What Suze Orman Got Wrong About the FIRE Movement

Recently my friend Paula Pant interviewed the matriarch of money, Suze Orman on her podcast Afford Anything. Less than 2 minutes into the interview, the conversation got very interesting:

“Have you heard of the FIRE movement?,” Paula asked.

“Yes, of course I have,” Suze said. “And I hate it.”

“Really?”

“I hate it, I hate it, I hate it,” she said. “And Let. Me. Tell. You. Why.”

Piqued your interest? It certainly caught my attention when Paula told me these lines at FinCon in Orlando before the episode aired!

As a 38-year-old member of the FIRE community and recent author of the book Retire Early With Real Estate, you better believe Suze was aiming her jabs directly at people like me! But I have some thoughts of my own on the strong opinions Suze expressed in the interview.

And in the rest of this article, I’ll share what I think Suze got right and what I think she got wrong about the FIRE movement.

What Suze Got Right

Overall I think the interview was wonderful publicity for the FIRE movement, for Paula, and for Suze (which is no accident from a media veteran on a book tour, of course). And below the slightly arrogant tone of Suze’s delivery, she’s a smart person with a lot of valuable financial experience to share.

As Paula said after the interview, we should all make a practice of listening deeply to others (especially if you disagree). If you can reserve judgment temporarily, you can always learn something.

Suze spent much of the interview pointing out that people retiring in their 30s or 40s on anything less than $10 million are naive. According to her, people in the FIRE movement haven’t considered the MANY unexpected catastrophes that could wreck our future finances.

From permanent disabilities to medical calamities to natural disasters that wipe out real estate portfolios, life can throw us VERY expensive curveballs.

So, Suze’s right!

Unexpected and Expensive Catastrophes Can Happen

Expensive black swan events (i.e. unexpected and rare) could happen to any of us. And it’s smart to prepare financially (and emotionally) just in case.

Suze also expressed concerns about an uncertain economic future. What happens to our economy if AI (i.e. artificial intelligence machines) replaces 25% of our workforce? She predicted economic strains to our investment portfolios and to government finances.

One possible result would be higher taxes to pay for the exploding costs of social safety nets for displaced workers. And that could mean less money to live on from our investment portfolio.

Could that happen? It’s possible. And to Suze’s point, we certainly should prepare for it.

But Technological Disruption Is Nothing New

I would also remind Suze, however, that in 1870 almost 50% of the U.S. population worked in farming. As of 2006, less than 2% of the population worked in farming because technology reduced the need for farm laborers.

In a 2018 Time Magazine editorial, Warren Buffett said this about that unprecedented technological disruption of farming:

“We know today that the staggering productivity gains in farming were a blessing. They freed nearly 80% of the nation’s workforce to redeploy their efforts into new industries that have changed our way of life.”

New technology has disrupted our societies as long as human beings have been around. And yes, the pace of change is much faster right now. But it’s also possible that our economy, government, and job market will adapt positively to these changes. The economic pie could get even bigger over the long run.

Warren Buffett thinks so:

“This game of economic miracles is in its early innings. Americans will benefit from far more and better “stuff” in the future.”

And that leads me to the three key points Suze got wrong about the FIRE movement.

What Suze Got Wrong

I found myself sometimes laughing and shaking my head in certain parts of the interview. It’s difficult for me to remain serious listening to boastful “I’m the money matriarch of the world” and “the FIRE movement is getting a Suze slapdown.”

But show(wo)manship is what Suze does. In the end, I can look past that.

My issues were more about her misunderstanding of the FIRE movement itself. I think Suze (and many other traditional financial thinkers) miss important nuances that make the concept of financial independence early in life so popular (and reasonable.)

I’ll begin with the loaded word retirement.

1. Our Definitions of Retirement Aren’t the Same

To many people, retirement means withdrawal. You quit work, let your assets (or a pension) support you, and retreat into a life of leisure.

Suze and many others who hear “early RETIREMENT” immediately think of 30-somethings doing this:

Or if we’re not on a beach, we must be on a couch all day, playing video games, and eating ourselves into Cheetos-induced comas.

I’m sure there are early retirees sipping piña coladas and sitting around eating Cheetos on couches. If so, you won’t get any judgment from me!

But in reality, the early retirees I know are MORE engaged in life than before. They’re living on purpose. They’re doing more of what matters!

What does this purposeful engagement look like? It varies as widely and beautifully as the variety of people within the FIRE movement.

What Early Retirement Looks Like For Me

In the case of my early retirement, I’ve been doing things like traveling with my family on a 17-month sabbatical/mini-retirement and trying to be a better husband and father.

I’ve also enjoyed staying fit and physically active, especially with pick-up basketball.

And during much of my time, I still work!

*GASP!*

The difference, of course, is that work for an early retiree has less to do with money and more to do with passion. We find projects and causes we love, and we throw ourselves into them.

During a typical week, I spend work time (unpaid) trying to improve walking and biking infrastructure in my hometown of Clemson, South Carolina (Go Green Crescent Trail!).

I also wrote a book (which will pay me some money), and I regularly write on this blog (which pays me very little).

And I still manage my real estate business from a high-level, pay bills, and sometimes acquire or sell properties. The real estate time commitment can range from 2 to 20+ hours per week, depending on the time of year (like when taxes are due).

So, the chastising Suze gave early retirees and the FIRE movement about somehow forgetting to engage with life is silly. In fact, the truth is the exact opposite!

And this leads me to the primary topic Suze addressed in her interview with Paula – risk.

2. Financial Risk Isn’t Even the Greatest Risk in Life

Suze was deeply concerned about risk. She’s seen first-hand calamities in life that destroyed the financial plans of her clients and audience members.

For example, she’s seen permanent disabilities wreck people’s finances. A once active person could get into an auto accident and become bed-bound for life. Not only could they not produce income, but their medical expenses would be permanently higher.

Would an early retiree be able to withstand this long-term financial shock? Would they be able to (or even choose to) get disability insurance?

And what about serious medical conditions like cancer? Could an early retiree who budgeted $50,000/year be able to suddenly pay their out-of-pocket medical costs every year?

These are real concerns. I appreciate Suze reminding us to plan for these possibilities.

But why did she stop with these risks? Some of the more likely and much more grave risks aren’t even financial.

The Ultimate Risk of Regret

“People are frugal in guarding their personal property; but as soon as it comes to squandering time they are most wasteful of the one thing in which it is right to be stingy.”

– Seneca, On the Shortness of Life

Time, not money, is the most precious resource of life. And the greatest risk is wasting the time that is given to you.

Here’s another way to think about that:

What will you regret most on your death-bed?

Is it bankruptcy and financial ruin? I certainly don’t like imagining those. But they’re not even the first regrets that come to my mind. Instead, I would regret:

- spending 12 hours per day working a job while my kids grew up without my presence.

- wondering what might have been if I gave more of myself to my marriage instead of just to my job.

- missing opportunities to travel and explore the world while I was still active and healthy enough to enjoy it.

Does that mean you should throw caution to the wind and live only for the moment? Of course not!

But making life decisions based on absolute financial security and fear of the future is as ridiculous as building your life around pleasure in the present.

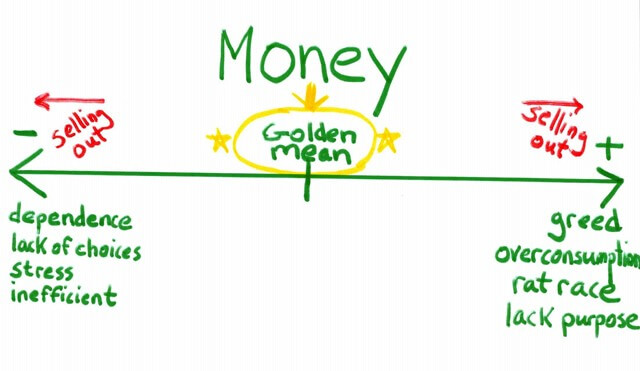

The Golden Mean of Money

As I shared in my Money-Life Manifesto, the ancient philosopher Aristotle taught that there’s always a middle around – a golden mean. For example, courage is a virtue (i.e. a good thing). But you can use courage too much or too little:

And you can do the same thing with money and financial security.

Do you want absolute financial security? Then work a grinding job for 50 years and build your whole life around earning money.

Do you want the maximum enjoyment of life right now? Then go travel, eat, drink, and be merry until your money is all gone in your 30s.

Or do you want the golden mean? Then work hard AND retire early and often (as Paula Pant says).

Smart early retirees make long-term financial goals. They save a large percentage of their income. And they plan to build wealth for the rest of their lives.

But they also take mini-retirements. They enjoy the many financial plateaus along the way. And they build in flexibility, entrepreneurial skills, and backup plans for true security.

In other words, the golden mean of retirement is to let neither the destination nor the journey dominate your life. Instead, walk the line of your golden mean by keeping your eyes on the peak while also enjoying the climb.

And that financial climb leads me to the final issue I had with Suze’s interview – early retirees running out of money.

3. An Anti-Fragile Approach to Early Retirement

At the heart of Suze’s hate of the FIRE movement was our apparent recklessness. Clearly, we must be underestimating our future financial needs by only saving portfolios of $1 to 2 million and calling ourselves “retired.”

Or in Suze’s words, we’re going to run out of money and get “burned!”

I seriously doubt Suze read the carefully considered withdrawal plans of my FIRE friends like Tanja at OurNextLife.com, Leif at PhysicianonFire.com, or Karsten at EarlyRetirementNow.com. And I doubt even more she’s read my own Rental Retirement Strategy (Or How to Not Run Out of Money).

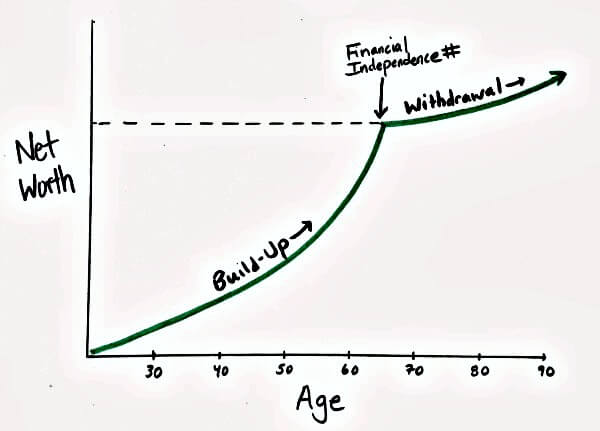

The truth is that few early retirees count on mindlessly living off their portfolios. Withdrawal after financial independence is a dynamic, active process.

And in my case, I practice a real estate-based variation of the “income floor + upside investing” strategy of Darrow Kirkpatrick at CanIRetireYet.com.

Using Real Estate For Income and Long-Term Growth

On the one hand, current income is a priority. My wife and I need to pay for our family’s needs. And we do that primarily with rental income.

Suze said that “$2 million is nothing … it’s pennies in today’s world.” But $2 million invested in a conservative real estate portfolio can produce $120,000 per year of income at a conservative 6% cash on cash return.

$120,000 per year won’t buy a private island, but where I come from, it covers an abundance of current living expenses, insurance of all kind, and even luxuries.

That rental income also doesn’t reduce your investment principle (which makes it hard to run out). And in the right locations, the equity of your portfolio could even continue to increase with property appreciation and mortgage pay down.

So, the goal isn’t to stop wealth building at early retirement. The goal is to live off current income while also growing your wealth and income enough to outpace inflation and other contingencies.

But Don’t Forget About Diversification

But depending too much on real estate (or any single asset class) has its own risks. My friend and long-time early retiree Todd Tresidder wrote in his excellent book How Much Money Do You Need to Retire:

You should be no more willing to bet your entire retirement on an insurance company’s ability to pay an annuity than you would rely on the government to honor its promises for Social Security. It’s okay to make each one a piece of your retirement equation, but each income source has risks that must be managed. Never leave yourself exposed to a single default that can wipe out your financial security.

Todd’s message is clear. Diversify your income and wealth building sources!

In my case, a move from a large concentration of real estate into more equities, bonds/debt, and perhaps commodities makes sense. For some of you with traditional portfolios, an opposite move into real estate may be in order.

But the common theme is that diversification is a key component of successfully surviving (and thriving) during inevitable ups and downs in the future.

And beyond diversification of your investment portfolio, smart early retirees also have backup plans.

Early Retirement Back-Up Plans

“If plan A doesn’t work, the alphabet has 25 more letters – 204 if you’re in Japan.”

– Claire Cook, Seven Year Switch

The primary early retirement plan for me and my wife is to live off our real estate investment income (without touching any principle). If all goes well, these investment assets will be intact and still growing to support us even better later in life.

But if not, our first and most important backup plans are our retirement accounts. At 38 and 41 years old, we don’t plan to touch those accounts until well after turning 60 years old. And even without future contributions (which we do plan to make), it’s very possible that these accounts will be worth $2 to $3 million after growing and compounding tax-free for 20 to 30 years.

And beyond retirement accounts, I wrote extensively about other backup plans in my book Retire Early With Real Estate. Here’s a summary list of those ideas:

- Live more simply, frugally, and happily – spending less isn’t always a bad thing. Even in a financial pinch, you may find that a simple life is, in fact, a happier life.

- Practice location arbitrage – My family and I spent 17 months in Ecuador and lived like royalty for $3,000/month (including private schools and good health care). There are many low-cost living opportunities around the world and within the US and Canada.

- Downsize or get creative with housing – Home equity isn’t an optimized investment. In a pinch, you could sell and downsize (or even rent) to save money. You could also earn income from your housing using the classic house hacking technique.

- Buy and sell properties – For those of us investing in real estate, buying a couple of extra fixer-upper houses to flip each year is very reasonable. At $20,000 to $30,000 per sale, this can be a solid source of potential extra income.

- Side Work or Side Hustle Business – This may not be possible if we’re in bad health, but it’s very reasonable to think we could make a little money on the side. Just $20,000 per year is the equivalent of retirement savings of $500,000 at a 4% withdrawal rate. So, a little income goes a long way.

- Sell a rental – This backup plan essentially eats into your principle. If you have enough principle elsewhere (like in a retirement account that you can’t yet access) selling a rental could make sense.

- Refinance a rental – Instead of selling, you could also refinance and pull out a big chunk of cash funds tax-free. Yes, you’d have a mortgage payment and increased risk. But done responsibly, you could just let the tenant’s rent begin to pay down the mortgage for you again. This means your net worth would once again grow.

- Seller finance a rental – Seller financing (aka an installment sale) means you sell a property, receive a down payment, and receive the balance of the price (plus interest) over time. This can be a great way to get more income passively if needed.

- Buy a Single Premium Immediate Annuity (SPIA) – This isn’t my area of expertise, but Jim Dahle at whitecoatinvestor.com call these SPIAs “the good annuity” for people in certain situations. They’re lower cost and free of the complex contracts of many other annuities.

- Reverse mortgage – Like annuities, reverse mortgages are controversial because they often have high fees and complex terms. But if you have a lot of equity in your home and don’t want to sell, it can be a backup source of income later in retirement.

So, will a solid early retirement portfolio, retirement accounts, and backup plans be enough to cover every single contingency? Maybe not 100%.

But do I sleep well at night? Absolutely.

And when I wake up from that sleep, I get a chance to do what matters and live a life I won’t regret.

That’s a risk-reward tradeoff I’ll take any day.

A Gift From Suze Orman

In the end, Paula’s interview with Suze Orman is a gift to the FIRE movement. It’s given us an opportunity to reflect and learn from a veteran of the financial industry. And it’s sure to bring even more attention to the idea of gaining financial independence earlier in life.

I also hope this article has helped to correct a few of the issues Suze got wrong:

- Early retirees are not withdrawing from life. They’re embracing a purposeful life MORE fully than ever.

- Early retirees are not wild risk-takers. They are calculated risk-takers. They see the old bargain of a 9-to-5 job until they’re 70 as riskier than an early-retirement.

- The retirement plans of most early retirees aren’t naive, fragile castles built on sand. At least the ones I know of are anti-fragile, multilayered, flexible plans built on a combination of investment savings, retirement accounts, side businesses, and backup plans.

What will the FIRE movement look like in the future? The next market downturn will certainly upset or delay some plans. And I’m sure the paths of most early retirees will have serious ups and downs.

But the movement is here to stay. The secret is out. You don’t have to delay the good life until you reach “retirement age.” You can work hard, save money, retire early and often, and do more of what matters.

Have you listened to the Suze Orman interview? What did Suze get right about the FIRE movement? What did she get wrong? I’d love to hear from you in the comments.