How to Run the Numbers For Rental Properties – Back-of-the-Envelope Analysis

Rental properties in the right location and with the right numbers are incredible vehicles to take you to financial independence. But without getting both of those factors right, rental properties may not work well.

So, in a prior article, I shared how to find the right location. In this article, I’m going to show how to find the right numbers. But instead of using in-depth rental property spreadsheets, the math I’ll share can be done on a scrap piece of paper. This form of quickly running the numbers is also called back-of-the-envelope (BOE) analysis.

Why Back-Of-The-Envelope (BOE) Analysis?

You may ask yourself why anyone would run the numbers on the back of an envelope for a major investment like real estate! Isn’t that crazy and risky?

But in reality, this is what most savvy, experienced investors do. Instead of wasting time early on, BOE analysis tells you if a potential deal has promise or not. If the BOE math looks good, you can then make an offer and get the property under contract subject to further inspections and verifications.

Even Warren Buffett, an investor who buys businesses for BILLIONS of dollars at a time, said this about running the numbers on investments during his 2009 annual meeting of shareholders:

If you need to use a computer or a calculator to make the calculation, you shouldn’t buy it”

Good deals should jump off your paper and smack you into action, even with back-of-the-envelope numbers. If you have to overanalyze the deal for hours using spreadsheets in order to make the numbers work, it’s probably not good enough.

With that advice from the Oracle of Omaha in mind, let’s take a look at how to run the numbers for rental properties. Here is an outline of what I’ll cover in the rest of this article (click on a link to jump directly to that section):

- Why good deals are like retirement engines

- The BOE Financial Snapshot

- My two key real estate BOE calculations – income & equity

- Putting it All Together – The Entire BOE Process

- How Faster Decisions Lead to Better Deals

Now, let’s get started!

(Watch me explain these concepts in a YouTube Tutorial)

Good Real Estate Deals Are Like Retirement Engines

Before we get into the nitty-gritty of numbers, let’s take a step back and look at the big picture. The #1 job of your rental property investments is to help you retire earlier and with more confidence.

I look at each property as a train engine. Each individual engine combines with the others to pull your overall finances down the tracks towards your goals. The better the property’s numbers, the more pulling power it has.

There are a couple of important financial goals these engine-like rental properties can help you accomplish.

First, rental properties help you build wealth. Over time, they can turn a small amount of your savings into a much bigger amount. Each of the real estate retirement plans I’ve outlined in other articles accomplishes this wealth-building goal.

Second, rental properties provide cash flow that allows you to live. This cash flow replaces your need to work at a job and trade hours for dollars. It’s the ultimate financial harvest, and it’s likely the reason you invested in the first place.

But how good is a particular rental property retirement engine? A quick back-of-the-envelope “snapshot” of the property’s financials will tell you.

The Financial Snapshot – Income and Equity

In my own back-of-the-envelope rental analysis, I create what’s known as a “snapshot.” A snapshot is like a quick photograph of your deal’s finances (I got the term snapshot from the book The Real Estate Game). You typically create the snapshot early in your deal analysis on a legal pad, envelope, napkin, or whatever scrap of paper you can find.

The snapshot allows you to quickly look at the financial highlights and determine if the deal meets your investment goals. This efficiency is especially handy early in your investing career because you will need to look at many deals (perhaps hundreds) before finding one that works.

My version of a rental property snapshot and the rest of this article focus on two important numbers:

- Income

- Equity

These numbers are related, but they each uniquely contribute to your wealth building and to your ability to generate cash flow that replaces your need to work.

I’ll explain my favorite tools for each of these calculations in the sections that follow. At the end, I’ll pull it all together and show you a step-by-step process to do a BOE analysis.

Income – Rental Property Calculation #1

There are a lot of different ways to define income. But I’m going to keep it simple:

Income is the money you earn after collecting rent and paying all of your expenses

In a basic investment scenario, you rent a property. Your tenants get to use the property, and in exchange, they pay you rent. After all of your expenses are paid, you get what’s left over.

This number is important because renting is the core business of investment properties. It’s the steady engine that pays your mortgage and pays your bills over time. Unlike your equity, which is based upon the relatively fuzzy estimate of the property’s resale value, rental income is less difficult to collect and less speculative.

So, how do you calculate income using back-of-the-envelope math? The following sections will explain my favorite tools to do that.

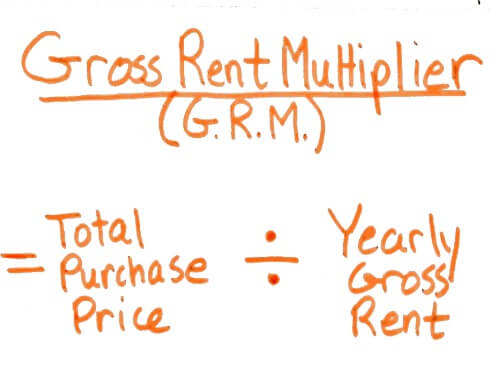

Gross Rent Multiplier (GRM)

Gross rent doesn’t mean gross as in disgusting. For those of us who collect rent regularly, it’s actually quite delicious:)

Gross rent means the total rent, before subtracting expenses or other deductions. And it’s useful because the gross rent is simple to find and easy to compare to other rental properties.

With my back-of-the-envelope snapshot, I begin by using the gross rent to calculate the Gross Rent Multiplier (GRM). The GRM is similar to the Price/Earnings (PE) ratio in stock investing. It’s just a ratio of the property’s total purchase price (including any upfront repair costs) to its yearly gross rent.

Why is the GRM useful? Because it roughly tells us how good a property is at producing income.

For example, a property with a GRM of 12 ($144,000 price / $12,000 rent) is much better at producing income (at least on paper) than a property with a GRM of 20 ($300,000 price / $15,000 rent). The higher the GRM, the less attractive an investment property becomes.

GRM isn’t the only quick analysis I use with gross rental income. A very similar rule of thumb is something called the 1% rule.

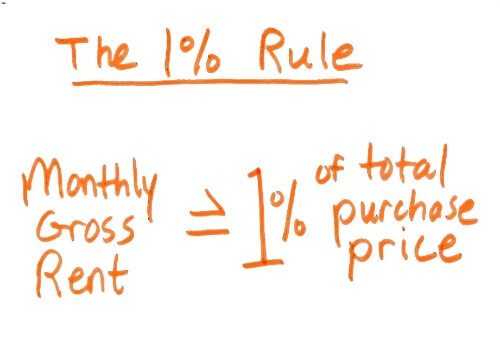

The 1% Rule

The GRM is a ratio using yearly rent. But real estate investors usually think in terms of monthly rent. So, the 1% rule is a rule of thumb that takes that into account.

I explained the 1% rule in more detail in another article. But in brief, the 1% rule says that the gross rent of a property should equal at least 1% of the purchase costs (or better).

For example, a property with a total upfront cost (price + closing/holding costs + repairs) of $200,000 should at least have a monthly gross rent of $2,000 to meet the 1% rule.

This property that meets the 1% rule would have a Gross Rent Multiplier of 8.33 ($200,000 / $24,000). $24,000 is the annual gross rent, or $2,000 x 12 months.

Meeting the 1% rule does NOT automatically make a deal good. I have even seen properties meeting the 2% rule that I’ve walked away from because of a bad location and rent collection challenges. And properties in high-priced locations will never come close to the 1% rule, yet they still could make financial sense in some cases.

This is a rule of thumb that just allows for quick and easy analysis. If a property DOES meet the 1% rule, it is just one sign that you may have an interesting investment candidate in front of you.

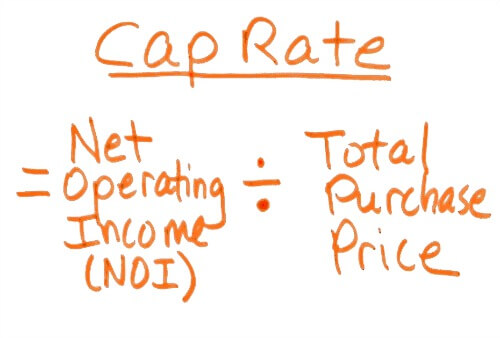

Cap Rate

A cap rate is another important income calculation. Unlike the gross rent multiplier, a cap rate tells us how well a property produces income AFTER expenses. In another article, I explained in-depth what a cap rate is and why it’s important. But for now, here’s a basic definition:

In case you’re wondering, the Net Operating Income (NOI) is your gross rent MINUS all of the property’s operating expenses and deductions like vacancy, management, taxes, insurance, repairs, HOA costs, etc. These expenses do NOT include financing costs.

**If you’re a visual learner, also check out the YouTube videos I made for more detailed explanations of Cap Rate and of Net Operating Income.

For an example of cap rate, let’s say a property produces $6,000 per year in NOI and its total upfront purchase costs are $100,000. $6,000 / $100,000 = a 6% cap rate.

Compare this to another property that produces $7,500 per year in NOI and its total upfront purchase costs are $300,000. $7,500 / $300,000 = a 2.5% cap rate.

One deal produces a 6% unleveraged return (i.e. if there was no debt). The other produces only 2.5%. If all other factors are equal, which deal would move you towards your financial goals faster? The cap rate makes this obvious.

I also use the cap rate as a minimum investment goal. I will typically set a minimum cap rate that I’ll accept for an investment in a certain location. If the cap rate is below that number, I won’t buy it unless I can do something to the property to quickly increase it.

Also, keep in mind that appraisers or brokers of investment properties use cap rates to discuss the overall market. They might say, for example, “the market cap rate is 7%.” This means on average most investors in the market purchase their properties with a 7% cap rate.

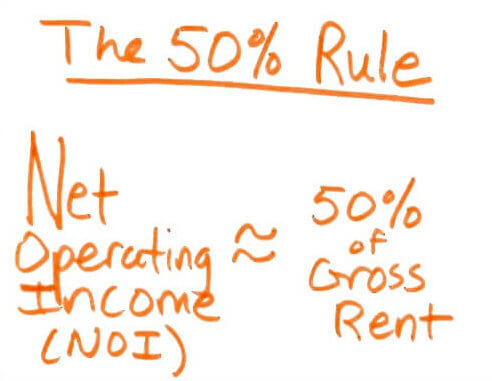

The 50% Rule

The 50% rule is a shortcut that helps you quickly estimate the NOI and the Cap Rate. But it’s important to remember that it’s just a shortcut and not the final analysis.

This rule of thumb assumes that 50% of your gross rent will be lost to your operating expenses. So, that means your estimated NOI is 50% of the gross rent.

This helps you quickly run the cap rate calculation with your back-of-the-envelope snapshot.

For example, if the yearly gross rent is $18,000, 50% of that is $9,000. If your estimated total purchase investment is $180,000, then your cap rate would be $9,000 / $180,000 = 5%.

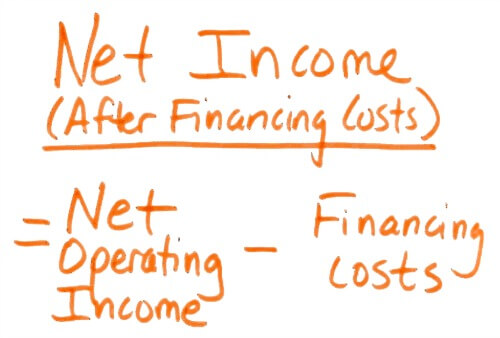

Net Income After Financing Costs

Until now all of our BOE income analysis did not take financing into consideration. But many real estate deals DO include financing. So, you will want to know how much rental income is left over AFTER you deduct our financing costs.

I’ll assume you can figure out how to estimate your monthly mortgage payment. If you need a refresher, I like this free amortization calculator and you can learn how I use it in my article How to Calculate Rental Cash Flow.

Here is the basic formula for pre-tax net income after financing:

You can set goals for a minimum amount of cash flow you’d like to earn per property. For example, your goal may be to earn a net income of $100/unit. So, a 4-unit property would have to produce a minimum of $400 per month.

This type of goal is useful so that you can ensure your property produces enough regular income to reinvest into one of your real estate retirement plans or to pay for your lifestyle once you’re ready to take it easy.

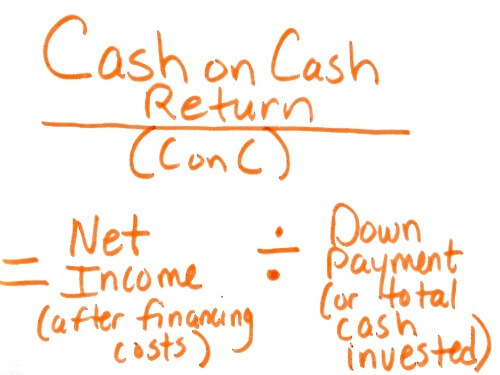

Cash-on-Cash Return

After calculating net income, I like to also run a final income calculation called the Cash-on-Cash (ConC) return. The ConC return tells you how much of your down payment or upfront cash investment comes back to you as cash per year. Here is the formula:

If you have a very small down payment (i.e. large amount of leverage), the ConC return is actually not that useful. For example, if you invested $5,000 and earned $400/month, you’d have a 96% ConC return! Or if you invested none of your own money (I’ve done this), the return is infinite – even with a minuscule positive cash flow.

While you could use these high ConC returns to brag to your friends, extreme leverage is really what makes this possible. And while I benefited early on from this kind of leverage, just remember that leverage-magnified returns can also lead to leverage-magnified losses! Eventually, you should have more cash to invest in deals if you’re successful.

The ConC becomes more useful when you invest these larger amounts of cash up front. It’s a form of discipline to help you compare your cash return from this deal to other potential investments like bank CDs, bonds, stock dividends, and annuities. Because cash flow is so critical to surviving long-run as a real estate investor, I like my rental investments to make a premium ConC return compared to these other lower-hassle forms of investing. So, if risk-free government bonds return 2%, I want to certainly make a lot more than that.

Like all of these calculations, you have to also look at the entire picture. If you’re making huge returns on the property’s equity, for example, it might be acceptable to have a smaller or even a negative ConC return for a short period of time. But in an ideal world, you’d make acceptable returns with all calculations.

Now that we’ve covered the BOE analysis for calculation #1 – income, let’s continue and look at calculation #2 – equity.

Equity – Rental Property Calculation #2

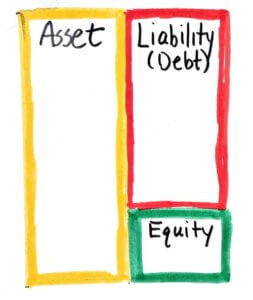

Equity is a financial term for what you own. Maybe you’ve heard equity used to describe shares of a stock in a company, but equity can also be calculated for a real estate property. What you “own” is the difference between the fair market value of the property (your asset) and the balance of any debt (your liability).

Here is my drawing of a balance sheet to show the basic relationship between assets, liabilities, and equity:

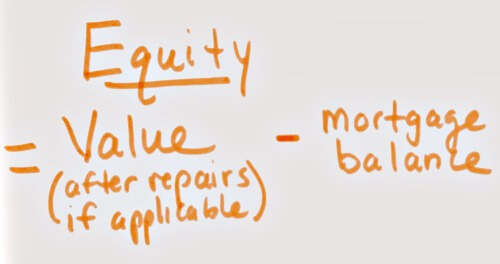

Calculating equity is simple. The math is like this:

There are two numbers you must know for this simple math, the value and the mortgage balance.

I explained how to do a quick property value analysis using comparable properties in The Ultimate Guide to Quickly Estimating a Property’s ARV at BiggerPockets.com.

This DYI valuation process is not a replacement for expert help from an appraiser or experienced real estate agent. But this article is really about how to be the captain of your own real estate ship. So, you should use 3rd party experts as additional resources, not as your only source of information.

The ARV process explained in that article also assumes you’re buying a house or small multiunit that is best valued with comparable sales. If you’re buying a larger income property that obtains its value from the income approach to value, you’ll want to use that process (and certainly get a second opinion). Here’s a good example of the income approach to valuation in action.

The mortgage balance calculation is more straightforward. For the present balance, you’ll just use the amount you’re borrowing. For a future mortgage balance, you can just use an amortization schedule.

To help apply this equity calculation, I’ll share some real-life scenarios.

5 Examples of Equity Calculations

Equity is a simple concept. But it’s also one of the most powerful ways to build wealth in real estate investing. These 5 examples will show you how it works.

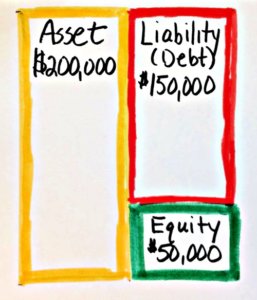

Example #1 – Full Price Purchase

In this example, you pay $200,000 for a property, put $50,000 down, and borrow $150,000. Because you paid the full price for the property, your equity is the same as your down payment $50,000.

Example #2 – 10% Discount

In this example, you work directly with the seller (no listing agent), close quickly, and pay cash. This allows you to negotiate a 10% discount from the full value of $200,000. So, you pay $180,000 for the property, you still put $50,000 down, but you now borrow $130,000.

Now your equity looks like this:

You spend the same $50,000 out-of-pocket, but your equity is now $70,000 ($50,000 + $20,000) including the 10% price discount.

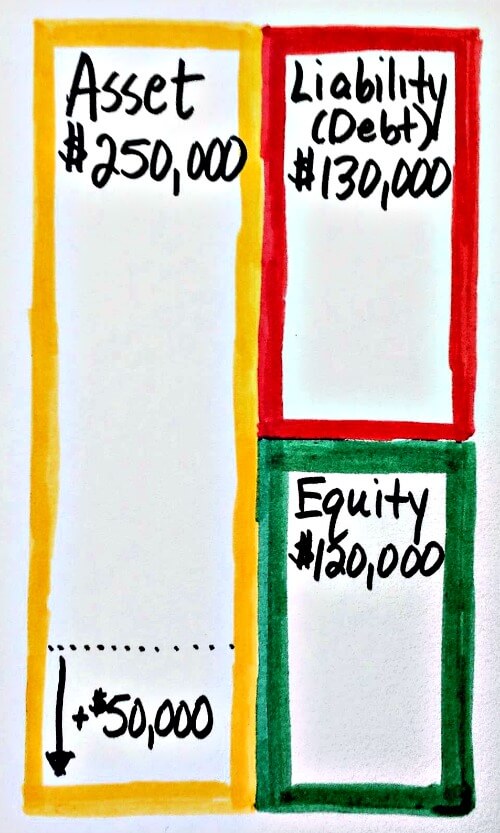

Example #3 – 10% Discount + Forced Appreciation

In this example, you again pay $180,000 for the $200,000 property, you still put $50,000 down, and you again borrow $130,000. But you see an opportunity to invest an additional $25,000 into property improvements that will increase the total value by $50,000 to $250,000.

Now your equity looks like this:

You spend $75,000 out-of-pocket, but your equity is now $120,000 including the original price discount and the forced appreciation from your improvements ($50,000 + $20,000 + $50,000 = $120,000).

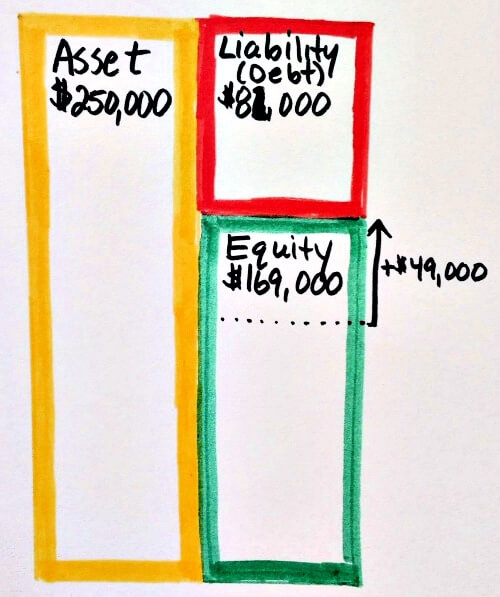

4 – 10% Discount + Forced Appreciation + Principal Paydown

In this example, you again pay $180,000 for the $200,000 property, you still put $50,000 down, you again borrow $130,000, and you again invest $25,000 to increase the total value to $250,000. But you now hold the property for 10 years and allow your net rents to pay down the mortgage principal balance.

I’ll assume that the mortgage had a 5% interest rate, a 20-year amortization, a payment of $858, and the net income at least covered the mortgage payment or more. Using my trusty online amortization calculator, I learn that my mortgage balance in 10 years will be around $81,000.

After 10 years, your equity now looks like this:

You spend $75,000 out-of-pocket up front, but 10 years later, your equity is now $169,000 including the original price discount, the forced appreciation, and the $49,000 of principal paydown during the holding period ($50,000 + $20,000 + $50,000 + $49,000 = $169,000) .

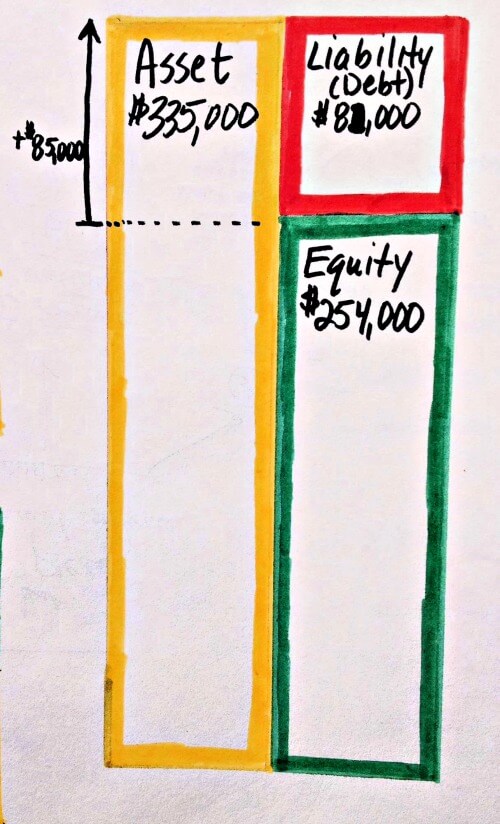

5 – 10% Discount + Forced Appreciation + Principal Paydown + Appreciation

In this example, everything is the same. Once again you also hold the property for 10 years while your net rents pay down the mortgage principal. But this time, the original full price of $250,000 after improvements passively appreciates by 3% per year to approximately $335,000.

After 10 years, your equity now looks like this:

You spend $75,000 out-of-pocket up front, but 10 years later, your equity is now $254,000 including the original price discount, the forced appreciation, the principal paydown, and the 3% passive appreciation during the holding period ($50,000 + $20,000 + $50,000 + $49,000 + $85,000 = $254,000)

As an aside, isn’t this impressive to see the potential equity growth of real estate over just a decade?! And this does not include any potential income benefits or outlandish appreciation assumptions.

** For bonus points, in scenario #5 what is the investor’s compounded annual rate of return over 10 years beginning with $75,000 and ending with $254,000 of equity? Ignore income or tax implications. Leave your answer in the comments section below so we can all compare notes.

A Note About the Fuzziness of Future Value

Forecasts may tell you a great deal about the forecaster; they tell you nothing about the future.”

Warren Buffett

The equity calculations above rely on the estimate of the property’s value. But as I said in the section on income, the entire process of calculating your equity is unavoidably fuzzy and speculative.

Why is this? Because calculating the present value of a property is an inexact science. Just ask any appraiser, or better yet read their disclaimer in the appraisal itself! And when you add the uncertainty of the future to that already imprecise value calculation, the picture gets even fuzzier.

This means you will need to decide how much you depend upon future predictions that are outside of your control. For me, I like to have equity growth WITHOUT counting on passive appreciation. If my property appreciates (which has certainly happened to me in the past), then I just get bonus returns.

This means that my BOE equity analysis just uses the future calculations that I can reasonably control, which include:

- the discount achieved at the time of purchase

- forced appreciation from improvements

- pay down of the mortgage principal

If, as in equity example #4 above, I can more than double my money from $75,000 to $169,000 in 10 years WITHOUT passive appreciation, I like the deal. But if I have very little equity growth without counting on passive appreciation, I need to make sure the income compensates me for that speculation. And if both income and equity calculations are unacceptable without appreciation, I will move on to another deal.

So, should you include passive appreciation in your equity calculation? It’s up to you. Some investors do. But just know that even in the best of locations, it is a more speculative form of investing than building in equity growth from those other sources.

Putting it All Together – The Entire BOE Process

You’ve looked at a lot of numbers and calculations so far! But let’s wrap this up to make these tools something you can use in your personal investments.

Here is the BOE analysis process in a nutshell:

- Find a potential property to evaluate

- Study current market rents and current operating expenses (or for quick analysis use the 50% rule)

- Create a snapshot of the property’s income by calculating:

- the Gross Rent Multiplier (GRM)

- 1% rule

- Cap Rate

- Net Income After Financing

- Cash-on-Cash Return (ConC)

- Study comparable sales in order to estimate the current value or the After Repair Value (ARV)

- Create a snapshot of equity by calculating:

- Current equity (Full value – debt balance)

- Future equity (Full value – future debt balance)

Now, you have numbers scribbled on your envelope. What’s next? And how will this help you buy profitable rental properties?

How Faster Decisions Leads to Better Deals

With your BOE snapshot in hand, you can now compare the deal numbers to your investment property goals. And this comparison – reality vs goals – is where the critical investment decisions are made.

The typical process works like this:

- Set your goals.

- Hunt for deals.

- Compare the potential deals to your goals.

- Make decisions.

Your decision could be to purchase a potential property for its current asking price. Or you may decide to make a lower offer that does meet your criteria. Or you may choose to walk away and pursue other deals.

But whatever you decide, the BOE analysis tool can help you do it more confidently and more quickly.

And making decisions quickly is important because buying good deals is a numbers game. You must look at a lot of losers before you find a winner.

When I began investing, a smart teacher told me that I would need to look at and analyze 100 properties before my initial real estate investing lessons could really soak in. After looking at and analyzing thousands of properties myself, I know the teacher was right!

So, if you want to improve your skills as an investor, the 100 property exercise would be a smart place to start. It will give you an opportunity to practice running these back-of-the-envelope numbers, and you might even stumble upon a deal along the way!

Conclusion

This article was all about running the numbers for rental properties on the back of an envelope. The idea was to give you a quick yet effective tool that you can use to buy more rental properties.

If you still love spreadsheets (like I do), don’t worry. There is still a time and a place for in-depth analysis during a due diligence stage. But the most effective real estate investment pros I know do this quick style of math on the back of an envelope (or even in their head) while out in the field looking at deals. I highly recommend you add it as a tool in your own real estate investing toolbox.

I wish you the best in your rental property hunting!

What were the biggest takeaways for you from the article? Will you use back-of-the-envelope analysis for your real estate investments? Do you have a different approach to analyzing deals?

I’d love to hear from you in the comments below.