Let’s be honest. Rental properties are fun and interesting, but what we really want is the large, steady rental income they will give us for many years to come.

That’s a fine motivation.

After all, this money can help you do more of what matters. And that’s exactly the point.

So, I’d like to share a case study about Lisa and Todd, a hard-working, money-saving, real estate loving couple in their 40’s who create a $100,000 per year rental income within approximately 20 years.

Todd and Lisa are not real people, but their situation is based upon real principles, concepts, and numbers I have encountered in my own business and in those of my coaching clients. I hope this case study will remind you of what’s possible with real estate rental properties.

Let’s get started.

The Background

Here’s a snapshot of Lisa and Todd’s financial situation as they begin their journey to create income from rental properties.

- Combined Lisa and Todd earn $100,000 per year

- Lisa owns her own business and Todd has a normal salaried job

- They each have 780+ credit scores

- Todd has $50,000 in his 401k at work

- Lisa has $30,000 in her Roth IRA

- They have $150,000 in cash savings (from flipping real estate, sale of stocks, inheritance, savings, etc)

- They can save an extra $2,500/month going forward

- The own a home worth $250,000 and they owe $100,000

- They can get a HELOC (Home Equity Line of Credit) for 80% of their home’s value

Lisa and Todd know they want to own rental properties. They were probably convinced (as I was) after reading Building Wealth One House at a Time.

Like all of us, they are busy with jobs, family, and other interests. So they don’t want to spend all of their time with real estate investing over the long run. They want a small and simple life style business, not a big albatross of a business around their neck.

A relatively small number like 7-10 houses would be a reasonable amount for them to manage long run. Because these houses would be in decent neighborhoods, they’d attract responsible, self-sufficient tenants that would make it even more passive.

Now let’s move on to the 5-step plan Lisa and Todd use to accomplish their goal of $100,000 per year in rental income.

Step #1 – Preparation

To accomplish this plan Lisa and Todd must find two things:

- The money

- Good deals

Easier said than done, I know.

For the money Todd and Lisa ultimately plan to use conventional mortgages. Their mortgage broker has preapproved them for up to six conventional, 30-year loans on investment properties with 25% down at a rate of 5%. If they run into hurdles with conventional financing down the road, they’ll also explore private financing or portfolio lenders at local banks.

But they won’t use these loans to BUY properties. Only to refinance.

They learned from reading the Coach Carson newsletter that speed is key when buying properties below value (like my personal record purchase in 3 days). Bank loans are too slow for purchases. The best deals require fast, available funds without a series of hurdles and delays.

So Todd and Lisa’s plan is to use cash for purchases and then refinance with conventional loans 6 months later after seasoning the properties.

After some work, their total access to cash includes:

$150,000 = cash savings

$100,000 = proceeds from an 80% HELOC on their principal residence

$250,000 = Total Cash Available

The couple also plans to save $2,500/month from their job income, so they will add $2,500 x 12 = $30,000 more to the cash stash each year.

They begin to shop for houses in their home location of Greenville County, South Carolina. They hunt for solid single family neighborhoods whose median price is about $160,000 per house.

Each weekend they ride and walk around neighborhoods to get a feel for the places where they want to invest (and where they don’t). They also get market statistics to become very familiar with the numbers for their target properties.

Step #2 – Acquisition

Lisa and Todd quickly recognize that free time and expertise are two qualities they lack. So they hire an experienced real estate agent to represent them as a buyer’s agent. This agent will help them find and evaluate all of their deals.

They choose this agent because she also has experience with rental properties. She understands how to hustle and move fast on good deals. And she is able and willing to evaluate not only the resale value but also the rental values and operating expenses of the properties they find.

The couple and their agent look and make offers on many properties beginning in the summer and fall of 2016.

After months of searching, on January 1, 2017 they purchase Properties #1 and #2.

Six months later on June 1, 2017 they refinance Properties #1 and #2, and they purchase Property #3. A refinance of Property #3 happens by December 1, 2017, and one year later before December 1, 2018 they buy and refinance two more properties for a total of five rentals all together.

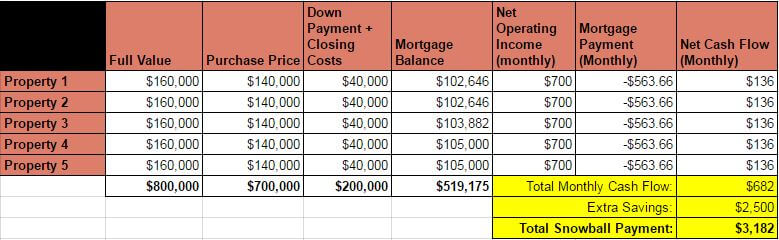

Each property is rented for $1,200 per month and has $500 of operating expenses. The resulting net operating income per property is $700 per month.

So, here is the financial picture of the properties and their mortgages towards the end of 2018, two years after the first acquisition:

What does all of this mean after the dust settles at the end of year #2?

It means they have a solid foundation to begin the Snowball phase, where they REALLY grow their equity and cash flow.

Step #3: Snowball! (Part 1)

Remember from step #1 that Todd and Lisa are willing to save an extra $2,500 per month from their jobs? In years 1 and 2 they used that money to help them have more cash for acquisitions and down payments.

But in year #3, they combine that $2,500 with the $682/month in positive cash flow to save a total of $3,182 each month.

Now here’s where discipline meets planning to really add some horse power to their wealth building.

On January 1st of 2019 (beginning of year #3), the couple decides to use this $3,182 per month to start a Debt Snowball Plan. The Debt Snowball concentrates all of the extra cash flow on one mortgage at a time in order to pay it off faster.

Like rolling a snowball, this plan starts slowly and then quickly gains enormous financial momentum as success compounds over time. The end result of a Snowball Plan is that mortgages with 30-year terms get paid off in MUCH less time.

How much less?

Let’s see how it works in this case study.

The Snowball Plan begins on January 1, 2019. Todd and Lisa now combine the extra snowball payment of $3,182 with the mortgage payment of $563.66 on Property #1 for a total payment of $3,745.66. This huge payment accelerates the payoff time of the mortgage, and as each mortgage is paid off the growing cash flow is applied to the next mortgage.

With a Snowball Plan Excel Spreadsheet to help me with the calculations (I used this one at Vertex42.com), here are the results and timelines of this plan:

- Property #1 is paid off by June 1, 2021.

- Property #2 is paid off by June 1, 2023.

- Property #3 is paid off by February 1, 2025.

- Property #4 is paid off by August 1, 2026.

- Property #5 is paid off by December 1, 2027.

Did you notice how the pace of debt payoff accelerated towards the end? That’s the power of a plan like the Debt Snowball. It keeps feeding and compounding on its own success.

So, just under 11 years after their first acquisition, our disciplined and hardworking couple has 5 houses free and clear of all debt. Without accounting for any appreciation, the financial scorecard looks like this:

Todd and Lisa now have 5 properties that produce $3,500 per month or $42,000 per year. They also have total equity of $800,000.

Do I think the rent and value of these properties will have actually appreciated? With the long-term prospects of this region in South Carolina and with the solid locations of the properties, I would guess they will at least keep up with inflation at 2-3%.

In the case of 2% appreciation the results would look more like this (I used this future value calculator to calculate these numbers):

But I don’t have unlimited confidence in my ability to predict the future of appreciation. So, I like that Todd and Lisa have a solid growth plan whether or not their properties appreciate.

At this point Todd and Lisa could decide that after 11 years this is enough to satisfy their needs and just stop here.

Or they could take a rest with a well-deserved mini-retirement.

Or they could just change their pace and switch to a part-time or enjoyable work schedule of semi-retirement.

But let’s assume they’re a little more ambitious (or paranoid about the future!) and want to continue the climb towards $100,000 per year in rental income. Here’s what they do.

Step #4: Preparations and Acquisitions (Part 2)

Todd and Lisa decide they are willing to work for a few more years, buy five more rental properties, and build their rental income to over $100,000 per year.

Here is the money plan for this stage of growth:

- Use a HELOC of $267,500 on their principal residence (now free clear and worth $315,000) for cash acquisition money

- Refinance rental Property #1 and #2 ($122,500 each) to raise $245,000 for down payments and closing costs

So, their total available cash to start buying properties is:

$267,500

+$245,000

= $512,500 available cash for acquisitions

With this big wad of cash and even more real estate experience, Todd and Lisa feel very confident that they can find and acquire quality single family properties worth $200,000 at a 15% discount of $170,000.

Their down payment on each property will be 25% or $42,500 and closing costs for each purchase and refinance will be $6,500. The loan terms will be 6%, 30-year loans.

After 3 months of preparations and searching, on April 1st, 2028 they purchase 3 properties. Six months later on October 1, 2028 they refinance those three and purchase 2 more.

By April 1, 2029 they have refinanced all 5 new rentals, and they are ready to begin Snowballing debt again.

Step #5: Snowball! (Part 2)

Now that acquisitions are finished and all refinances are complete, Todd and Lisa are ready to renew their Snowball Plan one final time.

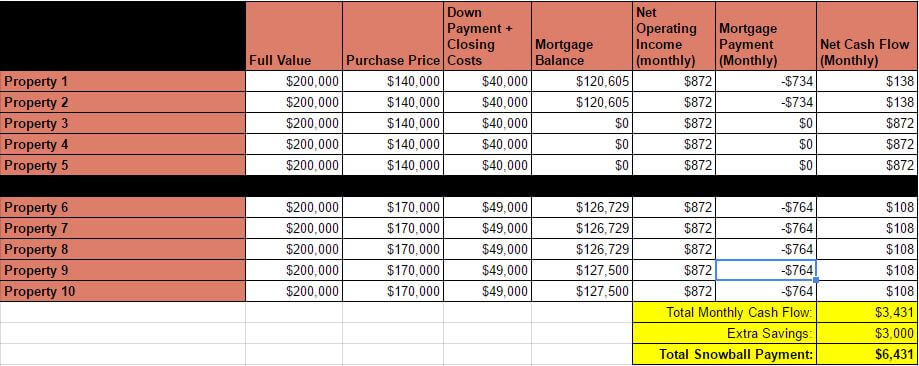

Here is what their portfolio of properties and mortgages looks like as of April 1st, 2029 when they begin the Snowball Plan again:

This time around, Todd and Lisa increase their savings to $3,000 per month to increase their snowball. Combined with their net rental cash flow they have a whopping snowball payment of $6,431 per month.

Using my Snowball spreadsheet again (this one at Vertex42.com), here are the Snowball Plan debt payoff results:

- Property 1: paid off by October 1st, 2030

- Property 2: paid off by February 1st, 2032

- Property 6: paid off by April 1, 2033

- Property 7: paid off by June 1, 2034

- Property 8: paid off by May 1, 2035

- Property 9: paid off by April 1, 2036

- Property 10: paid off by February 1, 2037

Finally! The Snowball Plan is done. This time the Snowball Plan only took 8 years and 3 months.

Lisa and Todd now own 10 rental properties free and clear of any debt!

But did they reach their goal of $100,000 per year rental income? Let’s see the financials of Todd and Lisa’s rental properties in the end, assuming a 2% appreciation rate from the values when they started 20 years earlier:

Todd and Lisa accomplished their goal!

At an age somewhere in their 60’s, they have a steady flow of over $125,000 per year in rental income that will support them for the rest of their lives. They also have over $2,385,000 equity in single family houses that can be sold or refinanced if large chunks of cash are needed in the future.

The True Purpose of This Case Study

As you all know, the one thing we know about a plan like this is that it will never work exactly as planned!

And there are many variations on this plan or in my assumptions that could make it much better (or much worse).

But can you see how creating a plan gives you a path to follow? It guides your actions and decisions in the present. As circumstances, the economy, financing, or any other variable changes, you can then change your plan as needed.

I also love a plan like this because it’s inspiring. When you see a case study where it works for someone else, it’s easier to believe it’s possible for yourself.

So the true purpose of this case study is to challenge you to think, to plan, and to take action. Real estate rental properties are a wonderful vehicle to build wealth and cash flow. But the most important rental property plan is the one you begin executing for yourself.

I wish you much success in your investing efforts!

What do you think about the case study? Could something like this work for you? Are there alternatives to this plan that work better? I’d love to hear from you in the comments section below.

Enthusiastically your Coach,

Get My Free Real Estate Investing Toolkit!

Enter your email address and click "Get Toolkit"

Hi Chad. We have a decent portfolio of holdings not far from you spread around N. half of GA. So you know the price point advantage we had buying. BUT never the less one needs to be financially prudent when buying rentals. I’d NEVER go into a deal with only $136/mo positive cash flow!! That is crazy risky. Plus it hits the “why bother” button loud and clear.

I don’t like turn-key rentals but if you can’t buy near the 1% rule in this couples area, then move to an area where one gets more than $136 / mo positive cash flow.

You ended on a note that this map may not be perfect, but at least it’s a map. But you didn;t say where the flaws and risks where and that was ending a few paragraphs too short in my view. 🙂

Tnx much Chad, curt

Hey Curt,

I appreciate your comments. I don’t disagree that getting better cash flow deals than I presented here would be nice. And personally I do much better every day. But with this case study I tried to show how average deals could still produce an above average result when executed well. Many people, especially part-time investors, are going to make decisions between these types of deals and more speculative, enticing deals that have even more hidden risks.

I’d call the deals I presented average, but that is different than “crazy risky.” These deals were bought 10-15% below full value and at approximately a 6% cap rate. The financing was 30-year fixed at 5%. The locations were solid, median-priced areas near jobs and growth. They would be very easy to rent and to keep rented. They were also in the couple’s home location, where they could keep a close eye one them.

People do crazy risky things in the investment world all the time. Speculative ventures in real estate, stocks, gold, etc never cease to amaze me. But buying an income property that has positive cash flow, even if smaller than ideal, and aggressively paying it off is not speculative. I would encourage people to learn techniques to buy them even better, but the point is that it can still work with average deals – and work well.

Thanks again. Nice to hear your views.

Absolutely! The nice thing is how few transactions are required – you don’t have to constantly be looking for deals, you only have to purchase 10 properties in 20 years. Pointing that out, plus that you can outsource the landlording can help people get past the mental hurdle.

I’d love if you could share more examples from actual clients you work with. Even though they aren’t 20 years in, we can get an idea for what their plan is.

Thanks for the comment, Brian. Good point about doing very few deals over the 20 year period. I like that, too. Less motion, less frenzy, just consistent progress.

If this case study goes over well, I plan to introduce more in the near future. I’ll start digging for more stories from clients that I’ve worked with and my own deals to give a variety of property types and approaches. Thanks for the suggestion.

Hi chad, good article. I’m am doing close to this strategy with the exception of the debt snowball. I’m 28 and have 5 properties, my goal is to have 10 by age 30 and 20 by age 35.

I’m curious on your thoughts of reinvesting cash flow into more properties instead of paying down debt. After all 6-10% cap rates, and 20+% leveraged cash on cash returns are higher than the 4-5% return of paying down fixed rate debt.

What I’m currently doing is taking the $20,000k plus positive cash flow as well as 50% of my salary and using it to buy forclosures cash, then refinance and repeat.

Also, rates are bound to go up in the next few years, so why not lock in as much low fixed debt as you can as long as the cash flow numbers work?

Thanks! I enjoy all your articles

Hi Asher,

You ask a really good question. I don’t know your entire situation, but at your age and with a long time-horizon, low interest rates, and a solid plan, I have no argument with your approach. Using cash flow to fund growth before you start paying down is exactly what I’ve done as well.

My investor/writer colleague in Texas, Erion Shehaj, wrote a great article responding to this very issue. You might also like his comments: https://www.biggerpockets.com/renewsblog/2013/02/14/pay-down-debt-recycle-cashflow/

The tough decisions in this issue start to come when you focus more on life equations and less on math/return equations. What I mean is that at some point it’s nice to live off the income, stop working so much, and reduce headaches and risk. Growth % is great when you’re in growth mode, but when you’re in harvest mode – cash flow, low risk, and low hassle are the keys. That is best accomplished, in my opinion, with a smaller, less leveraged portfolio.

The question is WHEN do you start harvesting? 10 properties? 20? 30? At 35 years old or 75? I like enjoying the peaks and plateaus. I want to keep maximizing growth (the peak), but I want to live and enjoy now (the plateaus). So I’ve gone through periods of paydown where I get to a plateau of cash flow, and then take a break. Then after a break, I start working hard and investing in growth again. It’s not mathematically the most efficient, but it’s DEFINITELY been the most rich in terms of life experiences.

We all have to find our preferred comfort zone, but hope that helps you think about it.

Can you still get tax breaks for dependants even if your income is only rental income?

I’m not a CPA, so it’d be better to ask someone like that. But I believe you can still get tax breaks for dependents with rental income.

Coach Carson,

STOP, Calling My Phone ….

Hi Patricia, I don’t ever do any outbound phone calls (or even have people’s phone number). So, it’s not me if you’re getting calls.

How does inflation affect all of this? And since you are using leverage to buy individual properties (and other factors), isn’t this more risky than stocks. If they got their HELOC and invested all of their money into ETFs that cover the S&P 500 (or similar index’s), how would that strategy compare to this one? It seems that the stock market route would be of equal or lesser risk (over a long time horizon) and would provide a similar expected return for absolutely no effort/headache.

Coach-

In Step 1, you say, “Their mortgage broker has preapproved them for up to six conventional, 30-year loans on investment properties with 25% down at a rate of 5%”.

1. How does one go about doing such a thing?

2. Are the loans pre-approved for a particular amount?

Forgive me, didn’t really understand the basic assumption….

Love your site, podcasts, etc!

This is a great breakdown of how to start this business. There are so many variables it helps to see a scenario in a few different ways. Thanks!

What happens when both husband and wife are no longer working because of the pandemic and can’t pay for the mortgages on all their homes? Unemployment will not pay the bills, their health insurance is gone, and he/she is in the hospital with Covid 19. Few folks are traveling and fewer folks trust short term rentals because many investors are involved in money laundering, out of country cartels, or not even in the state? See the BBC report on Vancouver’s money laundering rentals.Elaine

Hi Elaine, Happy and successful new year! I have to reply to help ease your worries. And I’m sure Chad can offer results from his portfolio over the past 10 months in SC, where I’m in North half of GA near jobs centers.

I’m not minimizing the horror, tragedy and impact covid had or will continue to have. I’m just reporting;

– We’ve lost zero rent due to covid job loss of our tenants. Yes about 5 out of 38 doors asked for rent deferal (I don’t give rent reductions, just deferal). Everyone has cought up. Just got 1200 yesterday (erentpayments.com) from a couple who gave me both of their $600 checks to start to catch back up.

– My large network of landlords hears of near zero losses as well. Atlanta/GA area.

– Chad has alot of education on how to buy a good rental; buy in hte path of progress (jobs, job growth), target blue collar permanent renters with some skills. IE avoid lower end rental market where tenants have no skills to help them get another job. A purposeful and targeted rental business is fairly resilient I’m observing through this real time lab experiment. Everyone needs to live somewhere. Hot areas (Atlanta etc) are way under built. Home owners are again becoming renters… Own decent 3/2 houses next to jobs centers AND transpertation. IE near freeway exits.

– Buy with decent cash flow >$250, in 2-3-4 yrs with rent raises cash flow should become $400-600. This translates into bankers criteria of high DSCR >1.7 and as in some of our houses 2.0+. Cash flow (DSCR) gives your business resilency,,, along with cash reserves in the bank. At least $10k for a dozen houses. Personally we have a lot of cash, I’m just saying the reserves can be on the small side to weather roofs and ACs per year. But more cash is better no doubt.

– The owners both getting covid, is terrible, no doubt. But if you electroinically collect rent (erentpayments.com) AND you setup mortgage auto pay out of the same account rent comes into. You hjave a nearly autopilot business where tents will pay the mortgage hands free while you are laid up, OR traveling out of the country (when its possible) etc etc.

Wishing you and everyone to be safe. Wear masks, stay away from groups of people. Best to all, Curt

I completely agree with you.

Any stable business can survive and come out of a crisis if you plan everything in advance and distribute income.

Of course, profits in most cases can be forgotten during this period.

But as statistics show, some rental companies were able to grow during Covid-19.

Planned action and discipline almost always lead to success. I think two qualities are needed for financial independence. First, it is hard work and discipline. Your analysis shows how important it is not to be distracted from the goal and concentrate your attention on the main thing.

But where does one find properties at that price point? I live in San Diego and bought a 4 bedroom for 650k 2 years ago (now worth 900k) I live in one room and rent the other three to girls my age. They fully cover my mortgage and I travel for half the year and rent out my room when I’m gone (so I have positive cash flow of $1400 for my room when I’m not in it). I have saved another $70k down payment and want to make the most of it with real estate investment, but I’m not sure what the best next approach is. In these scenarios you’re using such cheap properties, I have searched all over the map except for middle America states, and can’t find anything decent near this price range. Regardless, I would be hesitant to invest in an area I don’t know and can’t easily go to. Can you do an updated version of this idea but with metropolitan 2022 prices? Like how could one make this work with properties that are in the 400k’s? For us in these popular areas your chart is hard to follow. A mortgage for us is a minimum of $2000k and rent is near the same as this or a bit less. Basically I guess I’m just trying to ask, can this be made to work here in California and with high price properties?