How to Confidently Buy An Investment Property – My Go, No-Go System

Have you ever been afraid or uncertain about a decision to buy an investment property? When you’re spending hundreds of thousands of dollars on one purchase, these feelings are normal!

The question is how you respond to the fear and uncertainty. Do you slip into analysis paralysis where you’re frozen and never make a decision? Or, do you ignore the fear, become irrationally exuberant, and take aggressive, overly optimistic risks?

I am not exempt. Unfortunately, I have experienced both of those extremes in the past.

So, to help protect myself from my own irrational decisions, I developed a Go, No-Go System that I use as a filter for investment purchases. The criteria in this system help me more confidently make purchase decisions. Even more importantly, they also help me decide to pass on some properties that are too risky.

The Go, No-Go System For Buying Investment Properties

Many investors focus first on a property’s ability to generate a profit. I actually do this too with a back of the envelope analysis and a study of my investment market fundamentals. While profits are essential, they must also be balanced against Warren Buffett’s #1 rule for investing – don’t lose money!

For Buffett and other value-oriented investors, preservation of capital (your cash investment) is the primary consideration for investment decisions. Losing your hard-earned dollars will stop or slow your journey towards financial independence faster than anything else.

So, my Go, No-Go System is a method to help me apply Buffett’s rule #1 to real estate purchases. It’s like a filter that helps me mitigate the risk of losing the money that I, my partners, and my lenders invest. If I do that, the profits tend to take care of themselves.

Now let’s jump into the 3-part Go, No-Go System for buying investment properties.

Go, No-Go Filter #1: Wholesale Price

Residential real estate markets differ from stock markets in crucial ways. With stocks, millions of people buy and sell a company each day. With real estate, ONE person might buy a certain property every 5 years or more!

Stock pricing is very accurate based on constant “votes” from the market. Until a property actually sells, real estate pricing is the best guess of an appraiser or real estate agent.

Stocks can be sold in minutes. Real estate takes months or years.

Yet, even real estate, if priced low enough can be sold VERY quickly, like my experience of purchasing a house in 3 days. So at wholesale prices, and not retail prices, real estate behaves more like the stock market.

Think about your own house that you live in. The retail value might be $250,000, and it would take months to sell at that price. But there is a price low enough that a cash investor in your area would buy it in just a few days. That’s the wholesale value.

If your total investment is less than this wholesale price, you have reduced your risk of loss.

Why is this true? Because worst case (at least in the current market) you could just dump it to an investor and get your money back.

How to Determine a Wholesale Price

The wholesale price for real estate will vary greatly depending upon your market. In some markets, the price may be 85%-90% of the full value. In others, it may be 60%.

But it’s not hard to figure out the wholesale price point for almost any piece of real estate. You just ask other investors!

For example, if you want to sell your own property at a wholesale price in my market of the Upstate of South Carolina, just give me a call :).

And in your market location, you can also ask your investor friends what they would pay for your property or for a potential investment. Don’t be insulted if it seems low. It’s just helpful information.

Once you know the wholesale price, you can use it for the Go, No-Go System.

Go, No-Go Example Using Wholesale Price

Let’s say that you’re evaluating a potential fix-and-flip investment property. You would calculate two different purchase prices.

First, figure out your higher, retail price that you hope to sell it for. A real estate agent or appraiser can help you with this. In order to get multiple estimates of retail value, you should also use your own process to calculate the ARV (after repair value).

You then use this retail value to back out a purchase price that will allow you to pay all your expenses and still make your minimum profit goal.

Secondly and more importantly, figure out the wholesale price.

If your total investment is at or below the wholesale price, you can more confidently speculate on the retail price. This is also called a margin of safety.

Should you always buy below the wholesale price? Ideally, yes. But there are no rules that apply 100% of the time.

Sometimes, especially with longer-term rental properties, I may still choose to pay more than wholesale if it also meets my criteria #2 and #3 (below).

But even in those cases, I want to know the wholesale price going in. This tells me how much of my money is at increased risk from the start. If I can financially survive that potential loss, I can confidently move ahead with the deal.

Go, No-Go Filter #2: Positive Leverage

Use of leverage (debt) is an integral strategy for many real estate investors. But in my experience, misuse of leverage is the #1 reason investors lose money. I have some negative cash flow “scars” to prove this from my own deals!

Investing using debt should be treated like carrying a loaded gun. When my dad took me bird hunting as a little boy, he wisely taught me that a gun used carefully can provide you a meal. But a gun used carelessly can be your worst nightmare.

Debt leverage is the same. It can be a great tool or your worst financial nightmare.

So, how do you treat leverage carefully? To start, make sure it’s positive leverage. This means your leverage is helping and not hurting your deal.

What Is Positive Leverage?

Positive leverage occurs when your investment property produces more income than the cost of your financing. Put another way, it looks like this:

Positive Leverage = Cap Rate > Financing Cost

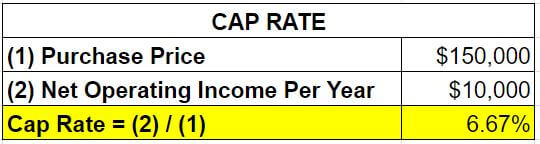

If you’re not familiar, I explain cap rates in this video. But a cap rate basically tells you how good a property is at producing rental income. It’s a return on investment calculation that assumes you have no debt.

For example, here is a chart that shows the cap rate for a rental property:

The financing cost in my analysis measures the total financing payment that comes out of your pocket. So, the financing cost includes both principal and interest payments.

Here is an example of how I use positive leverage for my Go, No-Go System.

Go, No-Go Example Using Positive Leverage

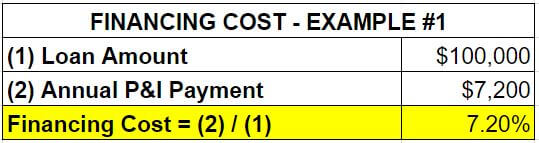

Let’s say you borrow a $100,000 loan at 6% with a 30-year amortization. Using my favorite amortization calculator, I find that the principal and interest payment is approximately $600/month. Therefore, the payment per year equals $7,200 ($600 x 12).

The financing cost is the ratio of your yearly principal & interest (P&I) payment and your total loan balance. Here is the calculation for this example:

Because the 6.67% cap rate is less than 7.20% (the financing cost), you have negative leverage.

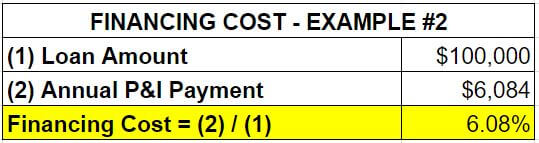

But if you got a 4.5% interest, 30-year loan instead, your payment would decrease to $507/month. The payment per year equals $6,084 ($507 x 12).

The financing cost for this 2nd example looks like this:

Because the 6.67% cap rate is more than the 6.08% financing costs, you have positive leverage.

Why Positive Leverage Is Important

Using debt is like renting money. The lender lets you use the money for a period of time and then you have to give it back. During the time you keep the money, you pay “rent” to the lender (i.e. interest).

With positive leverage, you’re making a profit on that rented money. Your return on investment increases because your debt contributes to the bottom line.

But with negative leverage, you’re making a loss on that rented money. Your return on investment decreases because your debt subtracts from the bottom line.

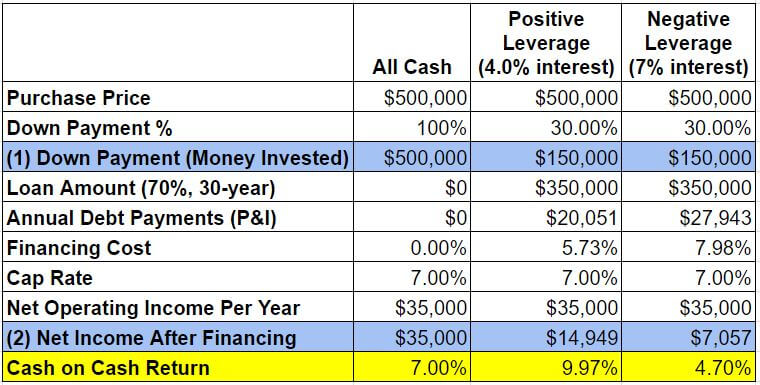

The chart below demonstrates how this works. It shows the same property being purchased with 3 different financing scenarios:

- No leverage (all cash)

- Positive leverage

- Negative leverage

With no leverage, the cash on cash return is 7%. Positive leverage increases the return to 9.97%. But negative leverage decreases the return to 4.70%.

The property is the exact same in all 3 scenarios. It cost the same and produces the same amount of rent. The only difference is the financing cost of the debt.

Obviously, you want positive leverage anytime you can. But as I said before, no rule applies 100% of the time.

In high priced markets, it may be difficult to find deals that produce positive leverage. So, if you choose to buy an investment property in these locations, you need to make sure you’re making money in some other way.

For example, some investors buy a property and count on it going up in value. But ask yourself if that potential appreciation return will compensate for the actual loss you experience because of negative leverage.

And if you buy a property with negative leverage, I would also make sure the other two Go, No-Go filters in this article are met. This way you minimize your risk as much as possible.

Go, No-Go #3: Balloon Payments

Balloon payments occur when your loan has a maturity date before it is completely amortized. For example, your loan could amortize over 30 years, but your lender could require you to pay the outstanding balance at the end of year 5. This would mean you need to come up with a HUGE amount of money either by refinancing, selling, or using your own cash.

I don’t like balloons. I’d prefer to have every loan fully amortize. Especially if you personally guarantee the loan, your home and your personal assets could be at risk if the balloon pops and you can’t pay it off.

But balloon payments are often the norm with commercial real estate loans. And for investors who don’t qualify for conventional, 30-year investment loans, this could be the only option you have.

So, if I do agree to a balloon, here are my Go, No-Go questions. I need to have a “yes” to one of these questions before I move forward to buy the property:

| 1. Is the loan balance low enough today that I could pay it off by selling at a wholesale price? (see Filter #1) |

| 2. Do I have enough cash reserves to pay the difference between the wholesale price and the loan balance? |

If the answer is no to both, it means I need to borrow less money and/or get a money partner who does have the cash reserves.

Early in my investing career, this filter led me and my business partner to bring in capital partners in order to cover our worst-case scenarios. The worst case never occurred, thankfully. We could say that we gave away profits needlessly, but it helped us sleep at night and invest with more confidence.

Zero Risk Investing?

In the world of entrepreneurship, there will always be some risk. Even with my Go, No-Go filters, I know I have made assumptions and taken risks that haven’t been addressed.

The key for me has been reducing enough risk so that I can sleep at night. Like me, you are bound to make mistakes and maybe even lose money at some point. But if you keep your mistakes small and if you proactively work to quickly correct them, you can still come out great in the end.

And that’s what I love about the game of real estate investing. No risk analysis is complete without the most important variable: YOU. Your energy, your enthusiasm, your creativity, your problem-solving ability, and your relationships all contribute towards solving problems and reducing risks.

So good luck with your next real estate purchase. I hope my Go, No-Go System helps you more confidently decide to buy or to pass on your next investment property.