Updated 9/25/2019

Watch YouTube Version

Listen to Podcast Version

House hacking is one of my favorite ways to get started in real estate investing. It is a method to live for free or almost for free by making a small multi-unit rental property your principal residence. In this way, your tenants basically help pay for your housing expenses.

The concept of house hacking is simple. But actually executing a house hack and maximizing your personal benefits can be a little more complicated. Finding the deal, getting a mortgage, saving the down payment, managing the tenants, dealing with taxes, and handling maintenance can seem overwhelming. But that’s why I created this guide!

Here is a summary of what you’ll learn below (click on a link to jump directly to that section):

- What Is House Hacking?

- Why House Hacking

- My First House Hack (including before/after pictures and real numbers)

- How to Run the Numbers on a House Hack

- Creative House Hacking Ideas

- How to Get a Mortgage & Raise Down Payment Funds For House Hacks

- Objections & Challenges

- 5 Steps to Buy Your First House Hacking Property

Let’s dive in!

What is House Hacking?

House hacking is when you buy a small multi-unit real estate property, live in one unit, and rent out the others. The property for house hacking could be a duplex, a triplex, a fourplex, a single family house, or even other creative property uses like garage apartments or mobile homes, which I’ll cover later. The income from the rental units can pay for some or all or expenses while you live there. Then once you move out, the property could also become a great long-term rental investment.

As a real estate investor for over 17 years, I’ve personally benefited from house hacks. I lived for free in a small multi-unit property for several years before moving out and keeping it as a rental (more on that later). I’ve also helped others get started with house hacking.

House hacking is the ideal housing choice for young homeowners who are willing to take the extra effort to learn how. If you start with house hacking as a young adult instead of the normal housing options (renting or buying a house), you can build much more wealth over the years. This is because of a concept called “opportunity cost,” which I explained in How to Retire Rich With Embarrassing Old Cars and Ugly Houses. Housing is one of the biggest expenses of every budget, so if you can cut that expense, save the money, and invest it wisely, you’re giving yourself a HUGE head-start towards becoming wealthy and even retiring early.

Now let’s take a look at more benefits of house hacking.

Why House Hacking

I’ve already mentioned the first big benefit of house hacking. It can reduce or eliminate your housing costs, which are a major part of most personal budgets.

A U.S. Bureau of Labor Statistics report for 2015 shows that 19.2% of the average U.S. household’s expenses were dedicated to shelter. The actual number was $10,742 per year or $895 per month on average. Canadian households’ average shelter expenses were even higher at 28.9% of household expenses. The actual shelter expense in Canada was $17,509 per year or $1,459 per month. Of course, these expenses will be much higher than these quoted figures in some locations, which makes house hacking even more important.

But there are other benefits to house hacking. Here are just a few:

- Occupants get the best financing terms – Owner occupant financing has lower interest rates and more attractive terms than investment financing. If you keep the property as a long-term rental, this is a huge benefit because you can keep the owner-occupied loan in place even after moving out.

- Smaller down payments are possible – As you’ll see in the section on financing your house hack, smaller down payments of 0% to 5% are possible with programs like VA and FHA loans. Typical investment loans require 20-25% down.

- Learn how to invest in real estate – House hacking is a hybrid of a residence and an investment. You live in the property while learning to invest. Everyone makes mistakes while learning, but it’s easier to recover when you’re on site and personally involved.

- Smooth transition to rental properties – When you live in a property, you get to know it well. You also get to know the type of tenants your property attracts. So, once you move out you will have an increased comfort level with the property and your tenants as a landlord. With your low-interest loan, you’ll likely also make the best possible cash flow from the property once it’s fully rented.

Now that you understand some of the benefits, let’s look at the example of my own first house hack.

My First House Hack – Merry Christmas to You

Early in my 20s as a recent college grad, I was living cheap and flipping houses. I actually lived in the spare bedroom of my friend and business partner’s house. My bed was in the corner surrounded by storage boxes! It was inexpensive housing, but I wanted a place of my own. And because I enjoyed paying little to nothing for housing, a house hack was a perfect next choice.

A friend told me about a vacant, foreclosed fourplex building in my small college town that needed A LOT of fixing up. I can just imagine the foreclosing banker showing up with a nice car and fancy shoes to see “Merry Christmas” spray painted across the front! Ha! I doubt he even made it out of his car.

Here’s how bad it looked inside before I bought it.

Before you think all house hacks are this nasty, keep in mind that this was ultra ugly. My motto in real estate is the uglier the better (because you get it cheaper). And this was clearly the worst property in a decent neighborhood close to the campus of Clemson University.

But there are many house hack opportunities without this much work. The choice is yours. And don’t worry. I didn’t move into that nastiness. We fixed it up, and pretty soon it was a warm, cozy home.

My Beautiful Little Fourplex After Some Love

After a few months and some help from repair contractors, my house hacking home was ready. I moved into unit #2, and I rented the other 3 units out to tenants who loved the upgrades.

The upgrades included four new central heat and air units, replacement windows, exterior paint, landscaping, a community garden, dishwashers, paint, new lighting/fans, back decks, and new floor coverings. Here are a few of the pictures after repairs were finished (you’ll notice that my girlfriend at the time, now my wife, loved bright colors).

Turning the building around was a lot of fun. And I also enjoyed living there. In fact, I liked it so much that this was the first home that my wife and I shared for several years after getting married.

But while the feel-good story is important, you and I both also care about the numbers. So, let’s look at the bottom line.

The Final Numbers for My House Hack

I bought the fourplex at a good price ($70,000) using a combination of a local bank loan and private financing. I then spent about $45,000 (yes, I told you it was nasty) rehabbing and upgrading the property.

Once I had 3 of the 4 units rented out, I moved into the 4th unit, lived there for 6 months, and applied for a refinance. Because the value was now much higher (about $155,000), I was able to borrow $120,000 and pull out 100% of my invested money. This particular strategy is known in online real estate circles as the BRRRR Strategy (Buy, Rehab, Rent, Refinance, Repeat). But I’ll talk about that more in the financing section of this guide.

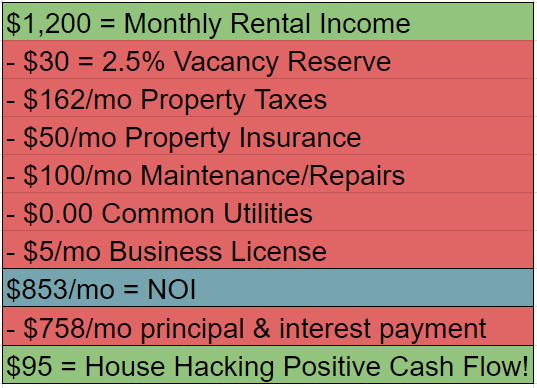

For now, let me show you the cash flow numbers after my fourplex was remodeled, occupied, and refinanced with a $120,000, 6.5%, 30-year mortgage.

I was basically getting PAID to live in my new home! Beautiful! And because of the refinance, I had no cash out of my pocket.

Not all deals are this good. I’ll admit this was a stand-up triple, to use a baseball analogy. But even if your house hack reduced your payment from $1,200 to $600 per month, would that not be a win? I think so. But you’ll have to decide for yourself what a good deal means.

To help you do that, let’s continue by figuring out the basic calculations of house hacking cash flow.

The Basics of Running House Hack Numbers

As you can see from my real life example, one of the primary goals will be to reduce or eliminate your housing payment. Fourplexes typically have the best numbers because they have 3 tenants that help to pay the bills. But other properties like duplexes and triplexes can do well too.

In addition to your monthly cash flow numbers, you’ll also want to pay attention to the price you pay. While it’s not always necessary to get a deal far below value for it to make sense (although that’s always better!), you also don’t want to overpay if you can help it.

A knowledgeable local real estate agent can help you estimate the value. You can also learn to estimate values yourself (a skill I recommend).

But here I’ll show you here how to do a few basic calculations that will help you understand your cash flow numbers before purchasing.

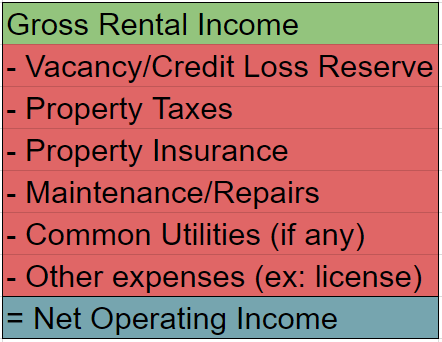

Net Operating Income (NOI)

The Net Operating Income, known also as NOI, tells you the amount of money your rental property will produce before paying your mortgage and before income taxes. Why is this number important for house hacks? Because it tells you how much of your mortgage payment will be covered by rent each month.

Here is the formula:

and here is an example:

I would recommend that you calculate the NOI when you first find a property and again with the help of your agent or other investors during the due diligence phase before purchasing the building. Calculating the NOI early is helpful because then you can then run a second calculation – your mortgage payment.

Calculating Your Mortgage Payment

This is a step you don’t have to do on your own. Your banker or mortgage broker can easily help you. But if you’re reading this article, you’re an empowered, DYI type who likes to understand it for yourself (that’s me too!). So, let’s see how simple it is to calculate a mortgage payment on your own.

- Estimate the purchase price of the property

- Estimate the down payment

- Subtract the down payment from the purchase price to get your loan amount (aka principal)

- Go to this online mortgage calculator (my favorite online calculator for years).

- Enter the loan amount (principal), interest rate, and the number of payments (leave at 360). Leave the fields for the payment amount and balloon payment blank, and leave payments per year at 12.

- Click “calculate.”

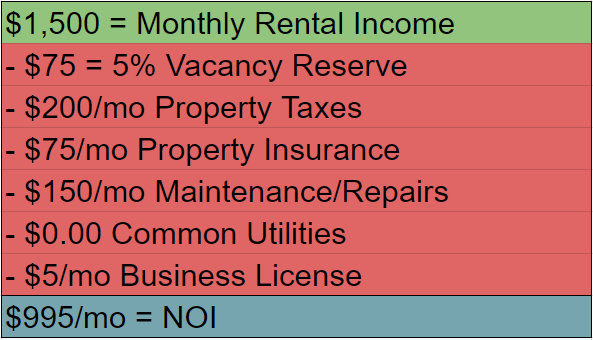

The mortgage calculator will tell you the monthly payment amount. If you want to practice, use the numbers below and enter them in the calculator to figure out your payment. Don’t skip ahead yet. I’ll show you the answer right after.

- Loan principal = $175,000

- Interest rate = 5.1%

- Term = 30 years (360 months)

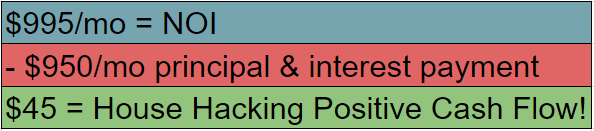

Now compare this number to the NOI calculation above. Are we living for free or not?

To find out, you use the mortgage payment you calculated above (the answer is ~ $950 per month). So, your house hacking monthly cash flow looks like this:

Living free! You’re welcome to do a happy dance now! I don’t know about you, but it’s a wonderful reality when your tenants are paying for your housing expenses.

Creative House Hacking Ideas

As you saw in my house hacking example, a fourplex can be a great property to buy for a house hack. But it’s not the only type. And it’s probably not the most common because there are fewer fourplexes than other property types. So, here are some other property types you can use for house hacking.

- Duplexes (VERY common)

- Triplexes

- Spare bedrooms of a single family house (rent to roommates or to Airbnb guests)

- Accessory Dwelling Units of a single family house (ex: basement apartment, garage apartment, or small, on-site cottage)

- Mobile home or RV rentals on a large lot of a single family house

- Rent parking spaces in your driveway (pavemint.com, justpark.com & see this article)

I’ll add a disclaimer that not every strategy will work in every location. For example, I don’t see the zoning codes of suburban neighborhoods allowing mobile homes in the backyard! So, do your homework with your local municipality before counting on the extra income.

But the point is that you should think creatively. If you want to house hack and reduce your house payment, seek out opportunities. This is a form of entrepreneurship, so get excited and go hunt for an opportunity in your location.

How to Get a Mortgage & Raise Down Payment Funds

A critical part house hacking is obtaining a good mortgage. My definition of a good mortgage includes the following:

- Interest rate is as low as possible and fixed long-term (can not adjust)

- Monthly payment is as low as possible (30-year loans are preferred)

- Small down payment

- No “gotchas” – like short-term balloon payments or prepayment penalties

You can accomplish most of these goals with traditional owner-occupied mortgage products (especially in the US). But of many mortgage options, three US-based lending programs stand out because they allow you to buy the property with a lower down payment. I’ll explain those briefly here.

1. FHA Loans (Federal Housing Administration)

- What is it? A federally insured loan program targeted to owner-occupant buyers who have less cash available and/or a lower credit score

- Pluses: Less restrictive qualifying requirements for borrowers (vs conventional loans), only 3.5% down payment, fixed interest rate for 30 years, 1 to 4 unit properties eligible

- Negatives: Higher fees (including an up-front mortgage insurance fee), slower approval process, major remodels not allowed (except 203k program, see below)

- Where to find it: FHA approved lenders can be found at most bank mortgage departments, mortgage brokers, credit unions, or mortgage lenders.

Further reading: Check out this Wikipedia article to learn more details about this program.

**Update** A comment from guyonfire.us reminded me about something called the FHA 203k home renovation loan. This loan product is pefect for house hacks. Both the streamline and the regular 203k loan give you the ability to borrow money for repairs. For more details see the Department of HUD 203k loan details.

2. VA Loans (Veterans Administration)

- What is it? A federally insured loan program especially for veterans of the US military.

- Pluses: No down payment ($0.00), fixed interest rate for 30 years, reasonable qualification requirements, multiple loans possible, 1 to 4 unit properties eligible

- Negatives: Paperwork and approval process isn’t super-fast, limits on the number of loans based on your “entitlement” ceiling, major fixer-upper properties won’t qualify

- Where to find it: VA approved lenders can be found at most bank mortgage departments, mortgage brokers, credit unions, or mortgage lenders.

Further reading: For more details on VA loans and using them to buy investment properties, read my friend Rich’s Investing With VA Loans – A Complete Guide.

3. Conventional Conforming Loans

- What is it? Conventional loans are loans not guaranteed by the government (whereas FHA and VA are guaranteed by the government). Conforming loans are a type of conventional loan that conforms to the underwriting criteria of Fannie Mae and Freddie Mac (two mortgage company giants). Conforming loans benefit house hackers by providing great terms, low interest rates, and flexible down payments (3% to 20% for owner occupied housing).

- Pluses: 15 and 30-year fixed interest rates and payments, faster qualifying than FHA and VA loans, 1 to 4 unit properties eligible

- Negatives: You’ll max out around 4 to 10 approved loans. Credit requirements are typically more stringent than FHA or VA.

- Where to find it: Lenders who make conforming loans can be found at most bank mortgage departments, mortgage brokers, credit unions, or mortgage lenders.

Further reading: Read this BiggerPockets article to learn more about qualifying for a conforming loan. Also, check out the Eligibility Matrix (8/2019 version) put out by Fannie Mae to describe their requirements for borrowers.

**Update** Patsy Waldron pointed out in the comments that the FannieMae Homestyle renovation loan program is also a great option for House Hacks. Like the FHA 203k loans, Homestyle loans can be used to purchase and renovate a 1 to 4 unit home as long as you occupy it. It can also be used for single family home investment projects even if you don’t occupy it. For more details see the Homestyle Renovation Matrix from FannieMae.

Using the BRRRR (Buy, Rehab, Rent, Refinance, Repeat) Financing Technique

You might have noticed that in the three financing programs I just described, major fixer-upper properties are not allowed (update – except for the FHA 203k loan program). So, if you are buying a typical property that just needs cosmetic upgrades, like paint and carpet, you’ll be fine.

But do you remember my personal house hack? It was in rough shape. So, how did I finance it?

I used a strategy that is often called the BRRRR technique. It’s actually been a popular strategy among real estate investors for a long time, but my friend and Bigger Pockets Podcast co-host Brandon Turner kindly gave it the catchy name. You can read Brandon’s original BRRRR post on Bigger Pockets here.

How does the BRRRR technique work? Here are the basics.

- Buy a property using short-term funds (cash, a line of credit, construction loan, hard money loan, private money, etc).

- Rehab the property to get it pretty and rentable

- Rent the property

- Season the rental (this is often 6 months)

- Refinance the property with a long-term mortgage (see the options I described above)

In an ideal world, your remodel will increase the value of the property. This is not a given, however, so carefully analyze the market and your purchase price with the help of a professional before you buy it. You can then refinance the property to pull out most or even ALL of your money out of the property. This is a happy day!

Little or no money down investing may sound like a gimmick. But in this case, it’s not. And when you combine this small amount of cash invested with the other benefits of house hacking, like reducing or eliminating your housing payments, you can see why it’s easily one of the best overall real estate investing strategies!

Objections and Challenges

I’ve been a house hacking evangelist for a long time. Many people get it right away and run as fast as they can to get started, but I also hear my share of objections. Here are some of the most common objections I hear plus my responses.

“I don’t want to live next to my tenants.”

The landlord-tenant relationship has bad stereotypes. Plenty of bad landlords and bad tenants have earned this reputation, of course. For this reason, you might be hesitant to live next to your tenants.

But keep in mind, you get to choose your tenants. You can’t and shouldn’t discriminate based on race, religion, color, gender, familial status, or other legally protected classes. But you can and should use a thorough tenant screening process to find only the best tenants.

And yes, there will be occasional texts, calls, or knocks at your door with maintenance issues. But you don’t have to do these yourself if you don’t want to. From the beginning, I’ve been very good at programming the name and number of contractors in my phone. I call them, they handle these problems, and I write them a check.

And I actually enjoyed getting to know my next-door tenants. I got to know wonderful, interesting people because the were my neighbors in a house hack. My life is richer for that experience.

“I Don’t Know How to Be a Landlord.”

We all have to learn to walk before we can run. And house hacking is the perfect way to learn to be a landlord. You’re bound to make mistakes, just like I did. But because you are living on-site, you can make up for your lack of knowledge with hustle, sincerity, and your own sweat.

Plus, you’re subscribed to the coachcarson.com newsletter for a reason! You’re a learner! Just like you learned to do everything else in life, you can learn to be a landlord. You’re welcome to search the archives for techniques and strategies. You can also leave comments and questions for me.

And if I can’t help you, there are many wonderful landlording resources and books that will bring you up to speed. Some of my favorites include:

- Landlording 101 (or How I Managed 90+ Properties From Another Country)

- The Book on Managing Rental Properties, by Brandon and Heather Turner

- Landlording on Autopilot, by Mike Butler

“I don’t think I can find a good deal?” [or] “There are no good deals in MY town.”

In the final section of this article, I will give you some action steps and resources to help find your first deal. But finding a good deal really is one of the most important and challenging parts of the process. But like any other puzzle, it can be solved.

Finding real estate deals is a lot like a treasure hunt. First, you need to know what you’re looking for. Second, you need to turn over a LOT of stones looking for a gem. If you don’t have the time to invest up front to find a good deal, house hacking might be something to put off for now.

And I’m very aware that different markets have different pricing and investment fundamentals. For those of you in California, Canada, Great Britain, or many other places around the world, the numbers of my personal house hack seem unreal.

You may or may not be able to find the perfect numbers in your market. But the principle of house hacks remains true – you can use the rent from your tenants to REDUCE your housing payment and save money. So whether you completely live for free or just save a lot of money, the concept is still beneficial.

Now, let’s finish by looking at how to find your first house hack property.

5 Steps to Buy Your First House Hacking Property

I’ve given you a lot of information about house hacking. But this guide will not be a success unless you take this information and apply it to your life. That’s what I want to help you with now.

Here are 5 steps that I think will get you moving in the right direction.

Step #1 – Commit yourself to the concept

If you’ve made it this far, I assume you like the concept of house hacking. Now, it’s time to commit. If you have a partner or spouse, discuss this with them. Listen to their objections, if any. And decide if house hacking is a good fit for your life.

If house hacking isn’t right for you, that’s fine. There are plenty of other real estate strategies and real estate niches that you can work on.

But if it is the right strategy for you, commit yourself to making it happen. You’ll need the energy of that commitment to stick through until the end.

Step #2 – Prepare Your Financing

I often compare purchasing real estate investments to bird hunting (I can’t help it, I grew up in the country). If you go hunting for birds without loading your gun with ammunition, you’re wasting your time and you’ll go to sleep hungry that night.

Real estate financing is the ammunition of your hunting for good deals. It’s smart to get your financing in order FIRST. Review the information I provided about house hacking financing. Then contact your preferred mortgage banker, private lender, or another source of money and get preapproved.

Once you have that preapproval, you can begin hunting for deals.

Step #3 – Study Your Market

While you are preparing your financing, you can also begin studying your market to increase your chances of finding a good house hacking property. If you’re an experienced real estate agent, you can probably do this on your own. For everyone else, I recommend that you hire an expert who not only knows the market but also understands investment properties.

What are you looking for with your market study? Begin by choosing the right target market. I made a written guide explaining this process. You want to focus in on a location that has solid fundamentals, like population growth, good jobs, and attractive amenities.

Then ask your real estate agent to show you the small, multi-unit properties available for sale in your target market. Figure out the current and the market rents for these properties. Run the net operating income and mortgage payment calculations I showed you before.

If the numbers for the listed properties seem good, that is wonderful. But the numbers might not be as good as you like. So, you may need to adjust your target market or adjust your goals to fit the reality on the ground.

Step #4 – Create a Deal-Finding Plan

Now it’s time to start hunting. But you can’t expect good deals to fall in your lap. You have to be proactive.

Most house hackers begin with the MLS (Multiple Listing Service). This is the database of properties for sale that only real estate agents can access. Your agent can search all of the current properties that meet your criteria. She or he can also set-up a filter search that alerts you anytime a new property that meets your criteria comes on the market.

The key to MLS success is jumping on deals quickly. If it’s a good deal, it won’t last long. That is why I had you prepare your financing and market study first.

While the MLS is a good place to start, it’s also the most competitive. I like other channels to find deals, like:

- Walking or Driving Neighborhoods (aka Driving For Dollars) – Get on the side streets, look for interesting properties, call for sale or for rent signs, talk to neighbors, leave your card or phone number, and just follow your nose. Few people will do this, and for that reason, it’s always been my favorite strategy to find deals.

- Write Letters – Some of my best deals have come from a simple letter. If I find an interesting property, either while driving for dollars or searching online, I’ll look up the owner and send them a letter. Keep in mind these are not properties listed for sale. These letters come to the owner out of the blue. Your letter might remind them that they wanted to sell!

- Word of Mouth – Don’t discount good, old-fashioned word of mouth. Tell everyone you know the type of property and the locations you’re hunting for. Instead of one set of eyes, you’ll now have many looking for you.

These ideas should get you started, but you can also study my process and how I found 33 deals in one year.

Step 5 – Take Action

None of this will work unless you take action. And I recommend getting out from behind your computer and out into the neighborhoods where the action actually happens. If you can’t do it personally, hire an agent to do it for you.

Successfully executing any plan, including purchase a property for house hacking, means you have to carefully budget your time. I see more dreams come to a screeching halt because of poor time management than any other reason. People get too busy and their momentum stops.

Prepare for this challenge ahead of time. Carve out time in your schedule. Write down “appointments” in your calendar to work on this just like you would a doctor’s appointment. Then don’t miss it!

If you need help with this step, I have written a lot about time management. If you begin with one strategy, I would suggest figuring out how to distinguish between the Urgent and the Important. Then prioritize your life accordingly.

Is House Hacking For You?

I hope this guide has been helpful. I’ve given you over 4,500 words of advice about house hacking. Now the ball is in your court!

If this article helps you to do your own house hack, please let me know. I’d love to celebrate your success!

Is house hacking right for you? If so, what are your next steps? What challenges do you see with your own house hacking plan? I’d love to hear from you in the comments below.

Get My Free Real Estate Investing Toolkit!

Enter your email address and click "Get Toolkit"

Again, perfect timing. Are you stalking me? Because this is getting weird and I love it.

I’m in the process of buying a triplex and depending on the utilities, I’ll be able to live completely for free or pay less than $100. Sounds like a pretty great deal to me!

What do you do for insurance? I got a quote and they want to charge me for a rental insurance policy since I have other people living in the house. Then I get to pay renter’s insurance on top of that to protect my belongings. It’s so dumb.

Ha, Ha. Yes, I just post whatever is going on with your blog. Makes it easier that way:)

That’s so awesome about your own house hacking story. Living for free is the way to go!

For insurance yes I got a landlord policy and then personal property policy on top of that (although my personal property was pretty cheap – lol). The only good part about the landlord policy is additional liability policy. Usually $500,000 – $1,000,000 is fairly cheap. Just shop around as much as possible.

Great article. One critique, you should add a piece about an FHA 203K loans. These are PERFECT for fixer uppers and allow people to utIlize leverage on 1-4unit properties.

Keep up the great work.

Great point about FHA 203k loans, Guy on Fire. Thank you. I have updated the article, linked to a good reference about the program, and gave you the credit with a link to your site!

Thanks for all the great ideas! And extra thanks for considering the Canadian side of things! Yes we look jealously at some south-of-the-border prices, but like you said, finding deals is like a treasure hunt. With persistence and proactiveness (is this a word lol?!), there are deals to be found in our crazy Vancouver, British Columbia market. I will be forwarding this article to my university-aged kids and hopefully some of your ideas will catch their attention!

Proactivity is a word in my dictionary! Thank you for reading, commenting, and sharing.

I think the key is absorb the principle, and then figure out a way to creatively apply it in your market. Plenty of people will say “that is impossible here” but here are walks a few who quietly figure it out and just do it anyway. Good luck!

That is an incredible story of your first house hack. I wish I did this in 2010 when Bay Area properties were so cheap and I was living with roommates anyway. Would have had to give up some in terms of location, but financially it would have been a homerun.

Yeah, that is why I am trying to get the word out to others now! Missed opportunities. I have a friend with a duplex he originally house hacked in Berkeley, California. It has just gone up and up since he bought it. It is about the only way to get into some neighborhood there, right?

Doooood this is legit! Thanks for the mention also!

Happy to share, Brandon! Thanks for reading and commenting.

Great article with some very useful details! My husband and I are considering a house-hack in our new city. We owned a very nice house that I loved (and miss!) but learned that a house is definitely a BIG expense! Now that we have moved to a new state, we can use house-hacking to reduce our housing expense. I have already identified a very good candidate- a side-by-side duplex in a pretty nice area of town, the right size for us and with ALL separate utilities! If we get it at the price we want (it is waaaay overpriced right now), the rent from one side will cover PIT but insurance will come out of our pocket. That makes up for not having to pay water/sewer for the tenants, in my eyes, so we will essentially break even before factoring in vacancy and maintenance. Now to convince the obstinate old owner to agree to ~20K less than what he thinks he should get. 🙂

By the way, Fannie Mae also offers a renovation loan, which can actually be used either by owner-occupants OR investors- it’s the HomeStyle loan. I don’t really like FHA’s 3.5% down loan because it now carries mortgage insurance premium for the life of the loan (PMI no longer falls off after you’ve reached 20% equity). Fannie Mae is superior in that respect, I think.

Thanks for reading and for sharing your story, Patsy! Good luck with the negotiation. Sometimes it’s a matter of patience and persistence. And other times it’s about moving to the next one if the numbers don’t work.

Thanks for sharing the Fannie Mae Homestyle renovation loan details. I’ll update the article to include.

But one thing I noticed from the FannieMae documentation (see link I added in article) is that the loan-to-value for a purchase of a duplex is 85%. So you’d just need to make sure you had the down payment needed. FHA’s down payment is a little lower.

Quite thorough, coach! What a great way to keep your expenses low while building equity.

I recall your contemporary Matt Birk living this way in his early days as a Minnesota Viking. As an economics major at Harvard, he knew how to hack his housing.

Cheers!

-PoF

Thanks PonF. Perhaps some of your ambitious readers in residency or early years of their career could adopt you this one. They work all the time and only need a bed anyway, right?

And that is interesting about Matt Birk! I did not know that. Thanks for sharing. Unfortunately not all intelligent professionals or economics majors make wise money choices, as you know of course!

I tried to find a link about Birk at one point recently, but didn’t find it. It was well documented on local news & radio at the time.

I’m doing my part to educate the high-income professionals who didn’t get their economics degree from Harvard. It’s an uphill battle, but we’re making strides.

Cheers!

Very thorough analysis for those that may want to dip their hands into real estate investing. I alternate on whether I want to become a landlord. Frankly I’m probably too busy with kids and other stages of my life to go there at the moment, so instead I’m testing out other avenues for real estate exposure. Honestly there is only one step in your analysis that would concern me, and its tied to my risk tolerance. Refinancing to take out all of your equity would make me nervous. We just left 2008 where people lost their shirts losing that approach. In small amounts, like a single structure it’s probably fine. But you can create a house of cards if your not careful.

Thanks for the comment! I agree that risk tolerance is something to consider with this strategy or really any leveraged real estate strategy. I personally encourage people to pick their starting strategy, but then move towards a portfolio of free and clear properties.

But I think it is also important to distinguish between the wide sprectrum of real estate risk. “Pulling out equity” can be risky in principle, but it is usually the case because the financing and the cash flow both get worse. In my example, my financing actually became less risky (short term private loan converted to longer term, fixed loan). And my cash flow improved (higher interest rate, higher payment converted to lower rate, lower payment). In 2008 the people who lost their shirts, both individual investors and big corporation, had risky financing (balloon payments) with poor debt coverage. Investors with positive cash flow and low risk financing did fine because rents were fairly stable.

But Of course there is always the possibility next time will be different. What if rents crater by 50%? That is why free and clear properties are a good long term plan for at least part of your portfolio.

Yes! I love this! When Mr. Beach Life and I were looking to purchase a home we started with duplexes and triplexes. Because of the laws in our town the only multifamily properties near downtown and the college were grandfathered in, so there weren’t many to choose from and they sold quick. We adjusted our plan and bought a single family house in a great neighborhood but one with a walk out basement and private entrance. We renovated it into a suite (basically an efficiency apartment without an oven. City rules state that once a second oven has been added it changes the property from single family to multifamily) and now rent it on Airbnb. We’ve been doing it since November 2015 and haven’t had to pay our mortgage or property taxes from our paychecks ever since.

I know that being a landlord can be work (I own an out of state rental property) but I am shocked at how many people instantly nix the idea of buying a multifamily property to live in and rent out.

I love your creativity! Thanks for sharing.

There are so many ways to make House Hacking work. I am also shocked (and motivated!) that more people don’t do this. Thus the guide! Thanks for helping me to spread the word. I would love to see many more starter homes built to accommodate House Hacking in the future. Wouldn’t it be great if more people did this instead of buying McMansions?

I might be missing something…but how long of an investment is this? About to start my first steady job, moving in from out of state and I don’t want to waste time renting. I would love to buy a triplex or something similar but not if I have to live in it for 30 years!

Good question, Carla! In terms of living there most people stay a minimum of 1-2 years as a residence. You can of course stay longer, but often people choose to move and rent it out after that. From there, you can keep it as long as it make sense within your overall real estate strategy.

2 years minimum is how long you need to live there

CJ, can you tell me where you got that 2 years as a minimum? For a different strategy where you’re flipping the house and want to avoid capital gains tax 2 years is certainly the minimum. But I’m not aware of any other rules that would require 2 years on a house hack.

Great content, Coach! Thank you for your insight. I am leaving for the service at the end of this year/ beginning of next year but I would really like to get at least one property under my belt before I leave. Do you think this is an attainable goal or do you think I would need to be living in the property for longer to make it work?

Hi Tyler,

Sorry I didn’t catch this comment earlier. Thanks for reading and asking a question.

It’s hard to say on the timeline. You would be pushing it a bit if you’re starting from scratch. But perhaps you could do a trial run and worst case you learn your market and practice the run-up to buying a property.

Will you have anyone at home when you leave for the service? If so, that would of course make it simpler. If not, you’d want to have a trusted person to help while you’re gone and/or a ;property manager for the other units that aren’t your residence.

Awesome article, I actually had a lot of fun reading. I am graduating in December of this year and my boyfriend and I are thinking of house hacking, BUT we don’t have any money lol.

Thanks for reading, Isa! I didn’t have a lot of money when I started either. It’s a little harder, but you just have to get creative with the financing (partners, private lenders, etc). Best of luck!

Thank you a lot for sharing this with all of us you really understand what

you’re speaking approximately! Bookmarked. Please also talk over with my website =).

We could have a link alternate arrangement between us

Do you advise against buying during an inflated real estate period? (Right now)

I am still buying:) So, that’s my best answer. But I’m buying with two things in mind: (1) I need to be able to sell it quickly for above what I paid for it (i.e. buy it below value) OR (2) I need to be willing to hold it long-term (10-12 years) and it still be a good deal. Speculating on that in between – like the next 1 – 5 years – is more difficult in my book. So, the main point is it just needs to be a good deal in one or both of those holding periods (very short, very long).

This article was super informative and the knowledge was very helpful. Thank you mate!

Thanks for a great article, Chad!

I am just completing my first house hack this year. It’s a SFR and I have been living for roughly $300/mo including my share of the mortgage and utilities. I’m under contract on my second as we speak and I’ll get better financing on it so hopefully I cash flow a bit while living there!

Someone mentioned needing to live in it for 2 years, and that is actually incorrect. When you sign the mortgage agreement, you are agreeing that you have the intent to live in the property as your primary residence for 12 months. Some special circumstances can even shorten that requirement.

The whole concept of the 2 years comes into play when you need to avoid capital gains tax such as live-in house flipping. But with house hacking, you can purchase a new long-term buy and hold property once per year.

Nice job on those house hacks, Kevin! Thanks for sharing.

And good point on the length of time. Some people confuse the IRS rule for capital gains tax exemption (2 out of 5 years) with the requirement in your mortgage to live there (12 months or so, as you stated).

I am a beginner and have found a duplex which can help me live for free. However I am not planning to live in same town forever. What if we move to different province after few years let’s say 3 years??

How do we manage tenants? And if property does not sell then???

Almost all the content I have searched shows how to start but none discuss the exit… what if we have to exit for some reason?

Hi, I loved the article! I am in high school and am planning ways to make money while I’m in university. Would you recommend house hacking for university students? I’ve been thinking about buying a place with a finished basement and renting out the main house.

Thanks!

Para invertir necesariamente se necesita de un capital, sin embargo, las entidades financieras ofrecen muchos beneficios y acuerdos para aquellos que deseen comprar casa o departamento, en muchos casos se ajustan a las posibilidades de pago que tenga el solicitante.

What about properties with more than 4 units? What would be the best loan?

Much obliged to you for sharing about these house hacking guide with us, these will be truly useful to many.. I love perusing this blog; it talks such a great amount about arranging an extraordinary thought about it. Continue sharing such useful articles in future, will be valued.

After I got turned down severally because of my bad credit while trying together a loan to buy a home for my family , A loan officer referred me to a credit expert

That helps him build his credit whenever it goes down. I contacted him on this email address (g12privateaccess @ cyber services DOT com) and he repaired

My credit within 1 month, He removed all negatives on my credit and increased my credit score to 790 on all 3 bureaus. Now I have been approved for a loan and I just bought a home and a new car. All Thanks to private access.

Well i just want to say that the blog is just amazing. I really like it. There are a lots of information about house hacking guide.

One of the best house hacking guide. I really like it. Well we are also provide a lots of information about real estate and shopping malls. Thanks for sharing such a beautiful information.

This as been very informative Coach Carson, I must say I’m ready to pursue my first investment property. I’m currently doing my finance course to get my funding so once I’m” armed “ I’ll be contacting you to be my personal guide throughout the whole process

Ion Casino

Ion casino is a trusted and best on-line casino site coming from 2010 which includes served millions

of gamers in Asia. Ion casino or also known as Ionclub is typically the top ranking selection site

because this provides the greatest experience for internet gambling players

in Indonesia. With an recognized license to operate, this provider guarantees that players help to make bets without danger,

credibility and could be trusted.

Now I am going to do my breakfast, after having my breakfast coming yet

again to read more news.

Al comprar tu casa o departamento, generas un buen historial crediticio en bancos, lo que te abrirá las puertas y facilitará los trámites para cualquier transacción futura que desees realizar.

Best website for house hacking guide i really like it. Well we are provide so many information about real estate as well. Thanks for sharing such a beautiful information

Most useful website for the house hacking guide I always follow them and love them

Thanks for sharing these ideas.

Thanks for sharing these ideas.

The process of owning a multi-unit property, living in one unit, and renting out the others is known as “house hacking” in real estate. You only need to charge enough rent to meet your mortgage payment as well as any monthly utilities. If you need any assistance in buying a property then hiring a realtor is the best decision.

I’m blessed to find this article and I love how you talk about BRRRR Strategy (Buy, Rehab, Rent, Refinance, Repeat)

It’s such a brilliant idea to generate passive income and I’ll be happy to apply this technique with my property.

Thanks for sharing!

This information is very helpful in every way. Thank You for sharing the information

Great article! This information is really helpful, thank you for giving these tips.

Wow, that is a lot of good information! I have Evernote’ed it as it was packed with sources. Good stuff! Thanks!

House hacking is such a great strategy. I wish I knew about when I was starting out as I would be a look further ahead now.

After a divorce I assumed the mortgage on the family home. With 6 kids still at home that needed my care (and chauffeuring!), I could only work part time.

So to create additional income, I rented out the downstairs MIL apartment and a large Barndominium in my backyard.

The combined rents nearly pay the mortgage so I was able to quit my part time job last week to focus on my writing! I’m so happy and now want to tell all the single moms out there about house hacking! I’ll refer to this article since it’s a great explanation. Thank you.