The Power of Compounding (Tax Free)

Albert Einstein supposedly said “compounding interest is the most powerful force in the universe.” It is doubtful Einstein really said that (Snopes and Quote Investigator), but it doesn’t take away from the importance of the message.

Compounding is a VERY powerful force that either works against you (borrowing) or for you (investing).

In our world of real estate investing, we can earn income from rentals or income from fix-and-flips and then reinvest that income to do more and more deals. That’s compounding at work.

But a big obstacle to really powerful compounding is income tax. It reduces our ability to compound growth of our investments by taking big chunks of our earnings along the way.

Probably the best legal way to solve this problem is to use self-directed retirement accounts to grow and compound our investments TAX FREE. Self-directed accounts allow you to invest your retirement funds in assets like real estate, tax liens, private notes, or land. A self-directed retirement account can be a traditional IRA, ROTH IRA, Solo 401k, HSA, and more.

To demonstrate my point I made a comparison between two hypothetical saving plans.

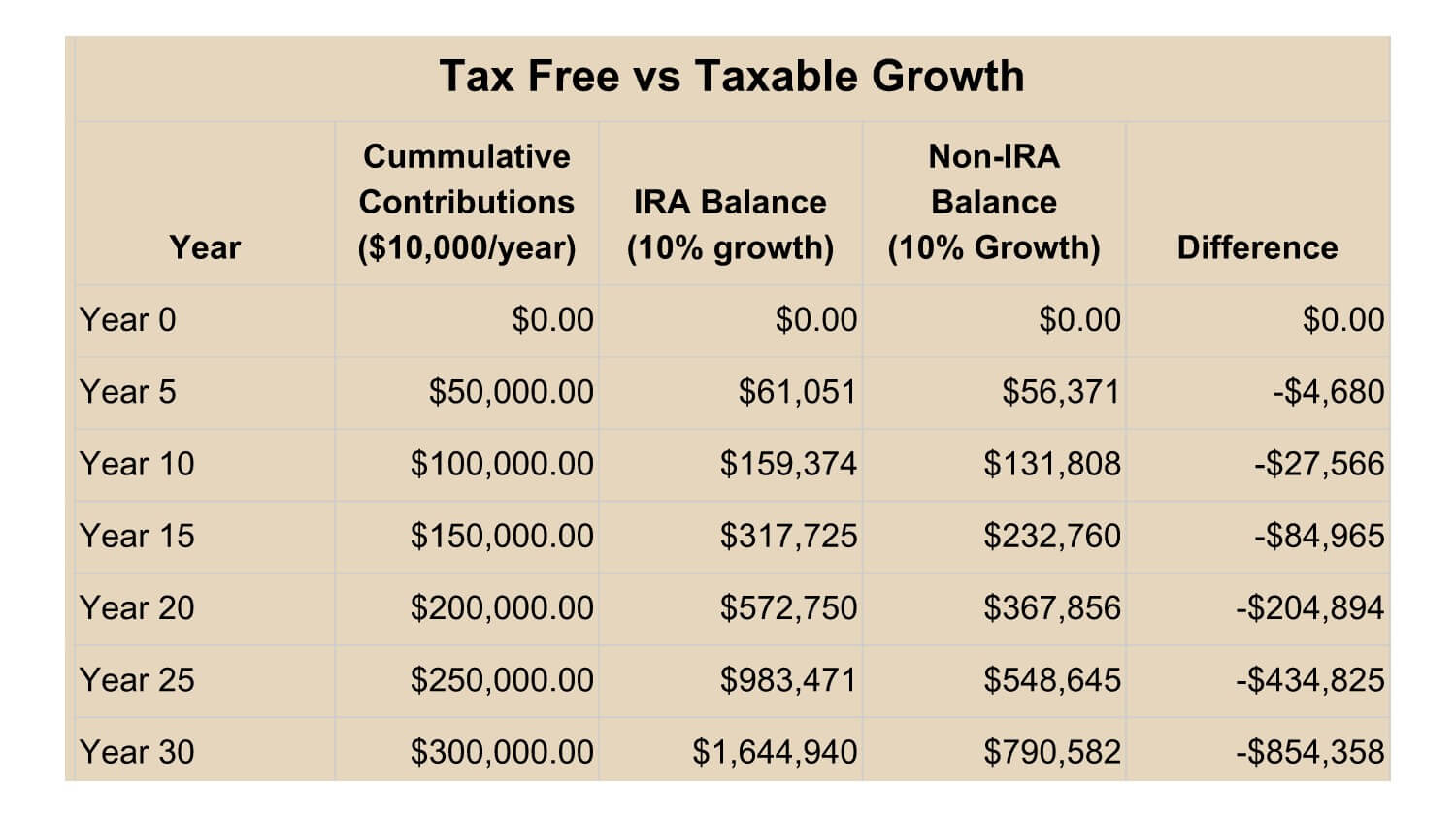

Plan #1 – IRA Balance – we save and then invest money at a 10% rate of return. All contributions and earnings would be kept in a tax-sheltered IRA account. So we would pay $0.00 in taxes, and all earnings would be reinvested (compounded).

Plan #2 – Non-IRA Balance – we would also save and then invest money at a 10% rate of return, but I assumed that all earnings would be taxed at an ordinary income tax rate of 40%. Therefore our NET earning was only 6%, and the compounding was less powerful.

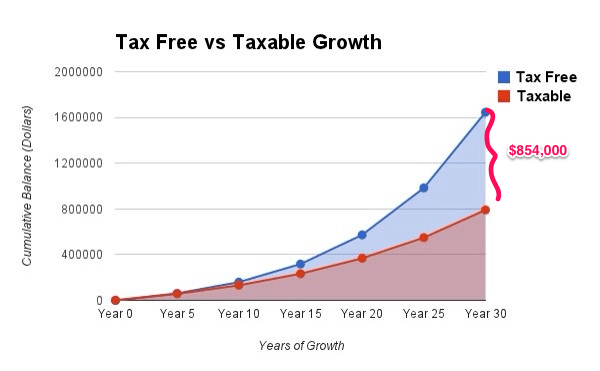

The difference in the final result is incredible. After 30 years the tax-free balance would have over 1.6 million dollars while the taxable account would only have 790,592 dollars.

That’s a difference of over $854,000!

To make that difference real, if the owner of each respective savings account retires and invests their entire year-30 balance into at a 6% yield, their incomes would look like this:

- Tax Free Account: $8,225/month or $98,700/year

- Taxable Account: $3,953/month or $47,436/year

The point of your investing is to eventually USE the money to fund your lifestyle, right? So, this difference is ENORMOUS.

As you can see, it pays to learn how to grow your investments tax-free.

I use my own self-directed IRA accounts for real estate related investments. So soon I’ll share some follow-up articles with my favorite real estate strategies for self-directed retirement accounts.

In the meantime, you can also get a free 1-1 consultation and an educational video about IRA investing from my friends at American IRA by visiting coachcarson.com/americanIRA.