Your Money Or Your Life, by Joe Dominguez & Vicki Robin

Your money or your life.

If someone thrust a gun in your ribs and said that sentence, what would you do? Most of us would turn over our wallets. The threat works because we value our lives more than we value money. Or do we?”

Joe Dominguez and Vicky Robin, Your Money or Your Life

Your Money or Your Life is one of those few books I read over and over because its ideas continue to challenge and inspire me. It’s a must-read for those interested in early retirement, financial independence, or improving their finances.

The book is officially about money. But in a deeper sense it’s about how to live your life. It’s about aligning your values and your daily decisions. It’s about swimming against the current of society in order to live a rich life on more than a just a material level.

The core premise of the book is that we trade too much of our lives for money. Most of our time, our identity, and our self-worth revolve around money or the things we do for money, like our jobs. If these truly made us happy, maybe that would be a fair trade. But in reality many of us are either miserable or dissatisfied with our careers and our financial lives.

So, if you feel like your existing patterns with money are not working, this book provides some interesting alternatives.

In this review I’ve narrowed down my favorite big ideas from the book. These ideas are are both extremely practical and deeply philosophical. If you really absorb and integrate them into your life, your relationship to money will change in a very positive way. And then when you’re asked whether you want your money or your life, you can happily answer “I want both!”

Stuck Making a Dying

How many people have you seen who are more alive at the end of the work day than they were at the beginning? Do we come home from our ‘making a living’ activity with more life? … Where’s all the life we supposedly made at work? … We are sacrificing our lives for money – but it’s happening so slowly that we barely notice.”

Joe Dominguez and Vicky Robin, Your Money or Your Life

Think of how much time most of us spend working. It’s not only the 40-60 hours per week while we’re officially on the clock. Work also includes the time commuting, getting ready each morning, decompressing each evening, attending post-work meetings, thinking about work at home, visiting the doctor for work or stress-related illnesses, and more.

As a percentage of our lives, work dominates like no other activity. If we’re lucky, we have work that challenges and rewards us in more ways than just a paycheck. But even then, work controls us instead of the other way around.

We work to pay the bills. We work to feel good about ourselves. We work to maintain our self-image. We work because we don’t know what else we’d do with our time.

There’s nothing wrong with work. It’s a noble pursuit. But are we really working to live? Or are we kicking the can until later in life when the time is finally right to start living (or when it’s too late)? The authors shared a story from who a lady who asked:

Is this all? Do I have to work and work and then retire – worn out – to be put out to pasture? To do nothing then but to try to spend money I saved up and to waste my time till my life is over?”

The main message of this book is that you don’t have to stay trapped in a life pattern you don’t like. Money is simultaneously the primary challenge and the primary solution. But, to solve this puzzle, you’ll have to undo some deeply ingrained habits and thought patterns.

The Myth of More is Better

If you live for having it all, what you have is never enough. In an environment of more is better, ‘enough’ is like the horizon, always receding. You lose the ability to identify that point of sufficiency at which you can choose to stop.”

Joe Dominguez and Vicky Robin, Your Money or Your Life

Do you know what financial myths you live by? A myth is not something untrue. It’s a story that you tell yourself below the surface of consciousness that affects your daily decisions.

It’s easy for us to see the myths of other people in other eras. For example, we study Greek myths in school. But our own myths? Those are much more difficult to identify. Yet, they determine most of our habits and our behaviors, for better or for worse.

One of the dominant modern economic myths is that more is better. This is a story we’re told long before we have a chance to question its truth.

If more is better, then the solution to most financial problems is to work more, to earn more money, to move up to a better job, to hire a better financial expert, and to get higher returns in the market. If we want to be happy, we should buy a nicer car, a bigger house, more food, more toys, and more expensive vacations.

This is not to say that any of those things are bad. But the satisfaction they produce is short-lived. It’s like a buzz from caffeine that wears off shortly after you drink a cup of coffee.

Unfortunately, the briefly satisfying more-more-more binges come with heavy, long-lasting financial chains, like a mortgage, a car loan, and credit card debt.

Psychologists call this phenomenon hedonic adaptation, which basically means you quickly revert back to your prior level of happiness after any life event – good or bad. Financially when you continually base decisions upon a more is better mindset, you get onto the hedonic treadmill, otherwise known as the rat race.

So, a big part of changing your relationship with money is to simply recognize the motivation and patterns behind your financial decisions. Plenty of outside forces are happy to make your decisions for you. Advertisers, for example, are happy to make you feel dissatisfied so that you’ll buy something new.

But once you become aware of the larger games being played, you can learn to ignore the noise and listen to your own direction. You can decide to replace the dominant myths of society with stories of your own choosing that actually serve your life.

This ode from poet Walt Whitman’s Song of the Open Road beautifully expresses the more unconventional path:

From this hour I ordain myself loos’d of limits and imaginary lines,

Going where I list, my own master total and absolute,

Listening to others, considering well what they say,

Pausing, searching, receiving, contemplating,

Gently, but with undeniable will divesting myself of the holds that would hold me.

Enough and the Fulfillment Curve

Part of the secret to life, it would seem, comes from identifying for yourself that point of maximum fulfillment. There is a name for this peak of the Fulfillment Curve, and it provides the basis for transforming your relationship with money. It’s a word we use every day, yet we are practically incapable of recognizing it when it’s staring us in the face. The word is “enough”.

Joe Dominguez and Vicky Robin, Your Money or Your Life

For me, this idea of “enough” was the gem of the book. It seems like common sense, but its application is anything but common.

You can look at your money and level of fulfillment in life as a graph. On the vertical axis is your level of fulfillment, and on the horizontal axis is the amount of money spent.

In the beginning of the Fulfillment Curve, each dollar spent creates an enormous jump in fulfillment. For example, paying for heat during a cold winter, a full meal when you’re hungry, or a home in a safe neighborhood for your family all bring significant spikes in fulfillment.

Eventually, as you spend more money, you reach the peak of the curve and that magical place called enough, which is very personal and unique for each person. But an interesting thing happens as you cross the peak of the curve and continue spending more. Your fulfillment flattens and then starts to drop. You’ve now reached the zone of over-consumption.

It’s as if the extra spending complicates and weighs down your happiness. A bigger house is nice, but it also requires a bigger mortgage payment, larger hazard insurance, nicer furnishings, more maintenance, a better security system, and a bigger job to pay for everything. The worry, stress, and pressure grow along with the amount of money spent.

The authors of the book describe the down slope of the curve as clutter.

Clutter is anything that is excess – for you. It’s whatever you have that doesn’t serve you, yet takes up space in your world. To let go of clutter, then, is not deprivation, it’s lightening up and opening up space for something new to happen.”

Way back in the 1800s one of my favorite writers and philosophers, Henry David Thoreau, was already experimenting in the art of decluttering and finding his unique version of enough. He wrote in Walden,

A man is rich in proportion to the number of things which he can afford to let alone.”

“Superfluous wealth can buy superfluities only… Money is not required to buy one necessity of the soul.”

And he also wrote about the people owned by their possessions, those deep on the down slope of the Fulfillment Curve:

I have in mind that seemingly wealthy, but most terribly impoverished class of all, who have accumulated dross [junk], but know not how to use it, or get rid of it, and thus have forged their own golden or silver fetters [shackles].”

[The bracketed comments are mine, because do you really know what “dross” or “fetters” are? I didn’t:)]

Enough is a very important concept. I can’t tell you exactly where it is for you. But if you’re honest, you can find it for yourself. And once you discover what enough is, you can begin to balance your spending on other important life possibilities, like freeing up your time with financial independence.

Money = Life Energy

Money is something we choose to trade our life energy for.”

“Our life energy is more real in our actual experience than money … So, while money has no intrinsic reality, our life energy does – at least to us. It’s tangible, and it’s finite. Life energy is all we have. It is precious because it is limited and irretrievable and because our choices about how we use it express the meaning and purpose of our time here on earth.”

Joe Dominguez and Vicky Robin, Your Money or Your Life

Have you ever thought about what money really is? You could read academic essays for days that describe nuanced definitions of the slippery concept of money.

But I’ve never found a more practical definition than this:

money = life energy.

This definition is useful because it helps you make conscious decisions about your work, your pay rate, your spending, and your investing. Instead of that dollar bill being just a piece of paper, it represents something you traded your time, your sweat, and your energy for. When you’re handing over your life, your priorities and method of handling money change!

This definition is also useful because it reminds us of what’s most important. In order to properly handle money, we have to think about our values and our life priorities. When you become clearer about what’s most important, money becomes just a useful tool that allows you to improve all of the other areas of your life.

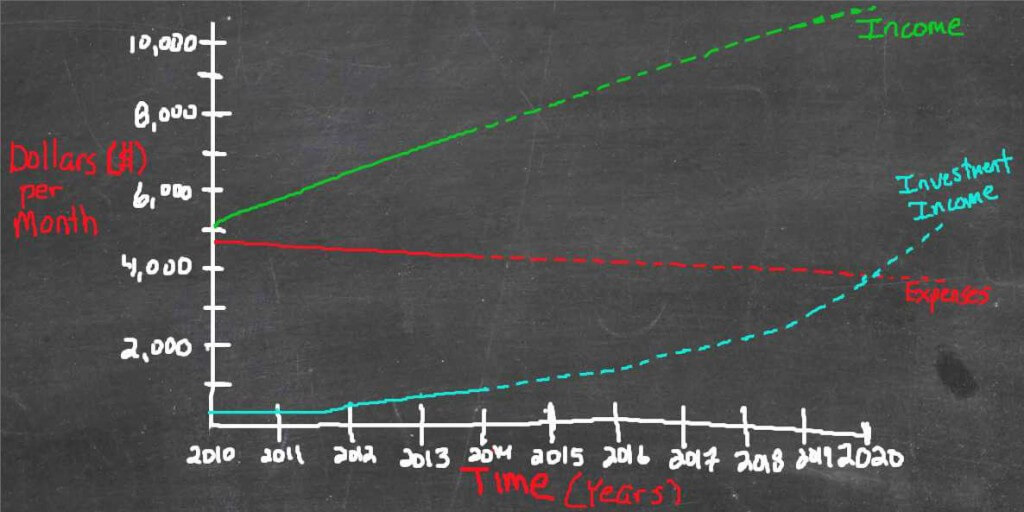

The Crossover Point to Financial Independence

The Crossover Point provides us with our final definition of Financial Independence. At the Crossover Point, where monthly investment income crosses over monthly expenses, you will be financially independent in the traditional sense of that term. You will have a safe, steady income for life from a source other than a job.”

Joe Dominguez and Vicky Robin, Your Money or Your Life

Ultimately, this book is about achieving financial independence. Practically speaking, the point where you can declare yourself financially independent is when your investments produce stable, consistent income sufficient to pay for all of your monthly living expenses.

You can create a chart like the one below. The point where the blue line (investment income) crosses the red line (expenses), is your crossover point. I share even more details about the crossover point and financial independence in a YouTube video I made.

The crossover point is a very exciting goal to make for yourself. Using a chart like the one above, you can plan and project the timing of your own crossover point based upon your income, savings rate, and your expenses. A free, online version of this chart can be found at an early retirement site I like called madfientist.com.

Keep in mind that making more money is a critical piece of the puzzle, but our savings rate (or the % of our income that we save) is the primary driver of a short (or a long) journey to financial independence.

It’s also worth noting that financial independence is not just about money in the bank or investment income. You could have millions of dollars and still not feel independent. Financial independence is also psychological, which is a big part of the message of this book.

Financial independence is an experience of freedom at a psychological level. You are free from the slavery to unconsciously held assumptions about money, and free of the guilt, resentment, envy, frustration, and despair you may have felt about money issues … Your emotional fortunes are no longer tied to your economic fortunes; your moods don’t swing with the Dow Jones Band. The broken record in your mind stops, the one that calculates hours till quitting time, days till payday, paydays till you have a down payment for a motorcycle, costs for the next home improvement project, and years till retirement. The silence, at first, is thundering.”

[bold letters added my me for emphasis]

I have a LONG way to go in the psychological realm of money. But I love the challenge! And I love the idea of freeing both my wallet and my mind from the chains that previously held them down.

Our lives are intertwined with our money in many ways. I hope you find the few ideas I’ve shared from this awesome book helpful. If the ideas resonated, be sure to get a copy for yourself.

Have you read this book? Did you enjoy it? What did you think of my favorite ideas? How does money play a role in your life (for better or for worse)? I’d love to hear from you in the comments section below.

Enthusiastically your Coach,

*all Amazon links are affiliate links where I earn a commission.