiate your repairs as part of your skin in the game. I once negotiated a $5,000 down payment (much less than the seller wanted) because I also agreed in my contract to a long list of repairs. I already planned to do them, but it put the seller at ease knowing I was spending an additional $30,000 or more improving the security for his seller financing.

Interest Rate Amount

This is another term that seems straight forward. But keep in mind that with long-term financing, you pay more interest than you do the original purchase price! So, it pays to negotiate as low an interest rate as possible.

For example, consider a $250,000 purchase price with $50,000 down and $200,000 as seller financing at 7% for 30 years. The total interest paid over 30 years is just over $279,000! But with a 4% interest rate, the total interest paid is just under $144,000. That’s a $135,000 difference!

You may even be able to negotiate an interest rate of 0%. But keep in mind that the seller will have to report imputed interest on their tax return. This is a tool the IRS uses to collect interest on loans with low or no stated interest. Rates below IRS issued applicable federal rates (AFR) must report imputed interest. For example, the long-term AFR in March 2018 was 2.88%.

Stepped-Up and Accruing Interest

If you’re in a stalemate on an interest rate negotiation, you could propose stepped-up interest rates. So, for example you may start with an extremely low interest rate in years 1 and 2 while you improve the property and raise rents. Then in year 3 the rate could increase to something higher once you’ve improved the cash flow (or sold the property).

You’ll also need to negotiate whether your interest rate is fixed or adjustable. As a buyer or borrower, you always want to fix your rate for as long as possible and as low as possible. But the seller may not agree.

So, if you have to add in an adjustable rate, just make sure to push it into the future as much as possible. A seller may be happy knowing that after 10 years the rate can adjust so that he or she isn’t stuck with a very low interest rate when overall rates have risen significantly. And you may be able to protect yourself with a ceiling so that the adjustable rate doesn’t go above a certain amount or go up too fast.

Delayed Interest Accrual

Interest is normally paid in arrears. This means interest starts accruing one date and then you make a payment later (usually on the first of the next month). But few people realize you can negotiate when the interest begins accruing.

For example, what if you’re buying a vacant property that will take 3 months to repair and get rented. The seller who is not currently receiving any income may be open to waiting 3 months to begin accruing interest. This means your first payment would be 4 months after closing! If your interest was $1,000/month, for example, this would be $4,000 in savings.

Payment Amount and Start Date

Most financing payments are amortized, meaning each payment includes both principal and interest. And usually the length of amortization is something like 15, 20, or 30 years. This means all the principal will be paid in those periods of time by just making the minimum payment.

You’ll want to make sure whatever payment you negotiate makes sense with your exit strategy. If you’re renting, you want it to meet your cash flow goals. And a lot of that will be determined by the interest rate you negotiate.

But, you can also negotiate a lower, interest only payment or even a negative amortization (not enough to cover all the interest). I personally don’t think either of these are a good ideas long run. Principal pay down is a form of discipline that prevents you from staying leveraged forever. But over a short-period, like where you’re trying to increase rents on a property, this can be a good tool.

And like the interest accrual negotiation, payments don’t have to start 30-days after closing. If you negotiate interest not accruing for 3 months, your first payment could start in month #4.

Maturity Date

The maturity date is a term that states when you must have all the principal of the financing paid back to the seller. Typically this is the same date when your amortization runs out, like at the end of 30 years. But you could also have a balloon payment, which means you must pay a lump sum payment of whatever is owed on a certain date.

I don’t like balloons payments. They sound so friendly, like birthday party decorations! But having to come up with a large amount of money at one time presents one of the biggest risks we face as real estate investors. Just look at how real estate investors, builders, and banks went out of business in the Great Recession of 2008 – 2010. Their balloons popped, and no one would give them the money they needed!

But if everything else in the deal makes sense and I have to negotiate a balloon payment, I want it as far in the future as possible. You want to give yourself time to make it through 7 to 10 year real estate cycles before having to refinance or sell.

I also prefer to negotiate a call date instead of a balloon date. This means the seller CAN call the loan due, but they don’t have to. This means you can continue making payments if the seller is happy instead of having to renegotiate the entire deal. I learned this specific distinction and many of the others from a very smart investor named Dyches Boddiford at assets101.com.

First Right of Refusal

Did you know that promissory notes, including seller financing notes, are assets that can be sold to third parties? There is a thriving business of note buyers who will likely contact your seller very soon after he or she sells the property to you with financing.

But the people who buy notes from your seller will almost always want a significant discount from the face value of the note. This means a on a $100,000 note your seller may receive $70,000 or less when it’s sold.

Wouldn’t you want the opportunity to buy the note at that same discount? I know I would! And I actually have several times in the past.

But I got that opportunity because I had a clause called a first right of refusal. This means the seller has to give me the first opportunity to buy the note if he or she decides to sell it.

I first learned this idea and many others in this article from a long-time investor and teacher, Greg Pinneo at corcompany.com.

Security For Financing (i.e. Description of Property Collateral)

A financing debt comes in two primary forms – secured and unsecured. Credit cards are unsecured because there is no collateral. But most real estate financing is secured because you give the lender a mortgage (or deed of trust) as security. If you stop making payments or breach another term of your contract, the lender can foreclose and take back the property.

This one again seems straight forward, but here are a few ideas to think about:

- First position or subordinate position – First position means a mortgage is recorded first on the public records. For this reason it must be paid off first if there is a foreclosure. Most financing will be first position, but there may be situations where the seller financing is in second position. For example, you could get a 75% loan from a bank or private lender (first position), a 20% seller carry-back financing (second position), and 5% down.

- A different property – You could give the seller a first position mortgage on a different property than you’re buying. This might be advantageous if you want to keep that other property as a long-term rental, and then you could sell the seller’s property in order to recoup your cash. I’ll explain this even more in the next section on substitution of security. But I’m mentioning it now because you could negotiate a different property as collateral from the start instead of using the subject property.

- Multiple properties – There might be a time where a seller wants additional security in order to finance to you. You may give the seller a first or second mortgage on other properties.

Substitution of Security

Also called “walking the mortgage,” substitution of security is an excellent term to negotiate as the buyer. This means that when you sell the original property, you can:

- Keep the promissory note in place (i.e. continue making payments on the debt)

- Satisfy the mortgage on the original property

- Give the seller a NEW mortgage on a different property as collateral

I did this one time when I bought two properties that were not ideal long-term holds. The houses were too big and expensive for rentals. So, I told the sellers that, and I also told them I’d like to give them different properties as collateral for their seller financing once I sold their houses. Obviously this wasn’t something they had heard about, and it took some explaining (I like to use drawings).

But because I had built a lot of trust and because I was solving their problem of getting their houses sold quickly, they said yes. I also put in the contract that their new, substitute security MUST be in a first position, MUST be below 70% loan to value, and MUST have sufficient net rental income to cover all of their mortgage payment. And obviously they could ask me to confirm all of that with a third party, if requested.

The Results of the Substitution of Security

So at closing, I gave them a 50% down payment and then 50% as seller financing mortgages. The interest rate on this financing was around 3%. Then I fixed up and sold both houses.

But instead of paying off the seller financing debt at closing, the closing attorney paid off mortgages on other properties that I owned (which were 7% interest). That meant those properties were now free and clear of debt, and the closing attorney just created new mortgages for my sellers and recorded them against those substitute properties.

In the end, the sellers had very secure first position mortgages on multiple properties. They also had a steady income stream to support their retirement. I essentially refinanced my long-term rentals by flipping the seller’s houses and moving their financing to my rentals.

It was a win-win transaction that all resulted because of the substitution of security clause.

Due on Sale Clause

The due on sale clause is a standard clause in conventional (i.e. bank) mortgages that gives the lender the right to call the loan due and make you pay it off if you sell the property. But you don’t have to include it in your seller financing. And I always prefer not to.

Why do I want to leave it out? Because I want the opportunity to sell the property on a wrap around mortgage (aka all-inclusive trust deed in some states) if the opportunity arises. This means I could resell the property and finance it to my buyer with payments and terms wrapping around the sellers.

I’ll show what I mean with an example.

I once bought a house with seller financing. It began as a rental house, but a couple of years later the tenant expressed interest in buying the house. They had saved 10% down, and they proved they could make on-time payments during the prior two years. So, we agreed to finance the house to them.

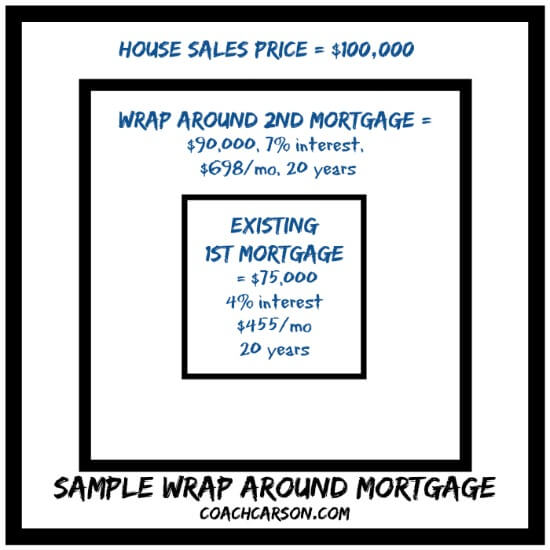

Example of a Wrap Around Mortgage

Here are the simplified numbers for my original purchase:

- $80,000 = my purchase price

- $5,000 = my down payment

- $75,000 = seller financing

- $455/month = payment at 4% interest for 20 years

Here are the simplified numbers for my resale and creation of a wrap around mortgage:

- $100,000 = tenant’s purchase price

- $10,000 = down payment

- $90,000 = seller financing (2nd position, wrap around mortgage)

- $698/month = payment at 7% interest for 20 years

My seller financing mortgage with the original owner is in first position. The buyer’s mortgage with me is in 2nd position. But I (or a third party servicing company if that makes the buyer more comfortable) collect 100% of the buyers’ payment, and use part of it to pay the seller financing mortgage.

The entire wrap around mortgage arrangement looks like this:

Results and a Caution For Wrap Around Mortgages

So in this example, I earned $5,000 from the down payment ($10,000 – $5,000 = $5,000). Each month I received $243 in positive cash flow ($698 – $455 = $243/month). And my starting equity position in the property was $15,000 ($90,000 – $75,000 = $15,000.)

Being in the middle of a wrap around mortgage can be a very profitable transaction!

But a word of caution. There is risk to this arrangement for me in the middle, because my buyer could stop paying me and I would have to continue paying my seller. And this actually happened to me during the Great Recession years. So, I highly recommend setting aside large cash reserves as a contingency.

The bottom line, however, is that a wrap around mortgage is a profitable strategy to “borrow” at a low interest rate and “lend” at a higher interest rate (aka arbitrage). And it only works because you didn’t have a due on sale clause in your original seller financing mortgage.

Owner Financing Contracts

One of the challenges with seller financing is that unlike bank financing, you (or more likely your attorney) will need to create your contracts. But this is also an opportunity, because the terms in traditional lender notes and mortgages are rarely advantageous to you as the buyer.

Here are the primary contracts you’ll need to have in place in order to execute a seller financing transaction:

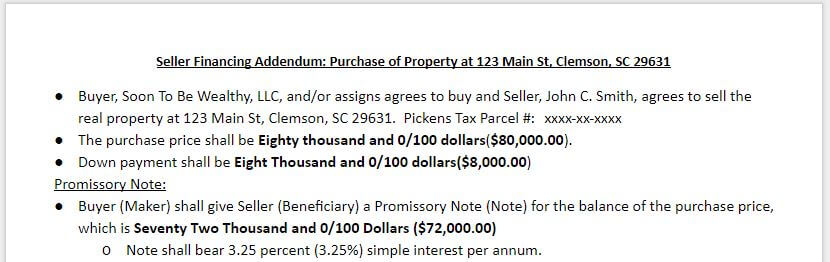

Seller Financing Addendum:

Much of a seller financing purchase will be standard. So, you can use a standard purchase and sale agreement in your state when you put a property under contract. But you’ll want to include an addendum that clearly explains all the terms of your seller financing agreement with the seller.

Early on you can have your attorney prepare one for you. But because every deal is such a custom transaction, I normally have a blank addendum with “Seller Financing Addendum” at the top. And then I hand write all of the terms the seller and I agreed to write there on the spot. Here’s an example:

The details of this addendum will just be the exact terms I covered in this article. Some the seller will agree to, and others the seller will not. So, I’ll either include or leave out the terms based on our negotiation.

Promissory Note and Mortgage (or Deed of Trust)

The promissory note is the contract that outlines all of the terms you’ve negotiated in the seller financing addendum above. When you hear the term “debt,” it’s referring to this contract. It basically states what you owe to the lender (or seller in this case) and how you plan to pay it back.

The mortgage (or deed of trust in some states) is the contract that connects your promissory note to the property that is pledged as collateral (aka security) for the debt. Although there are many terms included in a mortgage, it essentially gives the seller the right to foreclose and take back the property if you don’t keep your promises.

I recommend having your local attorney prepare the promissory note and mortgage for you. But be sure to not let them just use a boiler plate type they use for everyone else. Sit down with them and explain what you’re trying to accomplish as an investor. You can use this article as a guide for the terms you want to include, and the attorney may also want to include others that protect you and apply to local laws.

Challenges and Realities of Seller Financing

Before I close this guide, I want to point out some challenges to and realities of seller financing. As I hope you’ve seen, it can be a fantastic strategy for both the buyer and seller of real estate. But there are some things you’ll want to be aware of before jumping in. Here are a few of the major ones:

Seller Financing With an Existing Mortgage

The type of seller financing in this guide has assumed that a seller does not have a mortgage or has a small mortgage that can be paid off at closing. This allows the seller to give you a deed and then receive a promissory note and first position mortgage.

This has always been my preferred method to buy with seller financing. It’s cleaner and more straightforward for both parties. But there are also strategies where a seller has an existing mortgage and may be willing to seller finance.

The biggest problem with this is something called the due on sale clause, which I discussed earlier in the section on terms. Most traditional or bank mortgages include this clause, and it gives the lender the right to call the loan due if you sell the property without paying off the mortgage.

Risks and Seller Financing Variations With an Existing Mortgage

So, if someone finances a property to you and their underlying mortgage has a due on sale clause, you are taking a risk. The bank could call the loan due at any time, and you would have to pay it off or lose control of any equity in the property.

With that said, sometimes underlying mortgages don’t have due on sale clauses (like the seller financing in my wrap around mortgage example above). And in other cases, you may be willing to buy the property anyway and take the risk of the due on sale clause. It’s possible the lender will allow you to continue making payments instead of pursuing their option to call the loan due (at least for now).

In either of those cases, there are some variations of the primary seller financing strategy that you could use. As this is already a LONG article, I can’t cover them in detail. But I just wanted you to know they exist. Also know that each has it’s advantages and sometimes serious disadvantages. So, be sure to study the strategies carefully before using them.

The seller financing variations include:

- Contract For Deed (aka Bond-For-Title, Land Contract, Agreement For Deed)

- Lease With an Option to Buy (see my YouTube video for more details)

- Buying Subject-To the Mortgage (see my YouTube video for more details)

- Wrap Around Mortgages (aka All-Inclusive Trust Deeds) – which I covered briefly with an example in a prior section

I plan to cover some of these in future articles to show how they can be used.

Dodd-Frank Act and the Effect on Seller Financing

In 2010 the US Congress passed a sweeping law known as the Dodd-Frank Act. It was an attempt to control the lending industry to avoid another meltdown that caused the 2008 to 2010 recession. But in addition to bank regulations, seller financing was also included in the law.

But for the purposes of this guide, an important exception was included in the law. Seller financing to an investor (i.e. does not intend to reside in the property) is exempted from Dodd-Frank regulations. So, everything I explained in this guide where you, as an investor, negotiate to buy with seller financing will be exempt.

But in other cases where the seller financing is to an owner occupant, then the law may apply. See this article for an excellent summary of the law’s impact and rules as they apply to seller financing.

The Owner Financing Learning Curve

Perhaps the biggest challenge of the seller financing I explained in this guide is a learning curve. To successfully find, negotiate, sign a contract, and close on a deal with seller financing is different than the regular old closing with traditional financing.

I happen to think it’s worth the effort! But you’ll need to study this strategy, get help from local team members (especially your attorney), and practice.

I was very rusty when I bought my first seller financing property. But as you saw in the earlier example, I was able to overcome my rookie mistakes by just talking to sellers and taking action.

Conclusion

You’ve made it to the end of the Ultimate Seller Financing Guide! I hope you’re learned how seller financing works and why it can be a good idea for you and property sellers.

Seller financing has been one of my favorite tools to buy properties. It made closings much easier because I didn’t have to go the bank to get a loan. And the terms of my seller financing created financial benefits for both me and the sellers.

Plus, I found that my favorite part of buying properties with seller financing was the people. I built lasting, mutually beneficial relationships with real people. And that’s something that’s missing too often in the modern mortgage and real estate processes.

So, I hope you’ll make seller financing a part of your real estate investing strategy. Just apply the lessons from this guide and go make it happen!

Have you ever bought a property with seller financing? What was the process like for you? And if you have questions or comments about anything in the guide, I’d love to hear from you in the comments below.

to Buy Real Estate - Pinterest - 735x1332")